The Next Decade of Golf Agronomy

Golf course maintenance appears to be moving toward lower-input, precision-managed systems. The operators and investors who understand the transition early may own a structural advantage.

TODAY'S SPONSOR

Before we get into it. This week's Perfect Putt is presented by The Club by Old Tom Capital.

The golf industry is being rebuilt by a new generation of founders, operators, and investors. The course concepts, the technology, the brands shaping where the game goes next. Those deals move through a room. The Club by Old Tom Capital is that room.

A private network of accredited investors deploying capital into the corners of the golf economy where value has been overlooked and access has been thin. The companies making the game better, more global, and more inclusive for the next generation of people who play it. Ten or more deals a year, sourced from inside the ropes.

If you’ve ever finished a deep dive thinking, I would invest in that, The Club is where those conversations become allocations. Limited membership.

Now, onto this week's deep dive.

Read Time: 7 Minutes

The Current Operating Model

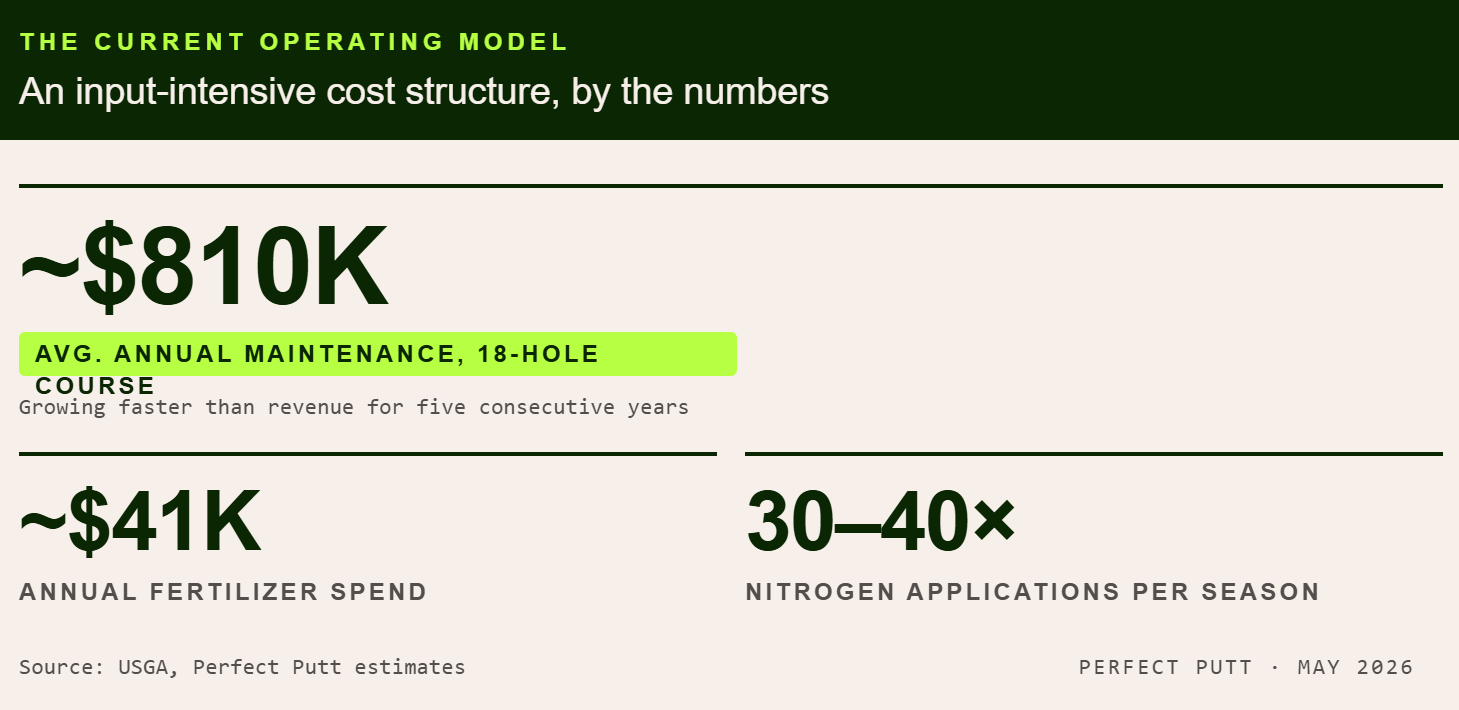

An 18-hole golf course is among the most input-intensive managed landscapes in commercial real estate. Maintaining 150 or more acres of playing surface requires continuous synthetic fertilizer applications, chemical disease treatments, mechanical thatch removal, precision mowing, and irrigation management. The average facility spends roughly $810,000 per year on maintenance, per USGA data, a figure that has grown faster than revenue for five consecutive years.

The model is built on frequency and intervention. Nitrogen is applied 30 to 40 times per season. Fungicide programs run on preventive calendar schedules. Thatch is managed through core aeration and verticutting that require multi-day course closures. Irrigation typically operates from a single weather station estimate applied uniformly across microclimates that vary dramatically within a single hole. Core agronomy inputs including fertilizer, chemicals, fuel, and electricity are increasingly tied to volatile energy-linked commodity markets that operators cannot effectively hedge or pass through. Labor markets are tightening, while regulatory pressure around nitrogen runoff, water usage, and chemical application is increasing across many of the coastal, arid, and resort markets where premium golf is concentrated.

The system has produced exceptional playing surfaces for decades. It is also expensive, chemically dependent, labor-intensive, and reactive by design. The question facing operators is whether the next generation of turf management tools can deliver comparable or better surfaces with structurally lower input intensity, reduced labor dependency, and less operating volatility.

From Reactive Management to Precision Systems

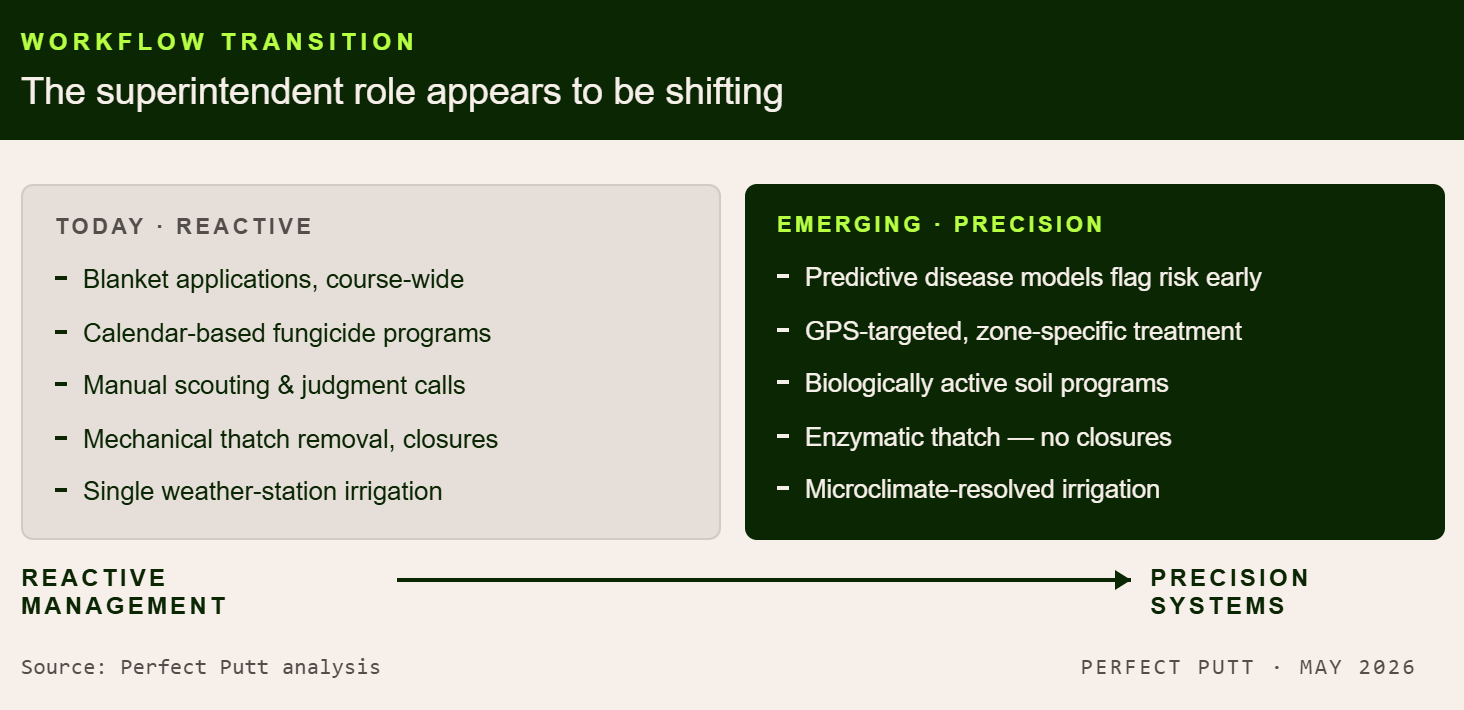

The role of the golf course superintendent is beginning to change. Not everywhere, and not at the same pace, but the direction is visible at the leading edge of the profession.

Today, most superintendents manage turf through a pattern of blanket applications, reactive disease treatment, scheduled mechanical interventions, manual scouting, and experience-based judgment calls made dozens of times per day. Generalized agronomic programs are applied broadly across the property. When disease or stress appears, the response is typically course-wide treatment rather than zone-specific intervention. The work is physically demanding, time-sensitive, and dependent on a labor force that is increasingly difficult to recruit and retain.

The model that appears to be forming looks different. Some superintendents are beginning to work with predictive disease models that flag risk before symptoms appear. Precision application technology, guided by GPS and informed by hyperlocal microclimate data, enables targeted treatment in the specific zones where pressure exists rather than blanket spraying the entire property. Biologically active soil programs may reduce the frequency of synthetic inputs over time. Enzymatic treatments can replace some mechanical thatch removal, reducing time for course closures. Real-time monitoring platforms are beginning to give superintendents a data picture that was previously unavailable: moisture levels, disease risk, shade exposure, and turf stress mapped across the entire course at high resolution.

When (not if) these tools mature and adoption broadens, the superintendent role will evolve from reactive turf management toward precision systems management. That is a meaningful operational shift. It implies fewer blanket treatments, fewer emergency interventions, fewer disruptive closures, and more time spent interpreting data, benchmarking performance, and optimizing programs across properties. For multi-course operators, it will also mean standardized protocols, centralized agronomic dashboards, and portfolio-level benchmarking that does not exist in most organizations today.

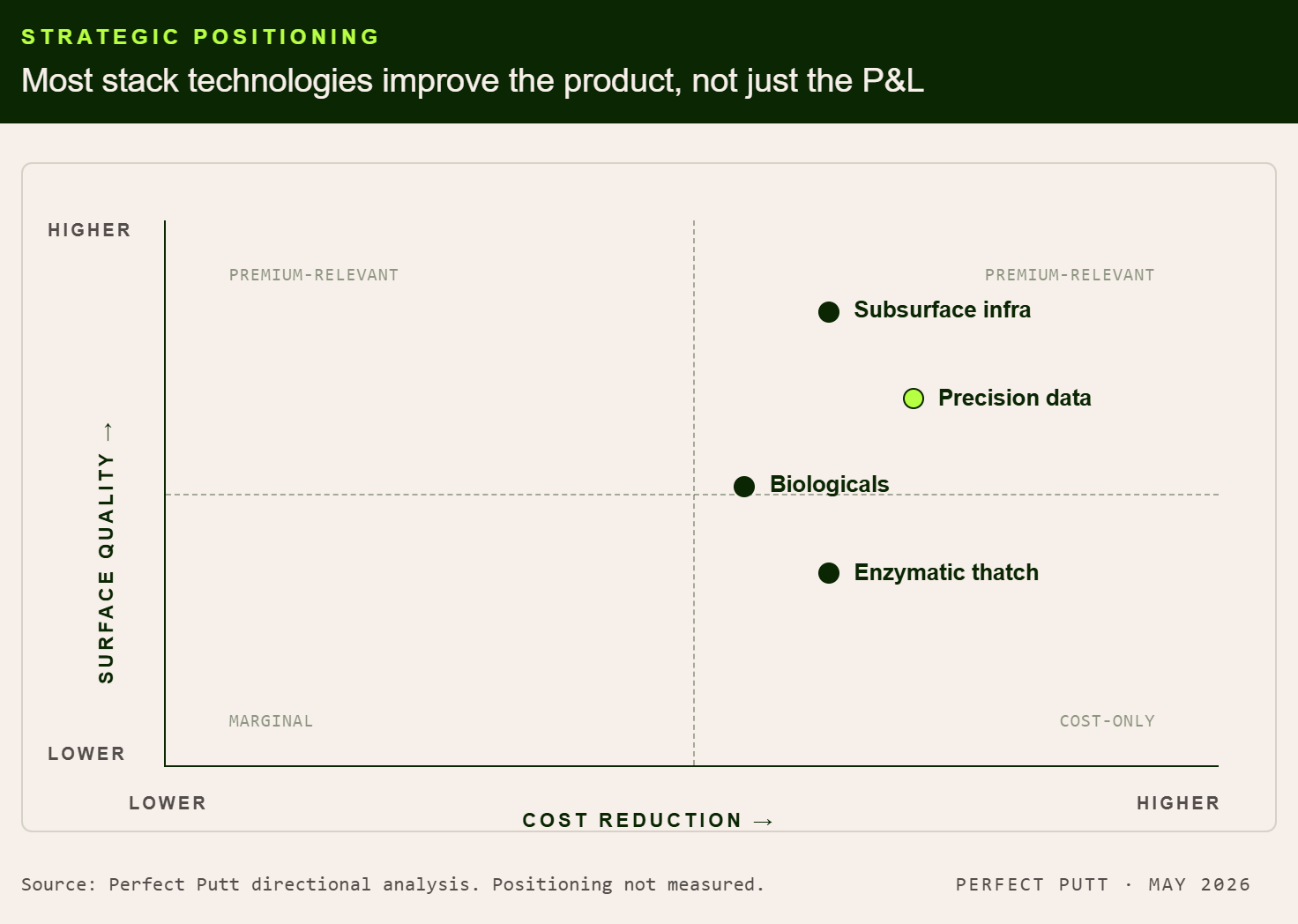

The Surface Quality Thesis

The cost argument alone is unlikely to drive adoption at the top of the market. Premium courses and private clubs do not make agronomic decisions primarily on cost. They make them on surface quality, consistency, and member experience.

This is where the thesis gets more interesting. Many of the emerging technologies being tested in golf agronomy have the potential to improve the playing product itself, not merely reduce the expense of maintaining it. Biologically active soils tend to produce healthier root systems, which can improve turf resilience under heat, drought, and traffic stress. Precision irrigation matched to actual microclimate conditions, rather than property-wide estimates, could deliver more consistent moisture profiles across greens, improving firmness and reducing the surface variability that golfers notice most. Subsurface drainage systems that control water movement through the root zone may extend playability through weather events and reduce the recovery time after heavy rain. Enzymatic thatch and algae management supports a cleaner soil profile, reducing surface disruption while delivering smoother, more consistent putting surfaces with fewer maintenance-related closures.

The combined effect, if these systems deliver on their early promise, is not simply cheaper maintenance. It is more consistent greens, healthier turf under stress, fewer weather-related closures, improved recovery after events, more predictable playing conditions across seasons, and a higher-quality experience for the golfer. That is the argument that could move premium operators. A course that produces better surfaces year-round with less volatility and fewer disruptions has a structural advantage in member retention, guest satisfaction, and pricing power. The cost savings may follow, but the surface quality thesis is likely the stronger commercial driver at the top of the market.

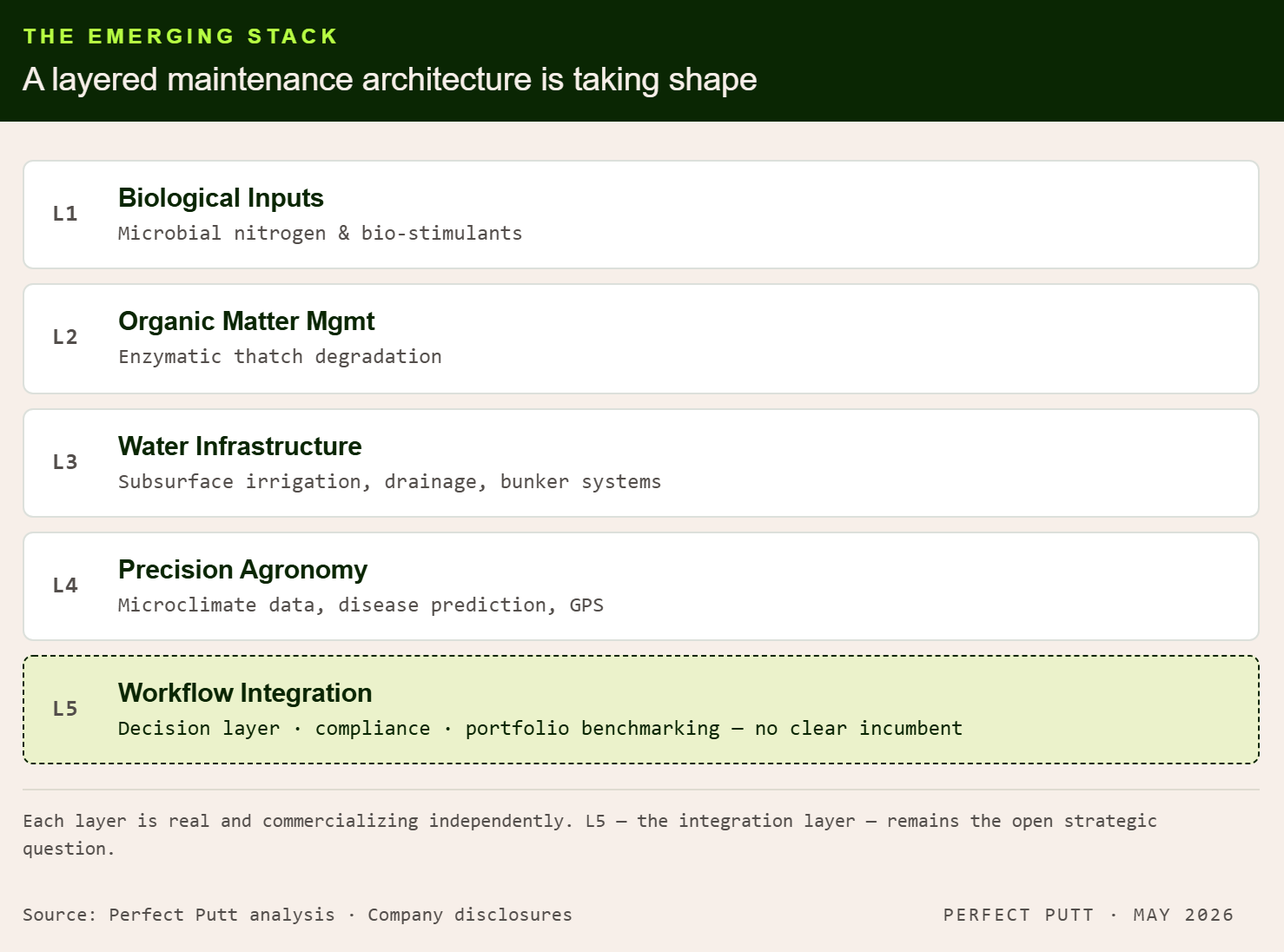

The Emerging Stack

The emerging maintenance model is not a single product or company. It is a layered system, and the businesses building it are arriving from different parts of the value chain. The stack is still early, fragmented, and commercially unproven at golf-industry scale, but the categories are becoming visible. Importantly, many of these companies are not building golf-only businesses. Golf is increasingly serving as a high-performance proving ground where products can be validated under demanding agronomic conditions before expanding into materially larger verticals including agriculture, residential lawn care, municipal landscapes, sports turf, and urban green infrastructure.

Biological Inputs

A new generation of biological input providers is focused on microbial nitrogen fixation, nutrient efficiency, and soil health enhancement. Collectively, these businesses have attracted significant investment and have deployed products across millions of agricultural acres. More recently, several companies have begun developing turf-specific microbial inoculants designed for golf and sports turf applications. These products aim to reduce synthetic nitrogen dependency by supplementing or partially replacing conventional fertilizer programs. Field trial data in agriculture has been encouraging, though golf-specific adoption remains early and performance may vary by soil type, climate, and management regime.

Organic Matter Management

A growing category of biological solutions is focused on improving soil profile quality, surface consistency, and overall turf health through enzyme-based and microbial technologies. These products are generally designed to integrate into existing spray operations without requiring additional equipment, labor, or course closures, allowing superintendents to complement traditional cultural practices with less disruptive maintenance approaches. Beyond turfgrass, many of these platforms are targeting large adjacent markets including residential lawn care and row crop agriculture, materially increasing their long-term market opportunity and commercial scalability.

Water & Subsurface Infrastructure

A new generation of subsurface drainage and moisture-management technologies is gaining traction across golf courses, sports stadiums, training facilities, and urban green spaces. These systems manage water movement throughout the root zone, enabling more precise irrigation and drainage control while reducing overall water consumption. Advanced bunker and drainage infrastructure is also improving course resiliency during extreme weather events and reducing long-term maintenance requirements. As municipalities, developers, and operators increasingly prioritize water efficiency and climate-resilient infrastructure, these technologies have applications that extend well beyond golf and sports turf into substantially larger landscape and urban infrastructure markets.

Precision Agronomy & Data

Emerging agronomic intelligence platforms are combining microclimate modeling, disease prediction, evapotranspiration monitoring, shade analysis, and precision application recommendations into integrated decision-support systems. Many of these solutions are designed to operate without extensive on-site hardware while generating highly localized recommendations across an entire property. Increasingly, these prescriptions can be integrated directly into GPS-enabled application equipment, connecting the data layer to physical execution in real time. If these platforms perform as intended at commercial scale, they could fundamentally change how superintendents allocate labor, water, fertilizer, and chemical inputs across a golf course.

The Capital View

Golf may be one of the most attractive early commercialization markets for precision agronomy and biological turf technology. Playing surface quality has a direct economic link to revenue: better conditions support higher green fees, stronger retention, and more favorable guest reviews. Superintendents are sophisticated technical buyers who test products rigorously and share data across professional networks. Regulatory and cost pressures are tightening simultaneously across labor, water, nitrogen runoff, and chemical use in the coastal and resort markets where premium golf is concentrated. These conditions create a market that is both willing to pay for performance and increasingly motivated to adopt lower-input systems.

For multi-course operators and PE-backed platforms, the economics could compound. A biological or precision program validated at one property could potentially standardize across 10 or 30 with centralized procurement, shared data infrastructure, unified compliance, and more efficient per-course staffing. That would represent operating leverage that fragmented agricultural markets cannot easily replicate. If maintenance-side value creation from lower-input systems proves durable, it could become as significant to platform economics as the revenue-side thesis that has driven golf course consolidation to date.

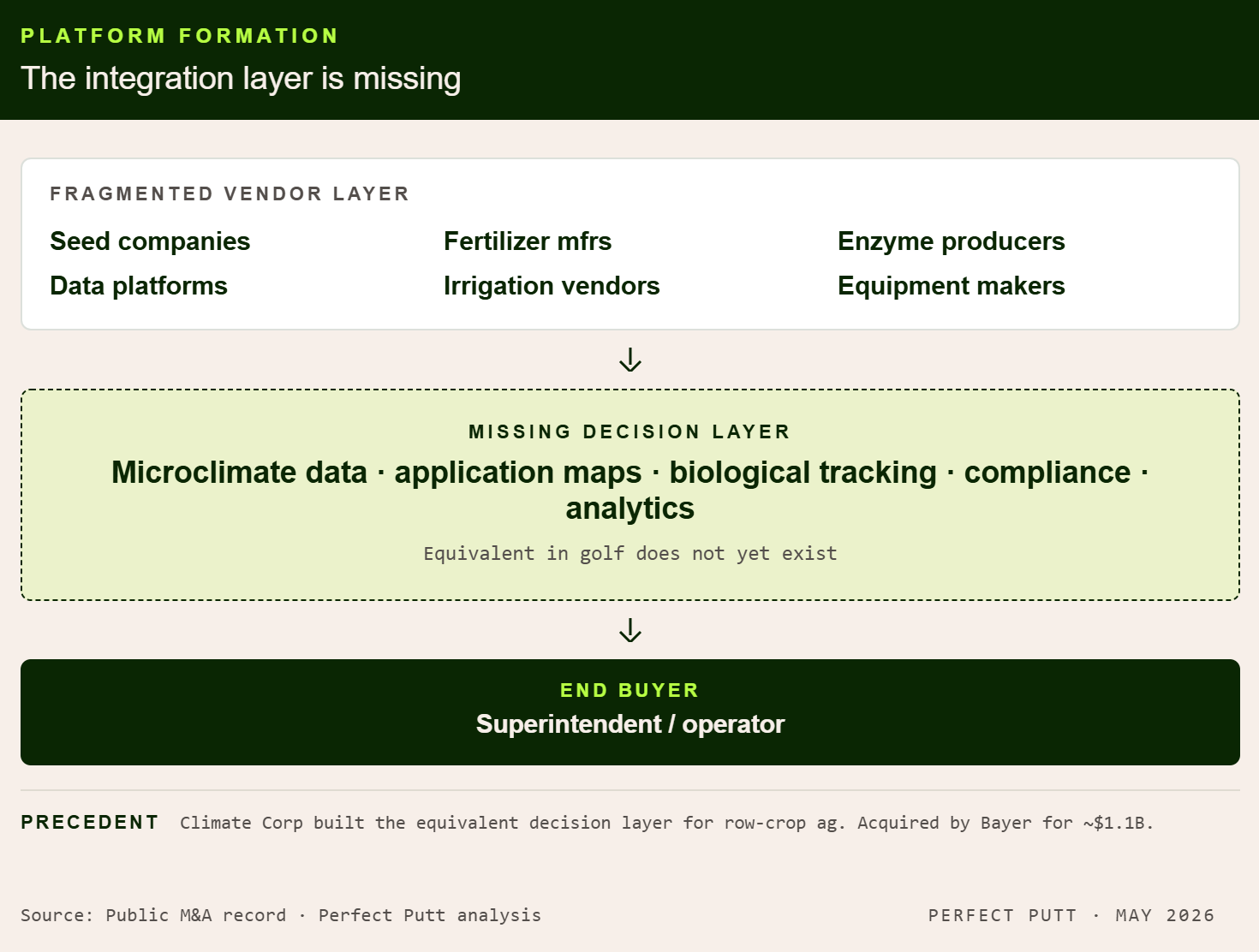

The integration layer remains the open strategic question. Today the market is vertically fragmented. Seed companies, fertilizer manufacturers, enzyme producers, data platforms, irrigation vendors, and equipment makers all sell into the same superintendent through separate channels with no coordination. The precedent worth watching is precision agriculture: Climate Corp built the decision layer above the row-crop supply chain and was acquired by Bayer for approximately $1.1 billion. The equivalent platform in golf, one that ingests microclimate data, generates precision application maps, tracks biological and enzymatic inputs, automates compliance reporting, and produces performance analytics, does not yet exist. Whether it emerges from a data company, an agronomic services provider, or a turf-specific startup remains unclear. But the structural gap is visible.

Future Direction Agronomy & Agriculture

None of this is settled. Many of the technologies discussed in this article are early-commercial, geography-dependent, or still accumulating the multi-season performance data that risk-averse superintendents require before changing established programs. Adoption will likely be uneven, moving faster at well-capitalized private clubs and PE-backed platforms than at municipal courses or small daily-fee operations. Climate, soil type, water availability, and local regulatory environments will all influence which layers of the stack matter most at any given property. The timeline for broad industry adoption, when it arrives, is measured in years and possibly decades, not quarters.

What is visible today is a direction. The category appears to be moving, gradually, from high-input, chemically reactive maintenance toward lower-input, data-informed, biologically assisted systems that have the potential to produce better playing surfaces with less operational intensity. The early movers, courses and platforms that begin integrating biological inputs, precision data, subsurface infrastructure, and enzymatic treatments into their agronomic programs, may build structural advantages in surface quality, cost efficiency, and operating consistency that are difficult to replicate once established.

The operating blueprint is still being written. But for operators, superintendents, and investors watching the next decade of golf infrastructure, the question is no longer whether these tools exist. It is how quickly they mature, how effectively they integrate, and which organizations are positioned to capture the advantage when they do.

The best way to support Perfect Putt is to share it with a friend.