Golf's Capital Gap

Breaking down Old Tom Venture Club

Golf generated $102 billion in direct economic impact in 2022 — up 20% from 2016. The growth is structural: junior participation at its highest since 2006, female golfers above 6 million for three straight years, off-course golf up 68% in four years. The sport is in the strongest commercial position it has occupied in two decades. The capital being deployed to the entrepreneurs building inside it does not match the scale of the opportunity.

Read Time: 6 minutes

The Thesis

Matthew Erley and Evan Roosevelt identified a simple problem: there is not enough venture capital being deployed in the golf industry. Erley spent the better part of his career on the growth side of startups — including Drizzly and Havenly — before angel investing led him into conversations with golf entrepreneurs. Roosevelt co-founded Random Golf Club. Together, they saw the same gap from different angles.

The problem compounds. If founders in golf do not have exit pathways, they are less likely to reinvest back into the industry. If the reinvestment cycle breaks, innovation slows. The flywheel that drives entrepreneurial ecosystems in technology, consumer, and healthcare — where successful founders become angel investors and mentors to the next generation — barely exists in golf.

So they built one. Old Tom Venture Club launched a little over a year ago as a syndicate model designed to connect accredited investors with golf-specific venture opportunities at check sizes that the industry had not previously accommodated.

How It Works

The structure is straightforward. Old Tom Venture Club operates as a syndicate with an initiation fee and no annual dues. Members must be accredited investors — individual income over $200,000 or joint income over $300,000, or a net worth exceeding $1 million excluding primary residence.

The club conducts due diligence on several dozen companies annually. When a company is selected for investment, the opportunity is shared with syndicate members for review. Members choose whether to participate on a deal-by-deal basis. Individual checks can be as small as $10,000 — well below the minimum threshold most early-stage companies would accept from a direct investor. The syndicate aggregates smaller commitments into a single institutional-sized check, giving individual investors access to deal flow and allocation they could not access independently.

The model solves two problems simultaneously. Founders get access to a curated investor base with deep golf industry knowledge and networks. Investors get access to vetted deal flow in a sector they understand, at check sizes that allow portfolio diversification across multiple companies.

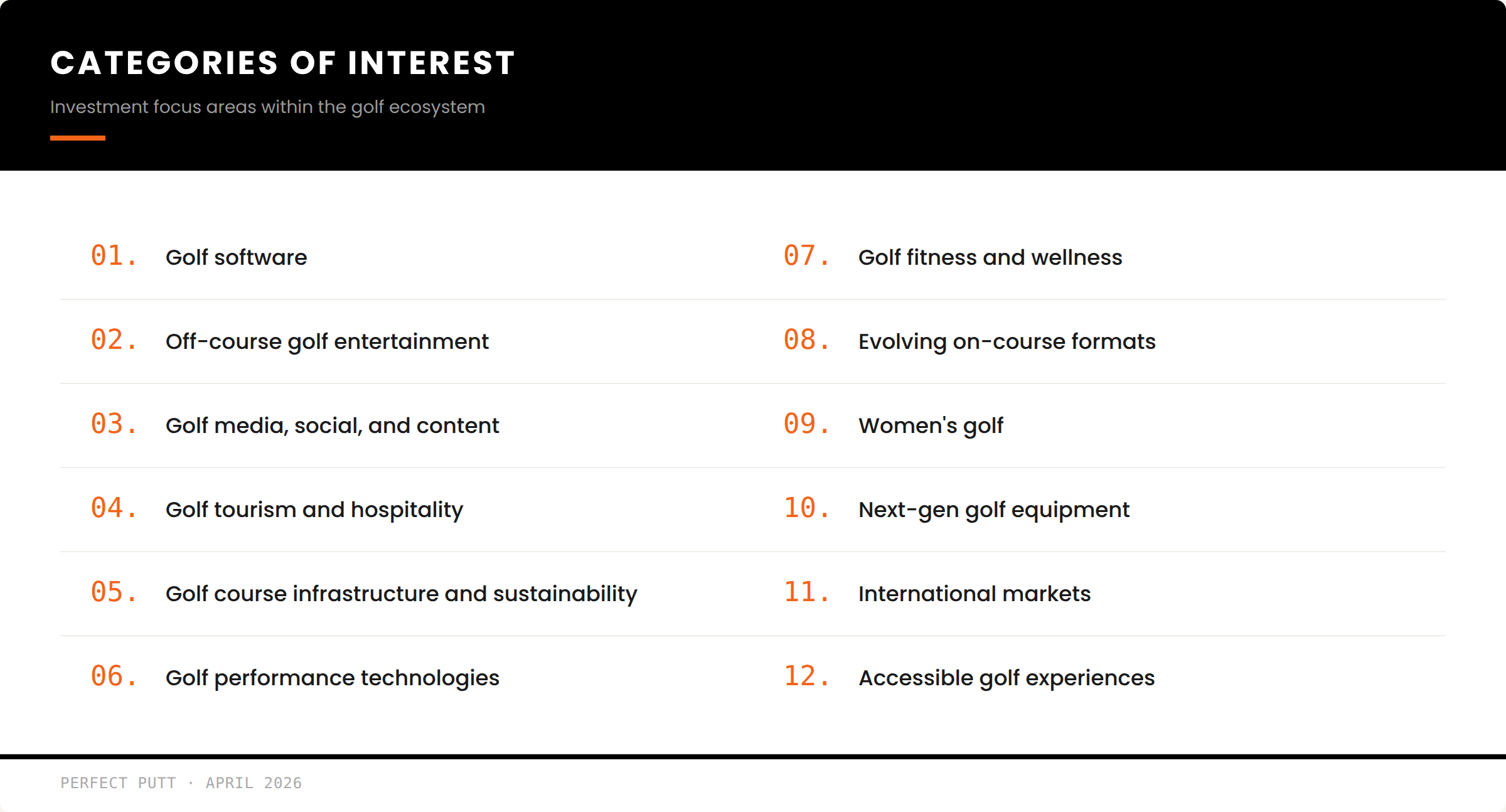

The Investment Lens

Old Tom Venture Club evaluates opportunities across twelve areas within the golf ecosystem. The exclusion list is equally instructive: they do not invest in golf courses, hyper-competitive categories like apparel or club manufacturing, or startups that lack a credible path to $100 million or more in enterprise value.

The logic is sound. Golf courses are capital-intensive, illiquid, and operationally complex — they are real assets, not venture opportunities. Apparel and equipment manufacturing are dominated by established OEMs with massive distribution networks and brand moats — the arbitrage for a venture investor is minimal. And the $100 million enterprise value threshold ensures the fund is targeting businesses with genuine platform potential rather than lifestyle businesses or niche products.

The syndicate invested in four companies in 2023: Fairgame, Dryvebox, Puttr, and Sweetens Cove Spirits. The plan for 2024 is eight investments. The membership base exceeds 100 investors — ranging from a top-50 professional golfer to members of the most exclusive golf clubs in the country.

The Broader Landscape

Old Tom Venture Club is not operating in a vacuum. The golf industry has seen significant institutional capital activity in recent years. Centroid acquired TaylorMade for a reported $1.9 billion in 2021. Callaway completed the Topgolf merger at $2.6 billion. 8AM Golf has assembled a portfolio of investments across the industry. The PGA of America partnered with Elysian Park Ventures to form EP Golf Ventures — a strategic move to support innovation within the PGA Professional ecosystem.

But the vast majority of that capital has been deployed at the top of the market — large-scale acquisitions, institutional buyouts, and strategic partnerships involving established brands. The early-stage layer — seed rounds, Series A investments, angel checks — remains dramatically underfunded relative to the size and growth trajectory of the industry.

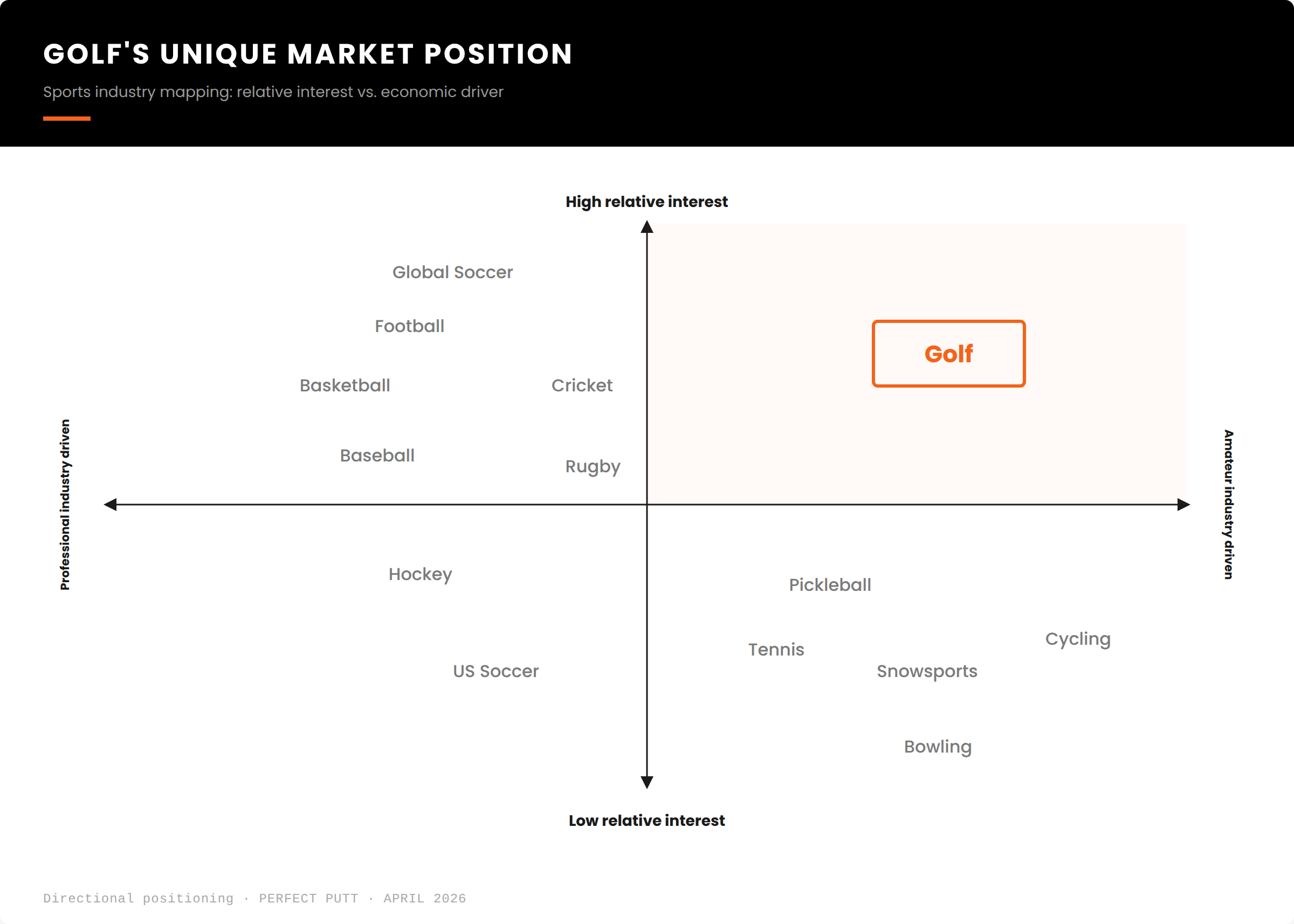

Consider the math. Golf is a $102 billion direct economic impact industry in the United States alone. It has nine consecutive years of more than two million beginner golfers. It ranks in the top ten recreational sports in America by participation — both on-course and off-course. The demographic growth is skewing younger, more female, and more tech-native. And the venture capital infrastructure serving this ecosystem is a handful of firms and a single syndicate.

Compare that to industries of similar scale — fitness, outdoor recreation, sports technology — where dozens of dedicated funds compete for deal flow and founders have multiple pathways to institutional capital. Golf is dramatically under-indexed for the capital that its growth trajectory should attract.

Why It Matters

The entrepreneurs building in the golf industry today are solving real problems: tee time optimization, simulator software, AI-powered coaching, mobile golf entertainment, creator monetization, junior development technology, and course management infrastructure. These are not speculative categories. They are responses to documented demand gaps in a $102 billion industry that is growing.

What those entrepreneurs need is capital, mentorship, and a network that understands the industry they are building in. The traditional venture ecosystem — Sand Hill Road generalists evaluating golf alongside fintech and enterprise SaaS — does not provide that. Golf-specific investors do.

Old Tom Venture Club's model is one answer. It may not be the only answer. But the thesis that underpins it — that golf needs more capital deployed at the early stage, that the reinvestment flywheel matters, and that the industry's growth will eventually attract institutional attention to the startup layer — is difficult to argue against.

The Takeaway

Golf's commercial position is the strongest it has been since the Tiger Boom. Participation is at record levels. Demand for new experiences is expanding. The demographic shift toward younger, more diverse, more technology-forward golfers is creating market opportunities that did not exist a decade ago.

The entrepreneurs are showing up. The capital is beginning to follow. The gap between the scale of the opportunity and the volume of early-stage investment being deployed remains significant — but it is narrowing. The firms and syndicates that establish themselves as the institutional infrastructure for golf venture capital now will be positioned at the center of the industry's next wave of innovation.

The game is growing. The businesses inside it need to grow with it. That requires capital — and more of it.

The best way to support Perfect Putt is to subscribe and share with a friend.