Golf's R&D Problem

Golf holds more patents than every other major sport combined — but the last transformational equipment innovations arrived decades ago. R&D spending at the major OEMs is growing in absolute dollars but declining as a share of revenue. The real innovation is happening at the edges: AI coaching, simulator software, VR golf, and the entrepreneurs building new categories that the established companies are structurally unlikely to invent. Golf's next breakthrough will come from a smaller company, just as it always has.

Golf is a $140B+ industry. Every week, Perfect Putt breaks down what's actually driving it. Welcome to the new members who've joined since our last send — you're now part of a growing community of 11,000+ golfers who follow the business of the game.

Read Time: 5 minutes

What the R&D Spend Tells Us

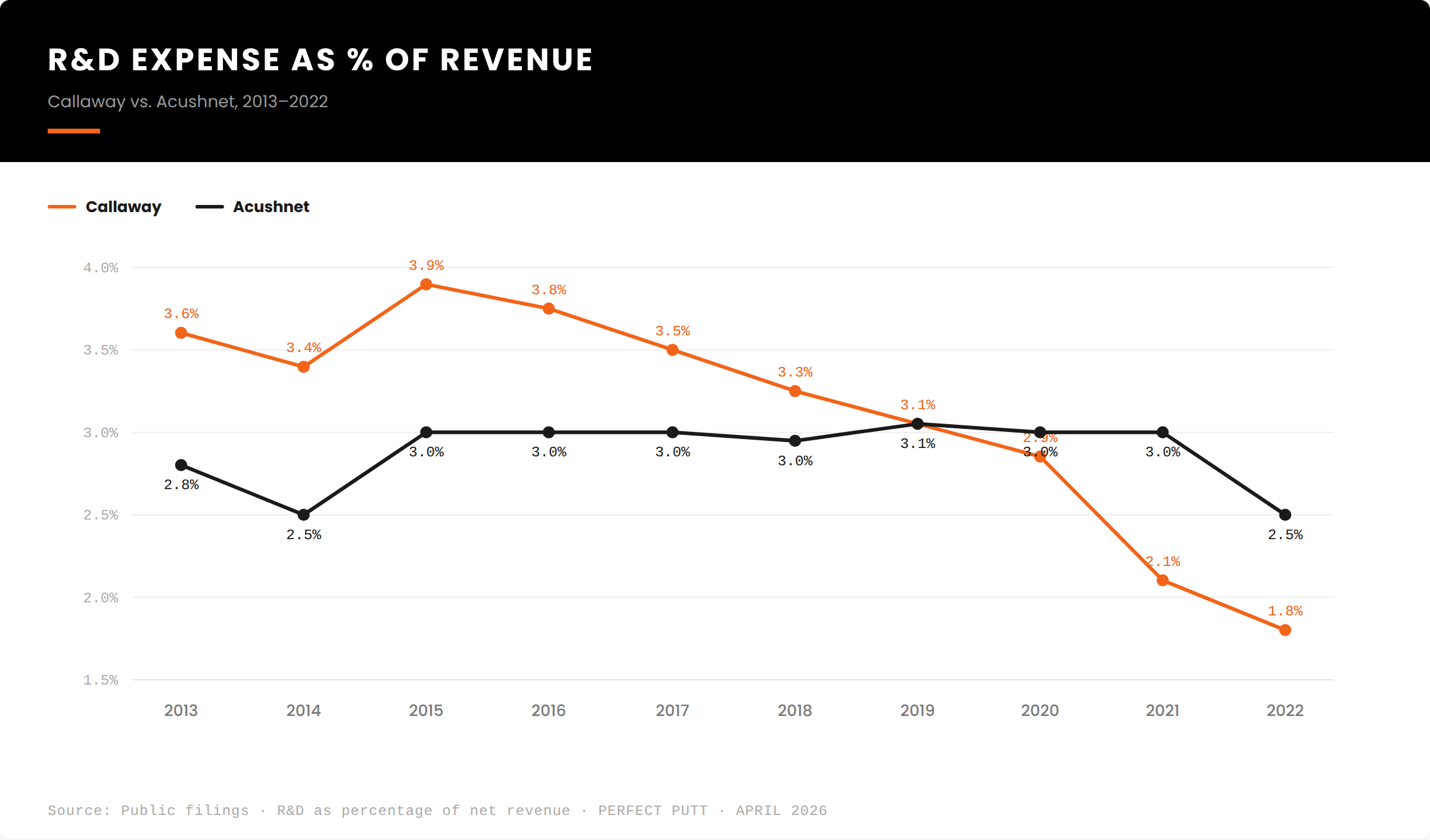

Acushnet and Callaway are both publicly traded, which means their research and development budgets are visible. The trajectory is instructive.

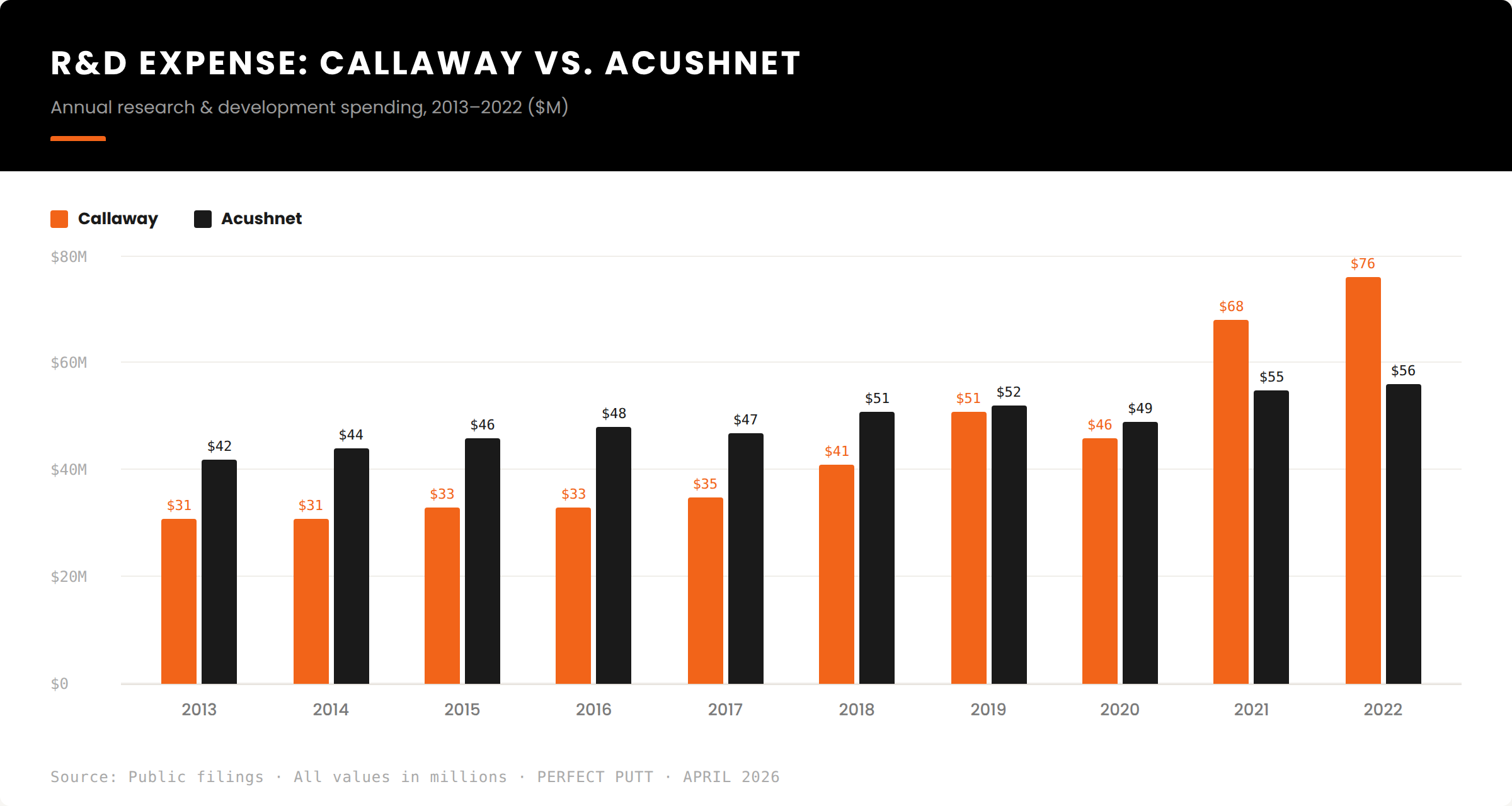

Since 2013, Callaway has more than doubled its annual R&D expenditure. Even before the Topgolf acquisition inflated the number, the trend was clear — Callaway increased R&D spending by 24% between 2018 and 2019 alone. Acushnet's growth has been more restrained: a 33% increase over the same period, with the largest single-year jump at 12% in 2021.

The absolute dollar figures suggest both companies are investing more than ever in innovation. But the relative picture tells a different story. R&D as a percentage of revenue — the figure that measures how much of the business is allocated to invention — has been declining at both companies in recent years. Callaway peaked in 2015. Acushnet peaked in 2019. Both have trended down since.

Revenue has grown faster than R&D spending. The companies are getting larger, but the share of the business dedicated to developing new products is shrinking. That is not inherently a problem — mature manufacturing companies in most industries follow the same trajectory. But it does raise the question of where the next breakthrough comes from.

How Golf Compares

The top R&D-intensive industries spend at levels that make golf equipment look like a rounding error. Biotechnology allocates approximately 30% of revenue to R&D. Software spends 19%. Semiconductors spend 17%. These are industries where the product cycle is defined by invention — if you stop spending, you stop existing.

Golf equipment is a manufacturing business, and the better comparison is automotive. The top five automotive companies — General Motors, Mercedes-Benz, Volkswagen, Ford, and Honda — spend between approximately 4.9% and 6.3% of revenue on R&D. Acushnet and Callaway sit in a comparable range, though trending toward the lower end.

The comparison is imperfect. Automotive R&D is driven by regulatory requirements (emissions, safety) and platform transitions (electric vehicles) that have no direct parallel in golf. But the pattern is consistent: mature manufacturing industries allocate R&D to incremental product improvement, not to fundamental category reinvention. Golf equipment R&D produces the next generation driver — not the next generation of the sport.

The Golf Ball Case Study

Callaway's golf ball investment is the clearest example of how R&D capital flows within the established OEM model. Callaway acquired Top-Flite in the early 2000s for approximately $125 million. Several years later, Callaway invested an additional $50 million into its golf ball manufacturing plant. The result: Callaway is the fastest-growing golf ball company since 2013, commanding approximately 20% of a market valued at roughly $1.3 billion.

The investment has returned meaningful value. But the product itself — while improved in materials, construction, and aerodynamics — has not changed the game in the way that the original solid-core ball replaced the wound ball. The R&D produced a better version of the existing product. It did not produce a new category.

That is the structural pattern. Established OEMs are incentivized to optimize the current product architecture — longer drivers, softer balls, more forgiving irons — because their revenue depends on upgrade cycles within existing categories. A truly disruptive innovation would obsolete their own inventory, disrupt their retail channel relationships, and require golfers to rethink equipment decisions they have already made. The business model rewards iteration, not reinvention.

Where the Innovation Is Actually Happening

The most significant innovation in golf over the past five years has not come from the traditional OEMs. It has come from off-course golf, golf technology, and the entrepreneurs building new categories entirely.

Sportsbox AI — now owned by Bryson DeChambeau — is building an agentic AI coaching assistant that captures swing data through a phone camera and delivers real-time diagnostic feedback. GOLF+ pioneered virtual reality golf and is expanding into traditional simulator software with mixed-reality putting that solves one of the category's oldest problems. Launch monitor companies have compressed the price of tour-grade ball flight data from $15,000 to under $700 in five years. GSPro has built a community-created course library of over 2,000 tracks on a $250-per-year subscription.

None of these innovations came from Acushnet or Callaway or TaylorMade. They came from startups, entrepreneurs, and small teams building at the edges of the industry — exactly where Karsten Solheim was when he machined the first PING putter in his Redwood City garage in 1959.

The Entrepreneurial Pipeline

The golf industry is experiencing an influx of entrepreneurial talent that it has not seen in decades. The post-2019 participation boom — 47 million Americans playing golf in some form, 19 million exclusively off-course — has created a demand environment that attracts builders. Founders in their twenties are launching companies with real products, real revenue, and real capital behind them.

The large OEMs will continue to invest in R&D. They will continue to produce incrementally better equipment. And those products will continue to sell — Titleist's Pro V1 franchise, Callaway's driver business, and TaylorMade's iron category are not going anywhere.

But the next breakthrough — the innovation that changes how golf is played, taught, experienced, or consumed — will almost certainly not come from inside those companies. It will come from the same place it always has: a founder with a thesis, a garage, and the conviction that the game can be better.

The best way to support Perfect Putt is to subscribe and share with a friend.