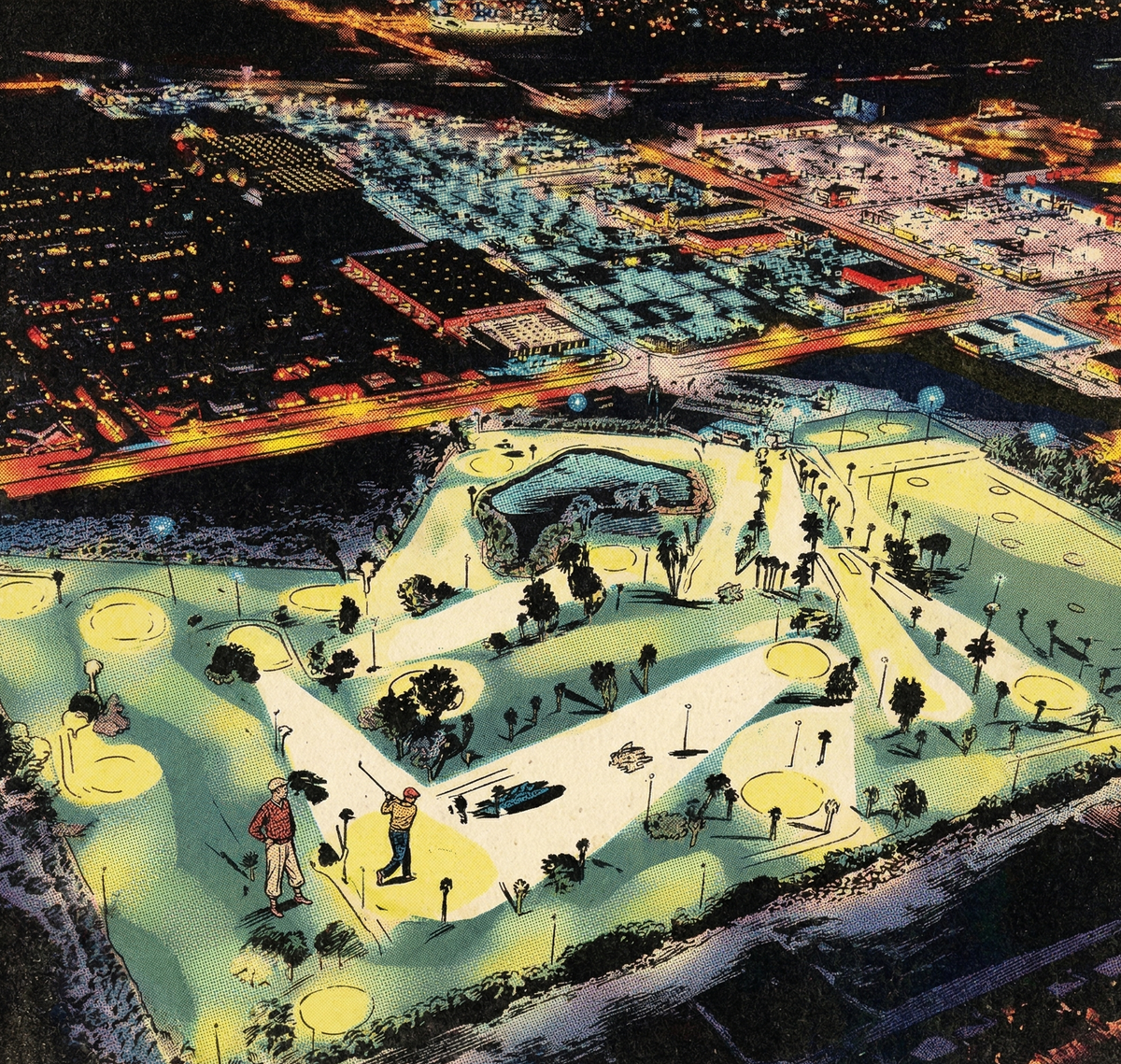

The Lighted Par 3 Opportunity

Google searches for "Par 3 Near Me" have grown 64% since 2019 — more than double the growth rate of "Golf Course Near Me." Of the 16,000 golf courses in the United States, fewer than 60 offer night golf with lights. Consumer demand for shorter-format, accessible golf is accelerating. The supply has barely moved. The lighted Par 3 may be the most underbuilt format in the industry.

Golf is a $140B+ industry. Every week, Perfect Putt breaks down what's actually driving it. Welcome to the new members who've joined since our last send — you're now part of a growing community of 11,000+ golfers who follow the business of the game.

Read Time: 6 minutes

The South Korean Benchmark

South Korea provides the clearest proof of concept for lighted golf. The country operates approximately 514 golf courses. Of those, 117 — over 20% — offer night golf with lights. The comparison is not perfectly analogous: South Korea faces acute land constraints that make traditional course development prohibitively expensive, pushing demand toward indoor golf, screen golf, and lighted formats. But the behavioral insight transfers. When golfers are given the option to play after dark, they take it — and in sufficient volume to justify the capital investment.

The United States has roughly 60 lighted courses across 16,000 total facilities. The penetration rate is less than 0.4%. Even modest adoption of the South Korean model would imply hundreds of additional lighted facilities in the U.S. market.

The Grass Clippings Model

Grass Clippings recently opened a lighted Par 3 golf course in the Phoenix metro area — the first 18-hole lighted course in Arizona. The project offers a granular look at the economics of the format.

The company originated as a golf apparel brand supporting greenskeepers. Community events at Par 3 courses led to the conviction that a lighted format could work commercially. After a lengthy site search — navigating light ordinances, noise restrictions, and the requirement to stay within the Phoenix metro area — Grass Clippings secured a 30-year land lease on Rolling Hills, an executive 18-hole course owned by the city of Tempe.

Grass Clippings and Scottsdale-based WestHawk Capital raised $15 million from investors to fund improvements and build the team. The lighting package alone was significant: 78 lights at a cost of approximately $1.2 million for equipment, plus an additional $1 million in labor and installation. The course was reconfigured — new tee boxes on all Par 4s, one hole redesigned, and a 15,000-square-foot lighted putting green added.

The course plays as a Par 62 during the day (10 Par 3s, 8 Par 4s) and converts to an all-Par-3 layout at night. The superintendent from TPC Scottsdale joined as Director of Agronomy. Troon was hired to manage operations.

The Tee Sheet Advantage

The most compelling economic lever in the lighted Par 3 model is operational: extended hours.

Grass Clippings operates a tee sheet from 7:30 AM to 9:50 PM — over 14 hours of available tee times. A traditional unlighted course in Phoenix operates roughly 10 hours of daylight tee times during peak months, and significantly fewer in winter. The lighted format increases tee time revenue opportunity by an estimated 50% relative to an unlighted facility on the same footprint.

At an average green fee of approximately $60 across day and night play, a fully utilized tee sheet generates roughly $20,000 per day in green fee revenue alone. Grass Clippings' 18-hole green fees range from $45 to $87 — meaningfully below comparable 18-hole public courses in the Phoenix market, where TPC Scottsdale charges $299, Grayhawk charges $306, and We-Ko-Pa charges $179. As part of the land lease agreement with the city of Tempe, Grass Clippings committed to maintaining affordable pricing — a constraint that doubles as a demand accelerator.

The Phoenix heat is the other structural tailwind. Summer daytime temperatures regularly exceed 110 degrees, compressing the playable window for traditional courses into early morning hours. Night golf at Grass Clippings inverts the problem — the hottest months become the highest-demand months for evening tee times. Seasonality flattens rather than concentrating.

The F&B Layer

The entertainment golf category has demonstrated consistently that food and beverage can represent 50% or more of total facility revenue. Topgolf, PopStroke, Puttshack, and Five Iron all operate on models where the golf experience is the traffic driver and F&B is the margin engine.

Grass Clippings is building into that model. The property includes a 5,000-person event space for concerts, with plans for a new clubhouse in the coming months. The positioning is deliberate: a lighted Par 3 is not just a golf course with lights. It is a golf entertainment venue with a real golf course as its anchor — a format that captures both the committed golfer and the social golfer in a way that a traditional facility cannot.

The incremental economics of F&B on top of the extended tee sheet create a revenue model that is structurally different from a traditional daily-fee course. Green fees provide the base. Extended hours expand the base by 50%. F&B captures an additional revenue stream on every round played. The three layers compound on the same fixed-cost infrastructure.

The Commercialization Wave

Grass Clippings plans to build four to five additional locations in warm-climate markets across the United States. 8AM Golf acquired 3s — a lighted Par 3 in South Carolina — and announced plans to open two new locations in Las Vegas and Nashville.

The golf entertainment category has been commercialized across multiple formats: Topgolf owns the driving range. PopStroke owns outdoor putting. Puttshack owns indoor putting. Five Iron owns indoor simulator golf. The Par 3 format — the one closest to actual golf — has not yet been commercialized at scale.

That is beginning to change. The demand signal from Google search data is clear. The economic model — extended hours, accessible pricing, entertainment layering, F&B capture — is structurally sound. The South Korean market demonstrates that lighted golf works at meaningful penetration rates. And the first wave of operators is building with institutional capital behind them.

The Takeaway

The lighted Par 3 sits at the intersection of three forces: consumer demand for shorter, more accessible golf formats; the golf entertainment trend that has proven F&B and experience layering drive margin; and the operational leverage that comes from extending the playable day by 50% through lighting.

Fewer than 60 lighted courses exist in a country with 16,000 golf facilities and 47 million people who engage with the sport. Consumer search interest in Par 3 golf is growing at double the rate of traditional golf courses. The first institutional-quality operators are raising capital and securing sites.

The Par 3 format is the closest thing to real golf in the entertainment category — and the lighted version may be the format's most investable expression. The commercialization cycle is early. The economics are compelling. And the gap between consumer demand and available supply is as wide as any in the golf industry today.

The best way to support Perfect Putt is to subscribe and share with a friend.