The Tariff Impact on Golf

The golf industry's biggest equipment makers are budgeting well over $100 million in tariff costs for 2026. That is real margin being extracted from an industry still finding its footing after years of pandemic-era volatility, supply chain disruption, and consumer price fatigue. The 10% Section 122 duty runs through July 24 with no visibility into what follows. OEMs cannot confidently price procurement when the policy may simply evaporate. The tariff is a cost. The uncertainty is the real tax.

We know. You subscribed for the business of golf, not a trade policy seminar. But when the tariff math starts showing up in driver prices and earnings calls, it becomes a golf story whether we like it or not. Bear with us — this one matters.

Golf is a $140B+ industry. Every week, we break down what's actually driving it. Welcome to the new members who've joined since our last send — you're now part of a growing community of 11,000+ golfers who follow the business of the game. If someone forwarded this to you, subscribe below.

Read Time: 7 Minutes

The Policy Backdrop

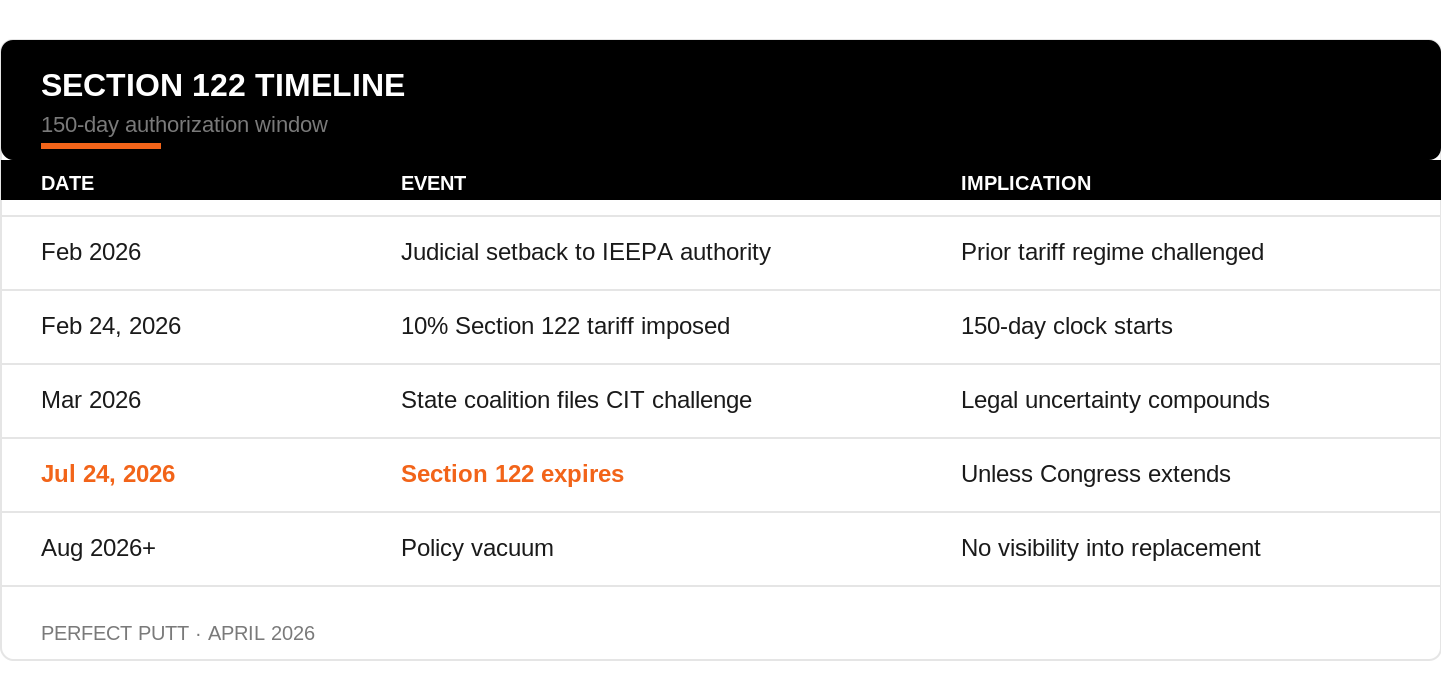

After the courts blocked the administration's prior IEEPA tariff authority, the White House pivoted to Section 122 of the Trade Act of 1974 — a narrower tool that allows temporary duties of up to 15% for balance-of-payments purposes. The catch: Section 122 is capped at 150 days unless Congress extends it. Congress is unlikely to do so.

A coalition of states has challenged the measure at the Court of International Trade, arguing Section 122 was improperly invoked. The tariff carves out certain metals, energy products, and goods already covered by Section 232 duties, and CBP has treated qualifying USMCA imports as exempt. Golf equipment got no such carve-out. But the legal outcome matters less than the clock. A 10% duty that could expire in months, jump to 15%, or be replaced entirely is not a pricing problem. It is a planning problem.

What History Tells Us

Golf has been through tariff cycles before. The outcomes are instructive.

In 2018, Section 301 tariffs on Chinese goods started at 10% and escalated to 25% by mid-2019. Club heads, shafts, and grips were all on the list. The margin hit for major OEMs was real but manageable — single-digit millions on smaller revenue bases. The industry did not re-shore. It diversified across Vietnam and Indonesia, moves that took five to six years to play out. The lesson: tariffs do not bring manufacturing home. They redistribute it across lower-cost geographies. Slowly.

Golf carts tell the sharper story. Despite general tariff coverage on Chinese goods, Chinese cart imports surged — manufacturers reclassified vehicles, shipped through third countries, and exploited regulatory loopholes. By 2024, the American Personal Transportation Vehicle Manufacturers Coalition, led by Club Car and Textron, pursued antidumping and countervailing duty relief. The resulting AD/CVD orders carried duties reportedly exceeding 600%. In our reading of that case, the original tariff regime produced circumvention, not protection. Enforcement lagged years behind the problem.

Then there is the Mexico question. In 2021, CBP ruling HQ H313087 held that golf clubs assembled in Mexico from Chinese-origin heads, shafts, and grips remained Chinese in origin for Section 301 purposes — the Mexican assembly did not constitute substantial transformation. Assembling elsewhere did not change where the product came from. For any OEM exploring nearshoring under USMCA today, that precedent is directly relevant.

Where Golf Equipment Actually Comes From

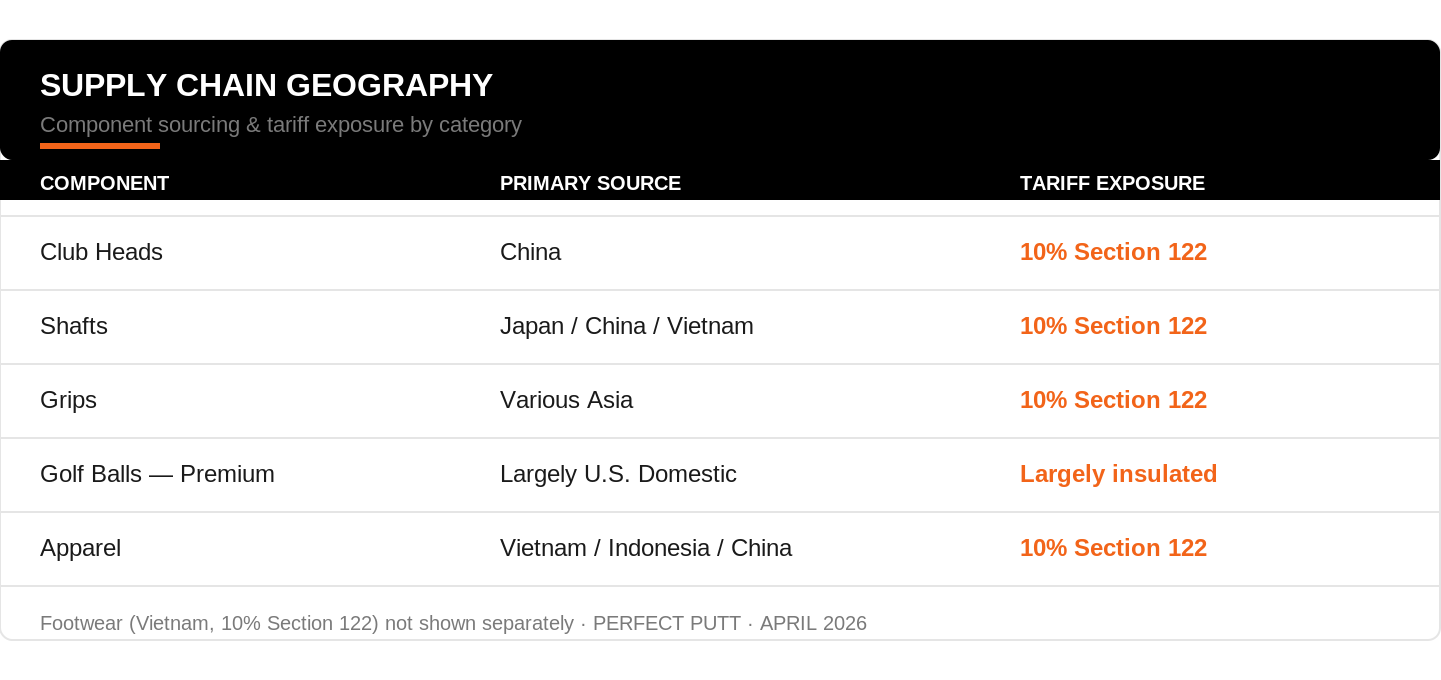

Golf balls are the bright spot. Several major OEMs maintain significant domestic ball production in Massachusetts and South Carolina, which reduces tariff exposure on their highest-margin consumable line. The degree of insulation varies by manufacturer, but the product category is partially shielded.

Everything else is Asia. Club heads from Chinese forging operations. Shafts from Japan, China, and Vietnam. Grips from various Asian suppliers. Apparel from Vietnam, Indonesia, and China. Footwear mostly from Vietnam. This supply chain has been optimized for cost over two decades — and as the 2018-2019 cycle showed, tariffs rearrange it across Asia rather than bringing it home.

Ping is the partial exception, with significant manufacturing in Phoenix. But even Ping supplements with overseas production. Domestic presence is not domestic immunity.

OEM Exposure

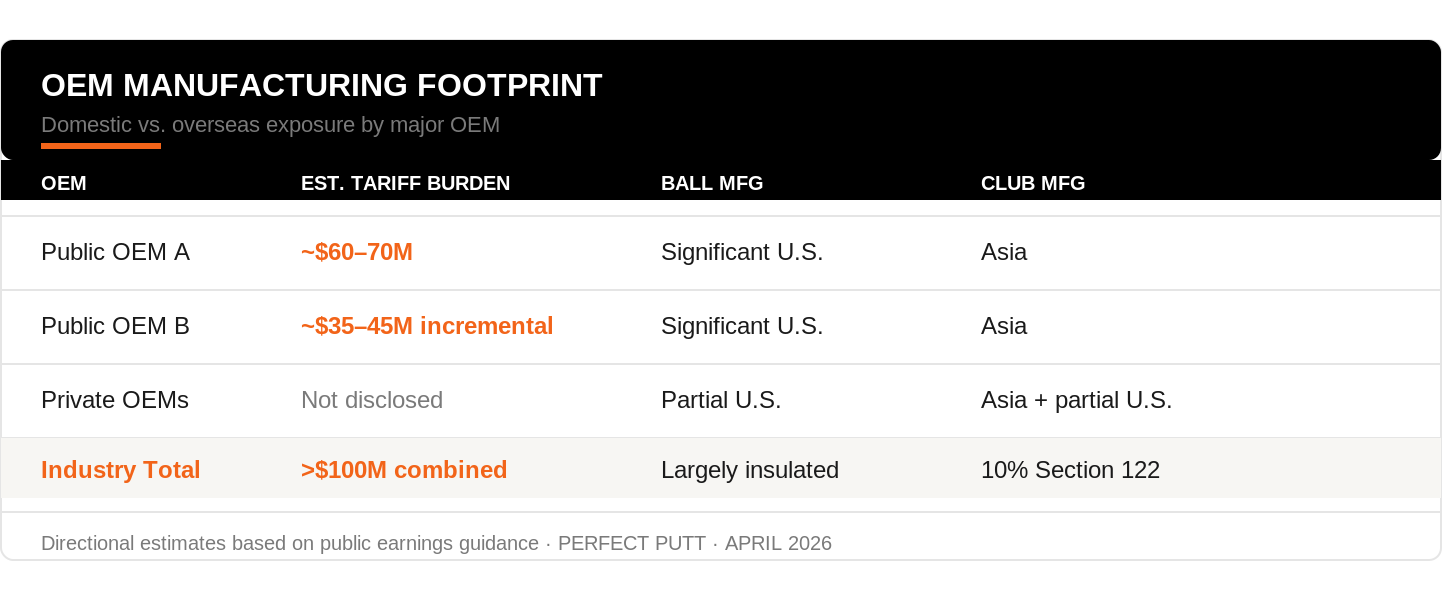

Based on recent earnings guidance, the two largest public OEMs alone imply more than $100 million in combined 2026 tariff cost — ranging from roughly $40 million to $70 million each depending on product mix and sourcing. The playbook is familiar: strategic pricing, supplier cost-sharing, sourcing shifts. But the scale is an order of magnitude larger than 2018-2019. What was a single-digit-million headwind is now structural margin compression.

Ball production provides partial domestic insulation. Clubs do not. Hardgoods are overwhelmingly sourced from China, Indonesia, Thailand, and Vietnam. For OEMs managing capital structure transitions or upcoming earnings windows, the tariff compounds already-complex financial positioning.

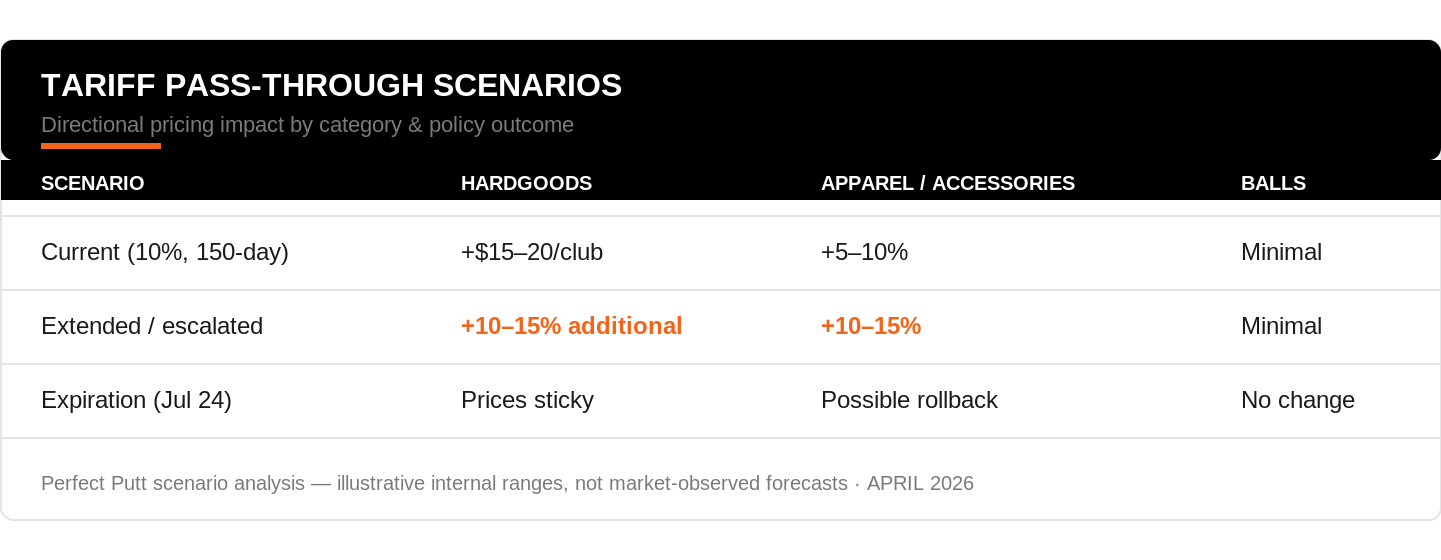

Private manufacturers do not disclose exposure, but their clubs come from the same Asian geographies. The private structure shields them from quarterly earnings pressure — a real advantage here. Across the industry, initial price increases of $15 to $20 per club are already in market. Every OEM is running the same math with different levels of visibility.

What the Consumer Sees

Equipment prices have climbed steadily over the past decade on the back of materials costs, technology investment, and input inflation. Several OEMs have already added $15 to $20 per club in early 2026 tariff pass-throughs. The question is what comes next.

If Section 122 extends past July 24 or gets replaced by something broader, a second round of increases becomes likely across hardgoods and apparel. Even a further 10% to 15% pass-through would push premium pricing into territory that tests willingness to pay. Prices were already elevated before the tariff landed. The structural risk is not the first increase — it is the cumulative weight of successive ones.

At some point, the recreational golfer delays a purchase, trades down, or buys used. That threshold varies by category — clubs are more discretionary than balls — but it is closer than the market is pricing.

The Uncertainty Premium

The tariff cost is mechanical. The uncertainty is structural. OEMs can still sign contracts, but they cannot confidently lock in multi-quarter economics or 2027 pricing until they know whether Section 122 expires, extends, or gets replaced by something else entirely. Companies that entered the year with stable guidance are now managing 150-day windows instead of fiscal years.

The early demand signals are mixed. Industry trackers reported strong retail sell-through in late 2025, but channel data through Q1 2026 suggests moderation — particularly in mass and sporting goods, where price sensitivity surfaces first. Whether that softening reflects tariff-driven caution, post-cycle normalization, or both is not yet separable in the data. What is clear: OEMs entering their peak selling season are planning against a demand curve they cannot confidently model.

Risks and What Comes Next

Three scenarios define the back half of 2026. Section 122 expires July 24 — OEMs who raised prices face consumer pushback and cannot easily reverse. Congress extends or the administration pivots to a different authority — uncertainty compounds. The Court of International Trade strikes the proclamation down — legal chaos with lower direct cost. Our base case is expiration, though replacement under a different authority remains possible. The 2018-2019 cycle started as "temporary" too. Those Section 301 tariffs are still in effect seven years later.

The most exposed players are not the major OEMs. They are the smaller brands with thin margins and no domestic manufacturing. The golf cart precedent is instructive: in our reading of the 2024 trade case, the initial tariff produced circumvention and consolidation pressure, not re-shoring. A similar dynamic could emerge in equipment if Section 122 is extended.

How the Industry Is Mitigating

The mitigation playbook follows familiar patterns. The first lever is geographic diversification — shifting manufacturing or final assembly to countries with more favorable trade treatment. Same response as the 2018 Section 301 cycle. The second is broadening the supplier base: reducing single-source concentration on Chinese components and building dual-sourcing arrangements for both leverage and continuity.

Beyond sourcing, OEMs are renegotiating cost-sharing with suppliers — spreading the tariff across the value chain instead of absorbing it at the brand level. Companies with Mexico operations are pursuing USMCA compliance for duty-free treatment, though the 2021 CBP substantial transformation ruling limits that path for products assembled from Chinese-origin components.

On the logistics side, bonded warehouse structures are gaining traction — converting distribution centers to bonded facilities to defer duties and re-export without incurring tariffs. The most sophisticated operators are building tariff simulation tools that fold policy variables into procurement planning. None of these strategies eliminate the tariff. Together, they compress the margin impact from catastrophic to manageable — as long as the policy window holds at 150 days.

The Capital Implication

The combined tariff burden across the largest OEMs exceeds $100 million. Material, but not terminal. These manufacturers have the scale, partial domestic insulation, and pricing power to manage through a 150-day window — especially with the mitigation playbook in motion. What they cannot manage through is permanent ambiguity. In our assessment, public OEM multiples already reflect this — the market cannot model what comes after July 24. Every upcoming earnings call will be read through a tariff lens.

The deeper risk is compounding price fatigue. If tariffs persist or broaden, successive rounds of increases push consumers toward substitution — buying used, delaying purchases, trading down. For investors, the posture is defensive until July 24 resolves: favor domestic production exposure, strong balance sheets, and the pricing discipline to avoid chasing margin in a volatile window. The tariff is temporary. The planning vacuum it created is the lasting damage.

Not every Thursday deep dive will read like a trade policy briefing. But when $100+ million in industry margin is on the table this summer, it is worth understanding what is actually happening.

Enough tariff talk – Go kick your feet up, sip on an Azalea, and Enjoy Augusta.

We'll see you next week.

The best way to support Perfect Putt is to subscribe and share with a friend.