Golf's Water Reckoning

Water is repricing faster than golf revenue is growing. Courses that deploy the full agronomy technology stack now will build a compounding cost advantage over those that wait.

Welcome to Perfect Putt, a twice-weekly newsletter covering the business and economics of the golf industry. If this was forwarded to you, subscribe below to join 12,000+ readers who follow how capital flows through golf.

Read Time: 8 Minutes

The Macro Picture: Water Is Repricing Everywhere

Golf's water challenge is a local expression of a global repricing event. U.S. household water costs are projected to more than double by 2050 in constant dollars. The Colorado River system sat at 37% of storage capacity as of early 2026, and the winter of 2025-2026 made it worse: eight Western states set record-low snowpack, with a majority of Colorado River Basin forecast points now expecting less than 30% of average runoff. Golf sits squarely in the path of these forces, concentrated in the geographies where water stress is most acute. Broad green fairways in a brown landscape make courses visible targets for regulators and public opinion in ways that far larger water consumers are not.

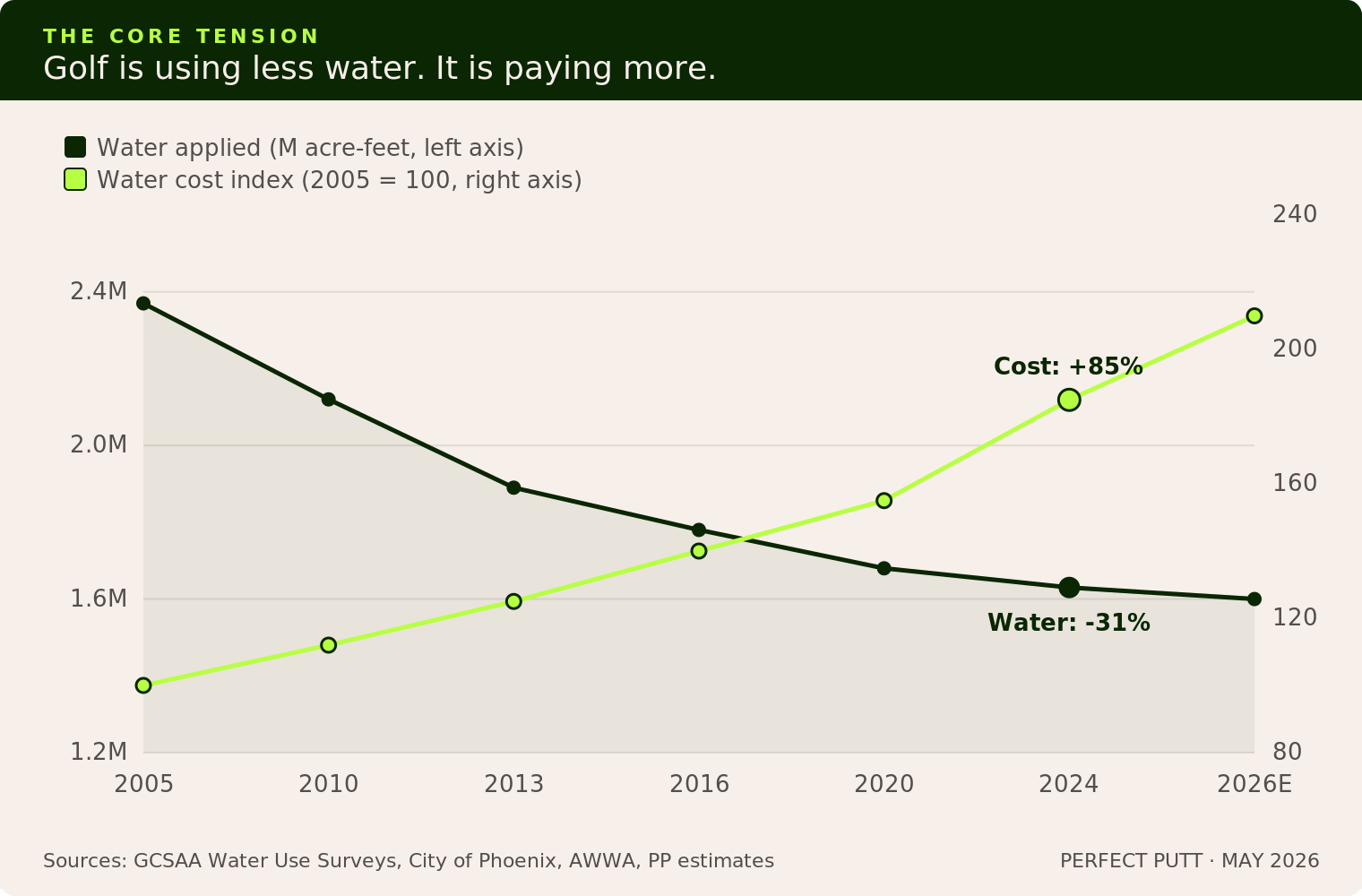

The U.S. golf industry applied 1.63 million acre-feet of water in 2024, enough to supply roughly 4.9 million American households for a year. That figure represents a 31% reduction from 2005 levels. The industry deserves credit. But the reduction is not the story. The story is cost. In Phoenix, municipal water rates have risen 48% since 2022. In Las Vegas, golf course water budgets were cut by more than a third overnight. Water has been golf's cheapest input for a century. In the markets where the game is growing fastest, that era is ending.

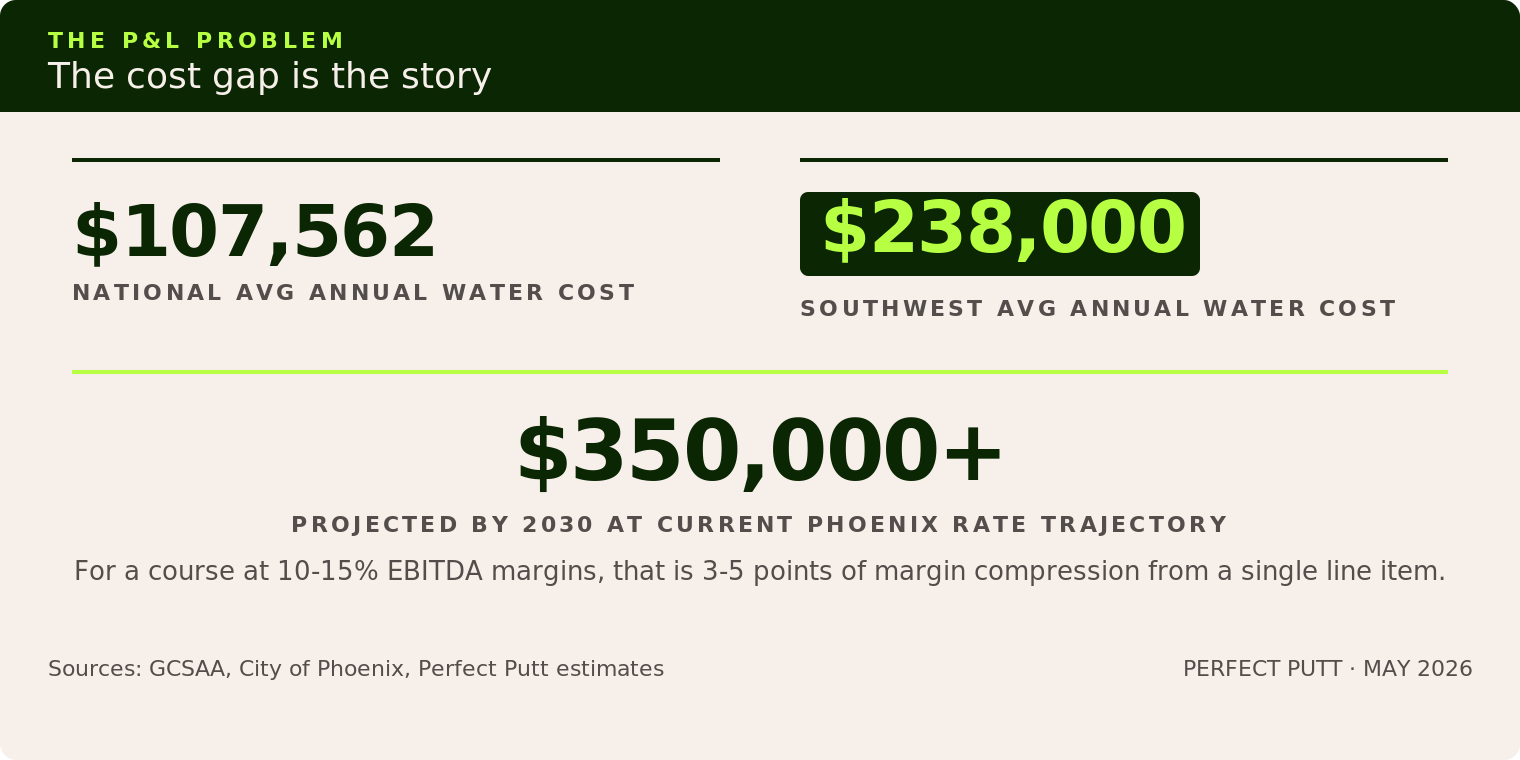

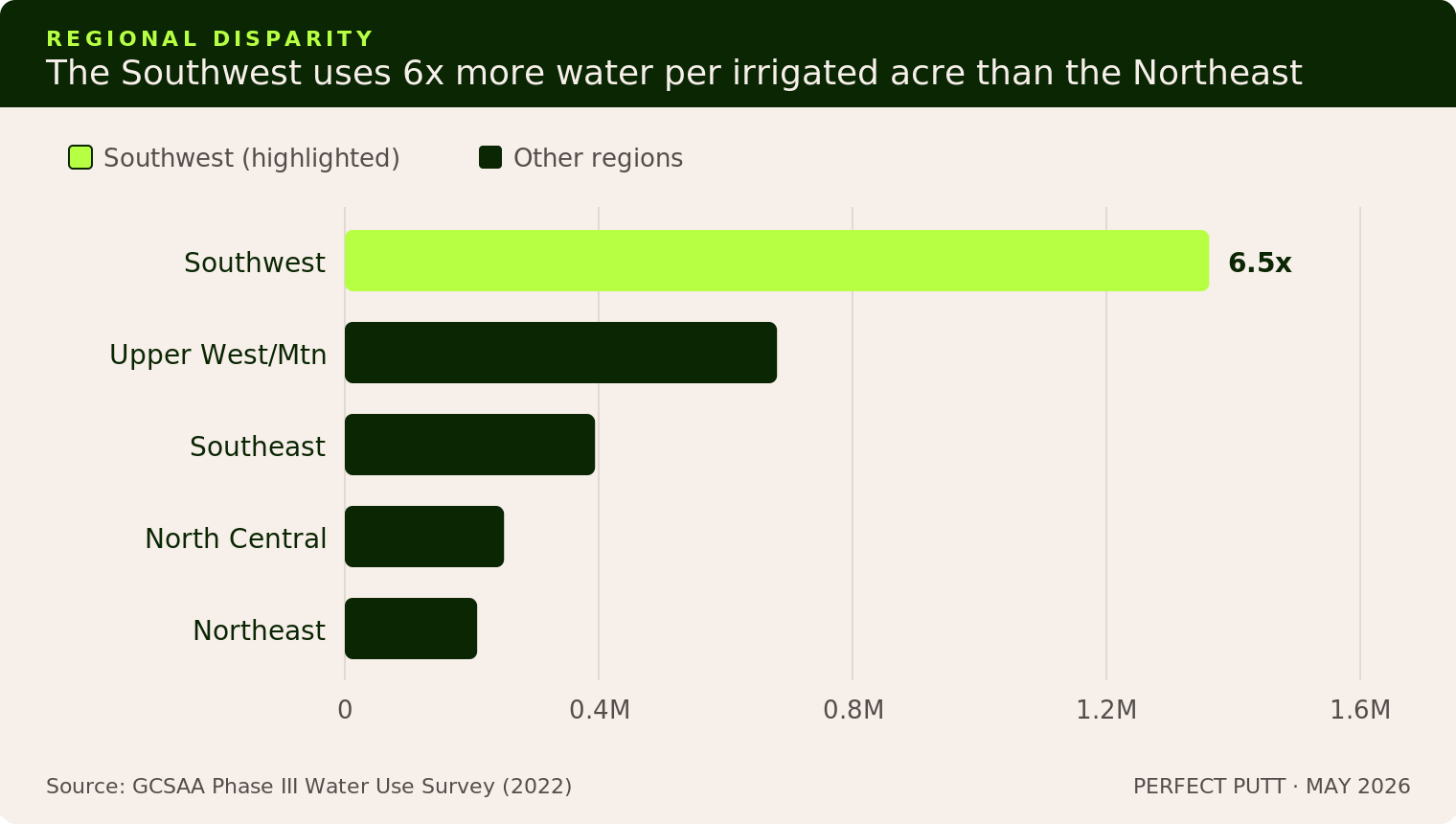

The usage gap is dramatic: a Southwest course applies more than 1.3 million gallons per irrigated acre annually, roughly six times more than a Northeast facility at 208,000 gallons. The cost gap is even wider. Courses that purchase water in the Southwest spend an average of $238,000 annually on irrigation, more than double the national average of $107,562. The Southwest is the only region where water application per acre has increased since 2005, rising 21.9% even as every other region declined.

What Golf Actually Uses

The most comprehensive industry water audit, released in late 2025, tells the efficiency story. Total application fell from 2.37 million acre-feet in 2005 to 1.63 million in 2024. Two-thirds of that reduction came from efficiency gains. Irrigated acreage also declined 11.5%, from 1.18 million acres to 1.04 million, driven by closures and operators actively shrinking their footprint.

Golf accounts for approximately 0.5% of total daily U.S. water withdrawals. In Arizona, golf uses roughly 2% of the state's water yet generates an estimated $6 billion in economic impact and 66,000 jobs. Green Section programs are estimated to save U.S. courses more than $1.9 billion annually in reduced inputs. The water is not wasted. But that argument does not change the cost curve. When water costs rise 10-15% annually in your market, a two-decade efficiency gain does not keep you ahead of the curve. It keeps you running in place.

For the roughly one-quarter of U.S. golf courses that purchase water, irrigation represents approximately 13% of total maintenance budget. If municipal rates in the southwest continue to rise at their current trajectory, a course paying $238,000 in 2024 will face $350,000 or more by 2030. For a daily-fee course generating $3 to $4 million in total revenue, that is a 3-4% compression from a single line item. For a course already operating at 10-15% EBITDA margins, that is the difference between viability and distress.

The Regulatory Squeeze

The cost curve alone would force change. Regulators are not waiting.

Las Vegas is the clearest example. In January 2023, the Las Vegas Valley Water District approved a reduction in golf course water budgets from 6.3 acre-feet per irrigated acre per year to 4.0 acre-feet, effective 2024. That is a 37% cut. Water consumed in excess of the budget incurs surcharges. Since 1999, 30 Las Vegas-area golf courses have collectively removed more than 900 acres of maintained turf.

The pattern is repeating across the West. Nevada enacted legislation in 2021 prohibiting Colorado River water for non-functional grass starting in 2027. Arizona's Groundwater Management Act caps new course allotments within Active Management Areas, though courses using 100% reclaimed water are exempt. California's AB 1572, effective January 2024, bans potable water on non-functional commercial turf; golf was explicitly exempted as functional turf, but the political trajectory is clear. When regulators begin classifying turf by function, the question is not whether golf faces scrutiny, but when the exemptions narrow.

The operational consequences are already visible. Roddy Ranch Golf Club in California closed in 2016 after just 16 years, citing $500,000 to $600,000 in annual water bills. In Phoenix, Moon Valley and Lookout Mountain invested $9.5 million in a canal water pipeline to switch off potable supply entirely.

The Full Sustainability Stack

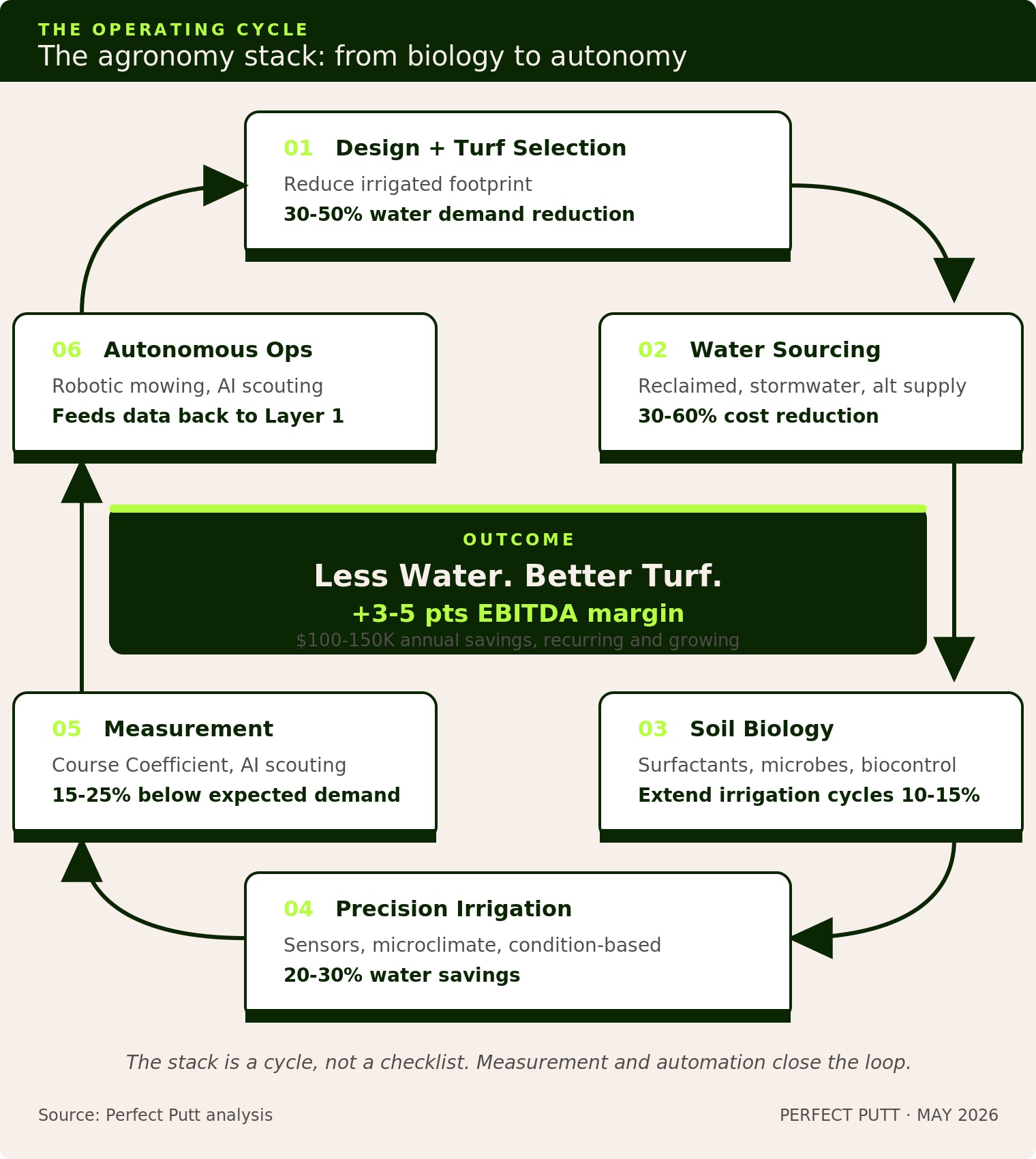

For most of the sport's history, water management meant turning on the irrigation system, running it on a schedule, and adjusting when something looked wrong. That model worked when water was cheap and regulations were loose. What is replacing it is a full sustainability stack: an integrated system of design, sourcing, soil science, precision technology, measurement, and automated operations. No single layer solves the water problem. Stacking all six is what changes the operating economics.

Layer 1: Design and turf selection. Drought-tolerant grass species, reduced irrigated acreage, native vegetation in out-of-play areas. Pinehurst No. 2's turf reduction contributed to a 50% water savings. Industry data shows 86% of golfers are receptive to the resulting changes in course appearance. The cheapest gallon of water is the one you never need to apply.

Layer 2: Water sourcing. Reclaimed water, on-site storage, stormwater capture, alternative supply contracts. Only 12% of U.S. courses irrigate with recycled water nationally, though in the Southwest, 34% of applied water comes from recycled sources. Reclaimed water is typically 30-60% cheaper than potable. For a Southwest course spending $238,000 annually on irrigation, switching to reclaimed supply could reduce that line item by $70,000 to $140,000. Infrastructure costs remain the barrier.

Layer 3: Soil biology and chemistry. The largest conceptual shift in course water management is treating irrigation as a biology problem rather than a volume problem, the same principle driving precision biologics across commercial agriculture. Companies like Aquatrols and Holganix engineer soil surfactants and microbial platforms that improve water penetration and root-zone resilience, stretching irrigation cycles. Locus Fermentation Solutions manufactures biosurfactants that document third-party gains in turf stress recovery. Novonesis brings enzyme-based biocontrol to turf through Actinovate SP, an OMRI-listed biological fungicide already standard in row-crop agriculture. The combined effect of this layer is that healthier soil and more efficient plant biology mean less water per unit of turf quality. For a course running $238,000 in annual water costs, even a 10-15% reduction in irrigation frequency from improved soil retention represents $25,000 to $35,000 in annual savings on a line item that is compounding against you.

Layer 4: Precision irrigation and microclimate intelligence. Schedule-based irrigation is the single largest source of water waste on most courses. Toro's Lynx Central Control and Rain Bird's CirrusPRO deliver condition-based watering with documented savings of 20 to 30%. TerraRad is pushing deeper: its turfRad system uses passive microwave sensors that mount on standard mowing equipment to measure root-zone moisture during routine passes, applying the same L-band technology used in agricultural satellite systems at turf scale. Toro was the first to integrate the data, building it into Lynx as its Spatial Adjust software in 2025, but the sensors are equipment-agnostic. Second Sun, a Danish company, attacks the problem from the atmosphere, providing real-time evapotranspiration data at the meter scale via satellite and integrating with John Deere's Operations Center. For a Southwest course, a 25% reduction in water application translates to roughly $60,000 in annual savings at current rates, and that number grows every year the rate escalates.

Layer 5: Measurement and autonomous scouting. The Course Coefficient compares actual water use to estimated demand based on evapotranspiration. Well-managed Southwest courses are achieving coefficients of 0.75 to 0.85, operating 15 to 25% below expected demand. You cannot optimize what you cannot quantify. GreenPulse, a Netherlands-based company, is closing that measurement gap at the turf surface with an autonomous robot that scans greens overnight and uses AI to detect disease like Dollar Spot one to two days before visible symptoms emerge. Early detection means targeted intervention rather than blanket application, reducing both chemical inputs and the irrigation adjustments that follow turf damage.

Layer 6: Autonomous operations. Husqvarna's CEORA platform is bringing autonomous mowing to professional turf at scale. The value is not just labor savings. It is what automation frees the maintenance team to focus on: soil moisture maps, irrigation prescriptions, optimizing the entire system.

None of this is cheap upfront. But each layer reduces a recurring cost that is rising faster than revenue. A course that invests $500,000 in precision irrigation and turf conversion today may save $75,000 to $100,000 annually in water and chemical costs, with the gap widening every year as municipal rates escalate. The upfront capital is a fixed cost. The savings are a growing annuity.

Five years ago, the sustainability stack was disconnected products. What is forming now is the same convergence of biologics, sensor data, and autonomous operations that reshaped row-crop agriculture over the past decade. Golf is a smaller addressable market, but the underlying technologies are shared. The companies building each layer of the turf stack are drawing from the same science, the same engineering talent, and increasingly the same distribution partnerships as their agricultural counterparts.

Innovation Today, Table Stakes Tomorrow

Within a decade, the full stack will be the minimum. Tightening water allocations, rising municipal rates, construction permitting tied to water efficiency, and growing scrutiny from regulators will make it not a competitive advantage but a condition of doing business. The courses and developers who build the full stack today will define the standard that everyone else is eventually forced to meet.

For operators, the implication is clear: invest before the cost curve forces your hand. Know your Course Coefficient. Model your water cost trajectory. Stack the interventions. For investors underwriting golf course assets, water access, source diversity, soil health infrastructure, and technology adoption are not amenities. They are valuation variables. A Southwest course at a 7x EBITDA multiple implicitly assumes water costs grow at or below revenue. If water is compounding at 10-15% while green fees grow at 3-5%, that multiple is mispriced.

The sport has reduced water use 31% over two decades. The next reduction will not come from incremental best practices. It will come from operators who build the full stack, measure relentlessly, and treat water efficiency not as an environmental initiative but as a core operating discipline. The ones who move first will not just survive the repricing. They will define what a well-run golf course looks like for the next generation.

The best way to support Perfect Putt is to share it with a friend.