The Economics of U.S. Golf Courses

Sweetens Cove evolved from a modest former golf property in rural Tennessee. Sand Valley emerged from central Wisconsin sand barrens long overlooked by developers. Bandon Dunes sat on a remote stretch of the Oregon coast far from traditional golf demand. None appeared conventionally investable. The insight was recognizing that exceptional land, paired with differentiated golf experiences, could create its own demand curve, pricing power, and brand gravity independent of geography.

At the same time, thousands of municipal and daily-fee courses operate with deferred maintenance and recurring taxpayer support. The celebrated properties and the struggling ones share the same underlying truth: in golf, economics follow product. That matters because golf in America is not one business. It is roughly 16,000 courses operating across five distinct economic models, each with different capital requirements, margin structures, and return profiles.

This piece examines where capital works in modern golf and the three ways investors deploy it: buy, build, or transform.

Welcome to Perfect Putt, a newsletter covering the business and economics of the golf industry. If this was forwarded to you, subscribe to join 11,000+ readers who follow how capital flows through golf.

Read Time: 8 Minutes

The Landscape

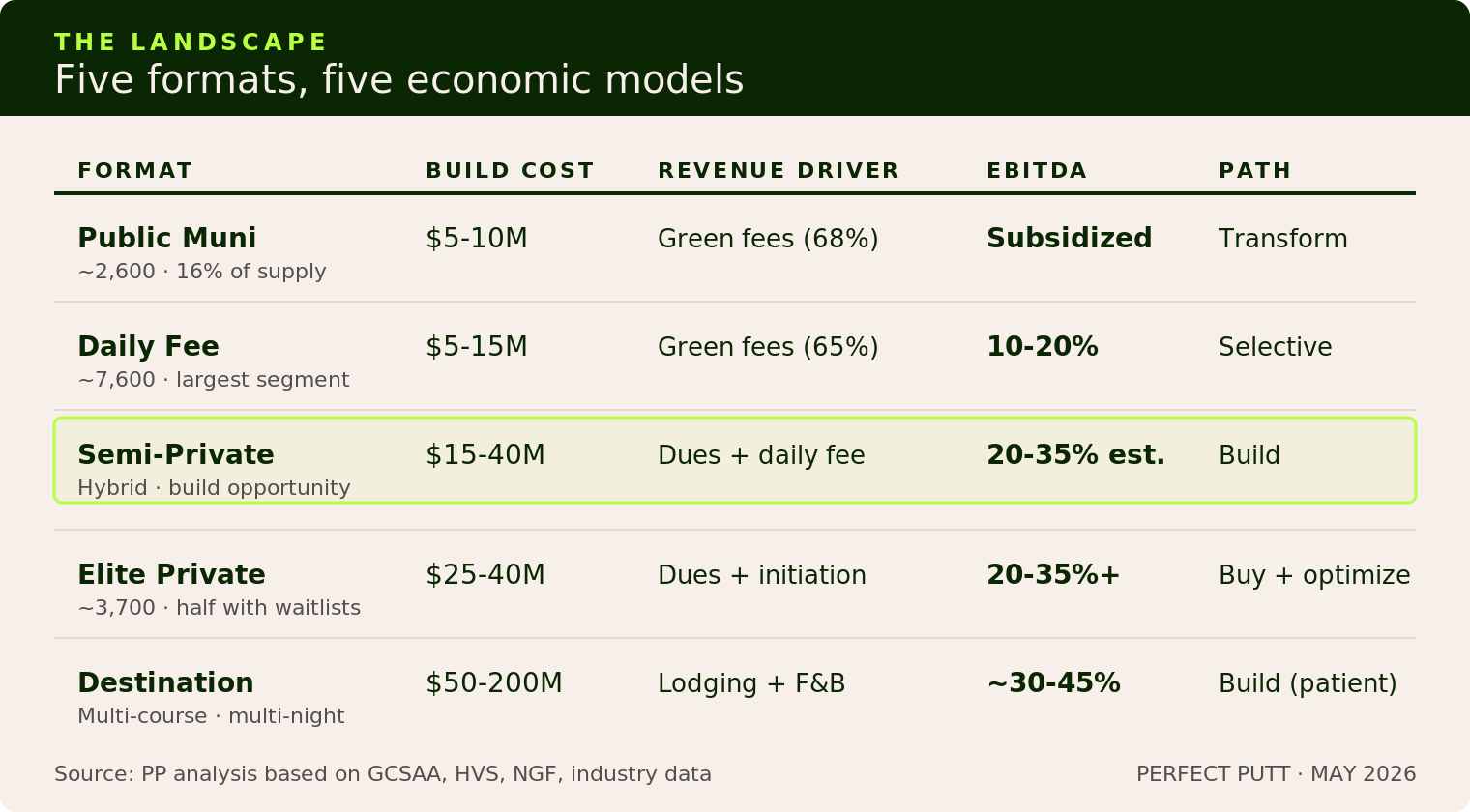

Before allocating capital, you need to understand the asset classes. Golf in America is not one industry. It is five distinct operating models with different revenue streams, margin structures, and levels of pricing power. Fewer than 20 new courses are built annually on average. Supply remains constrained while demand holds. The question is which formats convert that imbalance into durable cash flow.

Public municipal. About 2,600 courses, or 16% of supply. These are participation assets, not financial assets. Most lose money. Of 221 municipalities surveyed by HVS, 155 required taxpayer subsidies totaling $61 million. Returns here are social, not economic.

Daily fee. Roughly 7,600 facilities and the most operationally pressured segment in golf. EBITDA margins typically range from 10–20%, compressed by rising labor, water inflation, and limited pricing power against nearby substitutes. Construction costs run $5–15 million per 18 holes before land.

Semi-private. The most structurally attractive greenfield format in golf. Membership dues create recurring revenue while public play monetizes excess demand and lifts yield per round. Presold memberships can partially finance development, reducing upfront equity requirements. Premium semi-private supply remains limited nationally. That scarcity is the opportunity.

Elite private. About 3,700 clubs and the segment with the strongest repricing power since the pandemic. Median initiation fees rose from roughly $29,000 in 2019 to $50,000 by 2022 and continue climbing. Dues and initiation fees generate 55–60% of revenue, creating highly durable recurring cash flow. Waitlists remain widespread across private clubs.

Destination resort. The highest-revenue and most capital-intensive format. Multi-course properties monetize not just golf, but lodging, dining, retail, and wellness. Green fees become a minority of guest spend. Development costs range from $50–200 million with stabilization timelines measured in decades, not seasons.

Five formats. Three capital paths. The question is which model fits your capital base, risk tolerance, and time horizon.

Buy: Validating PE

The best risk-adjusted returns in golf are not coming from new construction. They are coming from acquiring existing private clubs and operating them more effectively.

The transaction history is clear. KSL Capital acquired ClubCorp in 2006 for $1.8 billion and took it public in 2013. Apollo acquired it in 2017 for $2.2 billion. KSL agreed to reacquire the business in 2026 for roughly $3 billion. Different owners, same conclusion: private clubs respond exceptionally well to professional management and strategic reinvestment.

The economics explain why. Recurring dues revenue with 90%+ retention creates unusually durable cash flow for a leisure asset. Affluent members spend more as the product improves. Amenity investment drives incremental margin with limited incremental fixed cost. Well-run platforms generate EBITDA margins in the low-to-mid 20s.

The playbook repeats across scaled operators: acquire at a reasonable multiple, invest in the asset, reprice the membership base, and allow EBITDA growth to compress the effective entry multiple over time. Clearlake doubled both revenue and profitability at Concert Golf Partners before selling the platform to Bain Capital at approximately $1.3 billion.

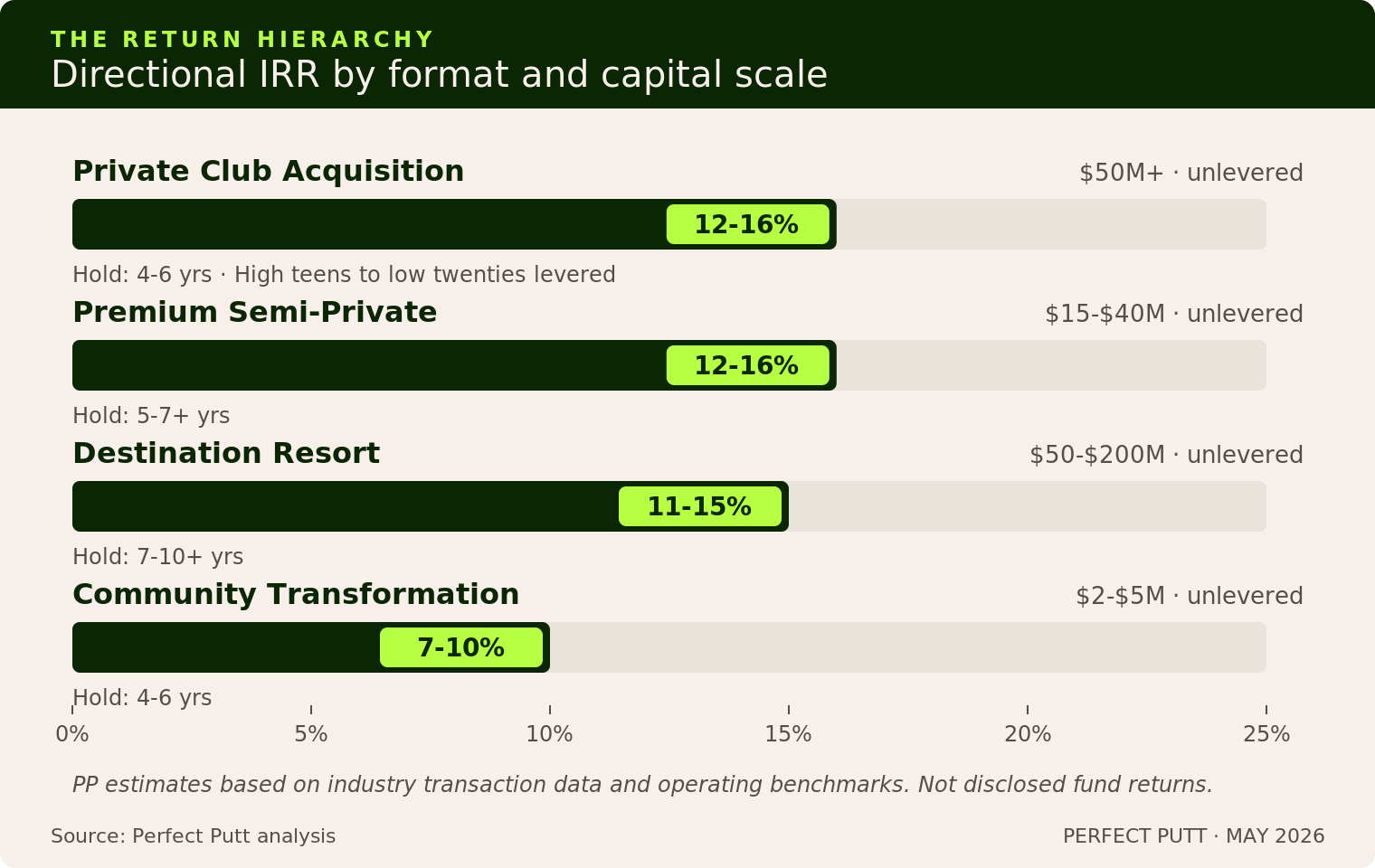

For investors with $50 million+ and a 3–5 year horizon, this is the most institutionally proven model in golf.

Build: Manufacturing Scarcity

Not every allocator can acquire a scaled private-club platform, and not every market offers one worth buying. For $15–40 million, the opportunity is building differentiated semi-private clubs in secondary markets within driving distance of major metros.

The economics begin with basis. Rural acreage trades at $5,000–15,000 per acre versus $50,000+ in suburban corridors. Membership dues provide recurring revenue visibility while premium daily-fee play captures upside demand. The model works because differentiated golf experiences face limited local competition.

The best projects create scarcity through product rather than exclusivity alone. Strong land, compelling design, and limited regional substitutes support premium pricing without resort-scale infrastructure. F&B, events, and modest lodging add incremental margin without materially increasing capital intensity.

The geography already signals where capital is moving. Florida, South Carolina, and Texas account for roughly 35% of active U.S. golf development projects. About 60% of new builds are private. Very few are premium semi-private. That supply gap is the opening.

But the economics only work if the product justifies pricing power. And in golf, the product starts with the land.

Land, Product, Brand, Returns

Every nationally relevant new-build course shares one characteristic: exceptional terrain. Sand, dunes, elevation, native grasses, coastal exposure. The land sets the ceiling on the experience and, ultimately, the economics.

Developers who understand this spend years sourcing sites before spending meaningfully on design. Once the land is right, differentiated product drives the rest of the model: premium pricing, organic demand generation, repeat visitation, and membership presales.

The customer is not simply buying golf. They are buying distinctiveness. Courses that feel interchangeable compete on price. Courses that feel singular develop pricing power.

That dynamic is playing out across the country. Sweetens Cove on Tennessee farmland. Gamble Sands in rural Washington. Landmand in Nebraska. Broomsedge in the Carolina Sandhills. Different geographies, same pattern: differentiated experience creates brand equity, and brand equity creates economic leverage.

The sequence matters. Land creates product. Product creates brand. Brand creates pricing power.

The Destination Ceiling

For investors with $100 million+ and a decade-long horizon, destination resort golf offers the highest absolute return ceiling in the sport.

Bandon Dunes generates upward of $125 million annually across golf, lodging, dining, retail, and caddie operations. The golf course is not the business. It is the demand engine for a vertically integrated hospitality platform.

That model dramatically expands revenue per guest. A four-day destination trip can exceed $4,000 per golfer once lodging, food and beverage, caddies, and ancillary spend are included.

The tradeoff is execution risk and capital intensity. Development costs range from $50–200 million with stabilization periods often exceeding seven years. Success requires expertise across hospitality, operations, development, branding, and course architecture simultaneously.

Very few operators can execute at that level. Dream Golf and Cabot have proven they can. Most groups cannot.

Transformation: Basis Arbitrage at Scale

The third opportunity requires the least capital and reaches the broadest customer base.

Municipal and daily-fee courses account for most of America’s 540 million annual rounds, yet many operate with aging infrastructure, deferred maintenance, and poor revenue management. The opportunity is not ground-up development. It is operational transformation at low basis.

Targeted investments of $2–5 million into irrigation, conditions, clubhouse upgrades, and pricing systems can materially improve both utilization and profitability. Public-private partnerships and management contracts further reduce capital exposure.

The returns are smaller than private-club acquisitions or destination development, but the risk profile is materially lower. More importantly, the customer base is vastly larger.

The same principle applies here as everywhere else in golf: improved product drives improved economics. Better conditions, better hospitality, and better experience translate directly into stronger retention, higher utilization, and greater pricing flexibility.

Product First, Then Capital

Three paths. One requirement.

Private-club acquisitions can generate levered IRRs in the high teens to low twenties over 4–6 years. Premium semi-private development targets unlevered mid-teens over 5–7+ years, aided by membership presales and lower land basis. Destination resorts target low-to-mid teens unlevered over longer hold periods with significantly higher capital requirements. Community transformations generate lower but steadier cash yields with reduced downside risk.

The formats differ. The underwriting principle does not.

Golf is ultimately a pricing-power business built on differentiated experience and constrained supply. Capital can amplify a strong product. It cannot rescue a weak one.

The best golf assets are not simply courses. They are recurring cash flow businesses built on scarcity, loyalty, and experiences competitors cannot easily replicate.

The best way to support Perfect Putt is to share it with a friend.