The $6 Billion Experiment: What LIV Golf Is Worth Without PIF

Saudi Arabia's Public Investment Fund confirmed on April 29 that it will end its financial backing of LIV Golf at the conclusion of the 2026 season. Two days later, LIV announced the formation of a new independent board led by a pair of turnaround specialists. The sequence tells you everything.

PIF has spent an estimated $5.3 billion on LIV Golf since 2022, with total outlays projected to exceed $6 billion by season's end. What it purchased was attention, not an economic franchise. What it leaves behind is a league generating real but insufficient revenue, carrying depreciating player contracts, marketing unvalidated franchise equity, and now governed by restructuring professionals. The question is no longer whether LIV survives. It is what a rational capital allocator would pay for what remains.

Welcome to Perfect Putt, a twice-weekly newsletter covering the business and economics of the golf industry. If this was forwarded to you, subscribe to join 11,000+ readers who follow how capital flows through golf.

Read Time: 9 Minutes

What $6 Billion Bought

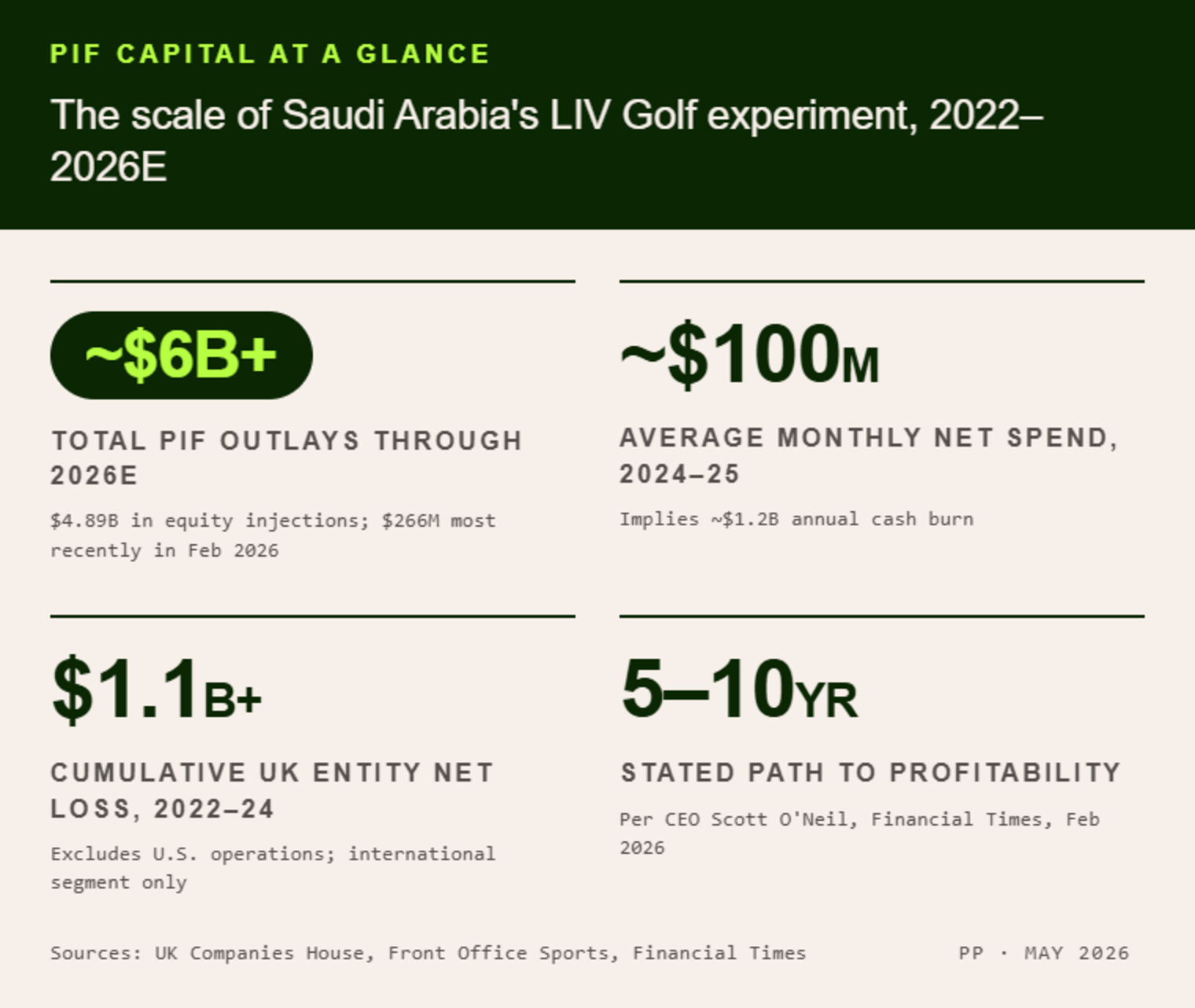

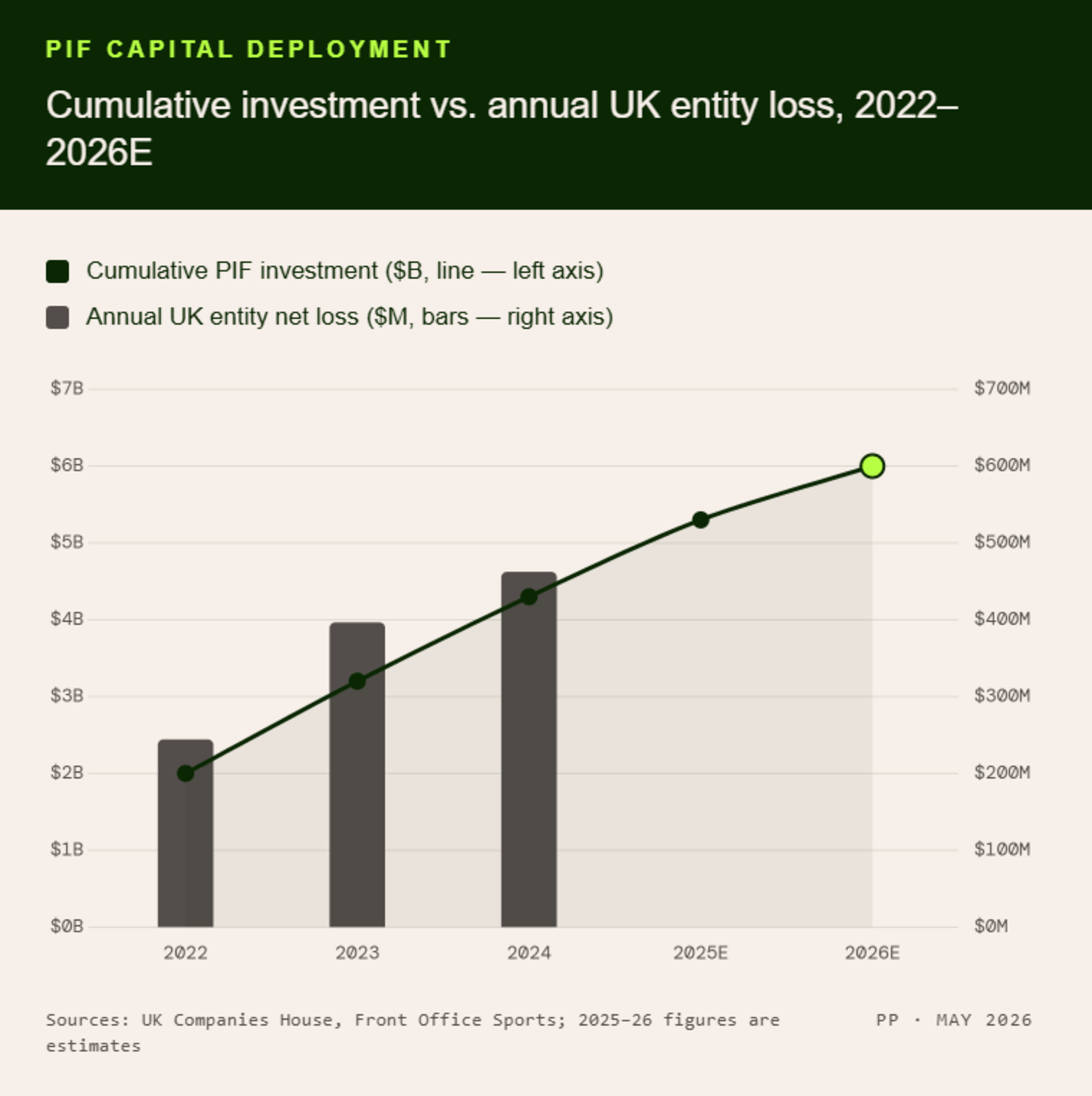

The scale of PIF's commitment to LIV Golf has no precedent in professional sports. Since LIV's official launch in 2022, PIF has purchased approximately $4.89 billion in ordinary and non-voting shares of LIV Golf Investments, per UK Companies House filings. A $266.6 million capital injection was approved as recently as February 2026. At the current burn rate, total outlays will surpass $6 billion by the time the final 2026 event is played.

The losses have been staggering. LIV Golf Ltd., the UK-based entity that operates LIV's non-U.S. business, reported losses of $243.7 million in 2022, $395.9 million in 2023, and $461.8 million in 2024. That is more than $1.1 billion in cumulative international losses alone, before accounting for U.S. operations. The league's net spend has averaged approximately $100 million per month across 2024 and 2025, according to Front Office Sports. CEO Scott O'Neil told the Financial Times in February that profitability was five to ten years away.

PIF's decision is not political. It is arithmetic. The fund's spokesperson stated that "the substantial investment required is no longer consistent" with PIF's investment strategy. When one of the world's largest sovereign wealth funds concludes that the incremental dollar into a sports property offers negative expected return, the signal is unambiguous.

The Rival League Playbook

The history of rival professional sports leagues is well-documented, and the pattern is unambiguous. The leagues that succeeded (the American Football League in the 1960s, the American Basketball Association in the 1970s) built independent economic value before forcing a merger from a position of strength. The AFL secured a five-year, $36 million television contract with NBC in 1965 that gave it both revenue and credibility. Art Modell, then the owner of the Cleveland Browns, later said: "The money is one thing, but credibility is more important. When NBC signed them, I knew they were for real." The ABA created a differentiated product (the three-point line, the slam-dunk contest) and built fan bases in underserved markets. Both leagues made the economic case for merger. The incumbent had to absorb them because they were generating independent value that could not be ignored.

The leagues that failed (the USFL, the original XFL, the World Football League) inverted the sequence. They led with player spending, assumed media value would follow talent, and collapsed when the capital source exhausted its patience. The USFL lost over $163 million (roughly $390 million in today's dollars) across three seasons. It signed Herschel Walker, Steve Young, and Jim Kelly. It had an ABC television deal. But ownership factions pushed the league from its differentiated spring schedule into a direct fall competition with the NFL, abandoning the only strategic position that gave it room to build. It won an antitrust lawsuit against the NFL and was awarded $3. Then it ceased to exist.

LIV Golf followed the failure playbook at a scale that dwarfs every prior example. The strategic error was not spending $6 billion. The error was spending $6 billion on talent acquisition without first building the distribution infrastructure (specifically, a domestic media rights deal) that converts talent into enterprise value. Every dollar of player guarantees was a cost without a corresponding revenue asset to amortize against. The AFL spent to compete, but NBC's television money funded the competition. LIV spent to disrupt, but no broadcaster funded the disruption. PIF funded it alone. And when a single capital source underwrites the entire cost structure of a professional sports league without requiring a return on that capital, the business never develops the discipline to generate one. The cost structure is never pressure-tested. The pricing model is never market-validated. And when that single source withdraws, there is no independent economic engine to sustain operations. That is not a business failure. It is a capital allocation failure, the most expensive one in the history of professional sports.

The Revenue Reality

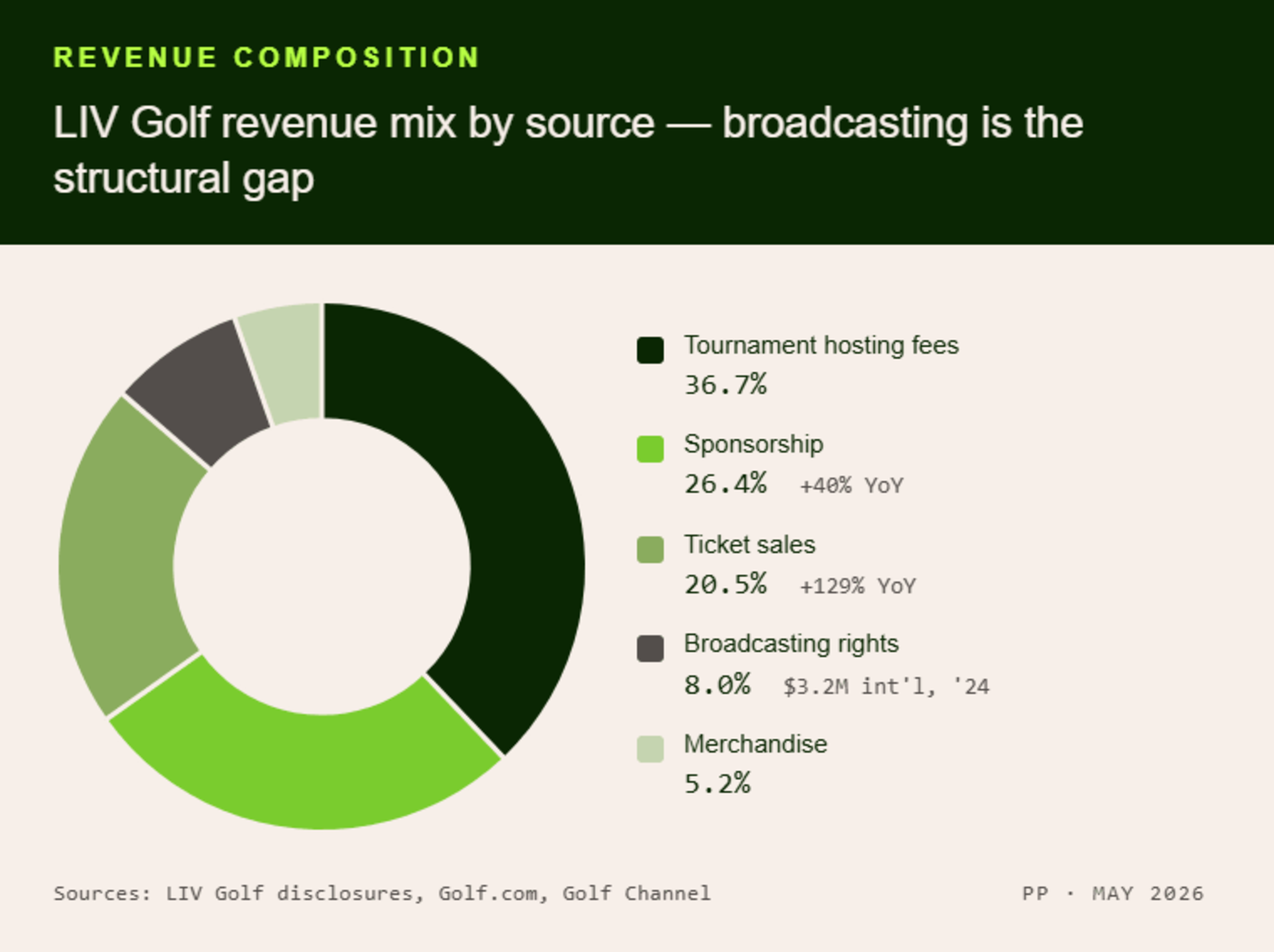

To its credit, LIV Golf has built a real revenue base. Revenue more than doubled from 2024 to 2025, per the league's own disclosures, and 2026 is tracking approximately $100 million ahead of the prior year. The league has secured $500 million in multi-year sponsorship commitments. Ticket sales are up 129% year-over-year and VIP hospitality sales are up 67%. Sponsorship income has increased 40% year-over-year through the first half of 2026.

The problem is the denominator. LIV's revenue mix, based on available disclosures, skews heavily toward tournament hosting fees (36.7% of total revenue) and sponsorship (26.4%), with ticket sales at 20.5%, broadcasting rights at just 8%, and merchandise at 5.2%. The media rights figure is the structural problem. LIV's UK entity generated only $3.2 million in international media rights revenue in 2024. Without a scaled media rights deal (the single asset that underwrites franchise value in every major professional sports league), the revenue base cannot close the gap against a cost structure that, based on the ~$100 million monthly net spend reported by Front Office Sports, has been running at roughly $1.2 billion annually.

Revenue growth is real. Revenue sufficiency is not. The trajectory is encouraging in isolation, but a business that generates a few hundred million in annual revenue against a billion-plus in annual costs is not approaching break-even. It is approaching a different question: what does this business look like at a cost structure the revenue can actually support?

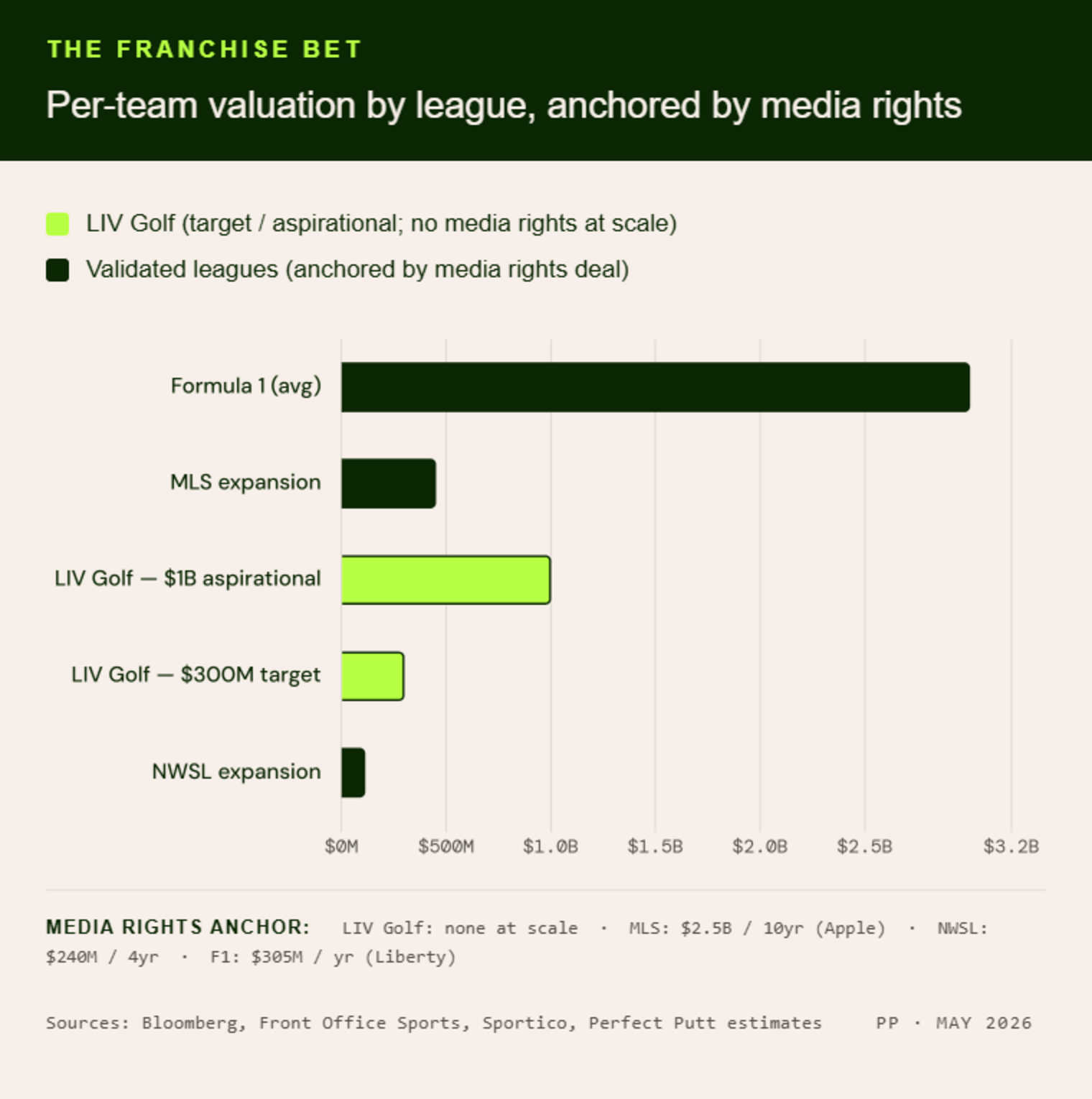

The Franchise Bet

Scott O'Neil's strategic thesis for LIV was never about tournament revenue. It was about franchise equity. "The essence of the return on this business will come through the equity on our teams," O'Neil told Fortune. The aspiration: 13 franchises, each worth $1 billion, with player-captains owning 25% and LIV retaining 75%. O'Neil invoked the Utah Jazz (purchased for $13 million, recently sold for just under $2 billion) as the precedent for what patient capital could build.

In January, LIV hired Citigroup to run a process selling minority stakes in two teams at an implied valuation of $300 million each, with a full control sale of one team also under consideration. As of May, no stakes have been sold. The reason is structural. Franchise valuations in professional sports are anchored by media rights, which create predictable, escalating, long-duration cash flows that underwrite leveraged acquisitions. LIV has no scaled media rights deal. It has no domestic linear television agreement. Its international media rights generated $3.2 million in 2024. Without the media rights anchor, a $300 million team valuation implies a buyer is purchasing brand equity, a roster of aging athletes, and optionality on a league that may not exist in 18 months.

Compare that to leagues where franchise equity has been validated. MLS expansion fees sit at $400-500 million, backed by a ten-year, $2.5 billion Apple TV media rights deal. NWSL expansion fees have reached $110-115 million on the back of a four-year, $240 million ESPN/CBS/Amazon deal signed in 2024. Even F1 team valuations (the closest structural analogue to LIV's team-based model) are supported by a $305 million annual Liberty Media rights package and robust hosting fee economics. In each case, the media rights deal came first. The franchise valuation followed. LIV attempted to build franchise value before securing the media rights that would justify it.

The Talent Cliff

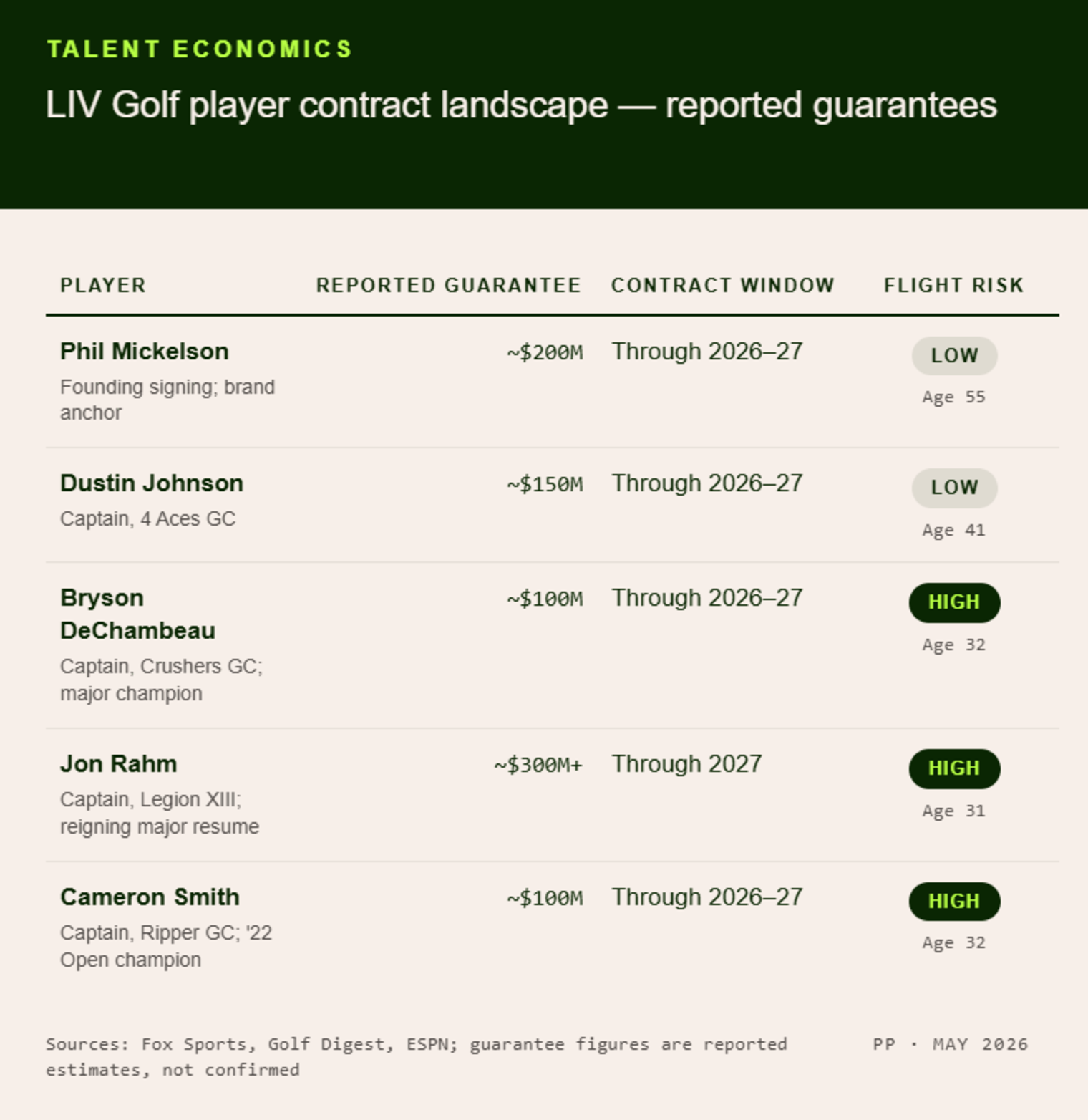

LIV's only irreplaceable asset is its player roster. The signing bonuses (reportedly $200 million for Phil Mickelson, $150 million for Dustin Johnson, $100 million for Bryson DeChambeau, per Fox Sports and Golf Digest) were the capital expenditure that created the league's market position. Top players received half of their guarantees upfront, with the balance paid in annual installments across three-to-five-year deals, according to Golf Digest reporting on contract structures. The longest contracts extend through the 2027 season.

Two dynamics are now working against LIV simultaneously. First, the guarantee structure is shifting. LIV has already informed players that contract renewals will not include the large upfront payments that characterized initial signings. Future compensation moves toward a performance-based model, which eliminates the primary economic incentive that differentiated LIV from the PGA Tour. Second, players are exploring alternatives. Multiple representatives for LIV members have reached out to the PGA Tour about return pathways, per Golf Digest. The Tour's Returning Member Program, a performance-based pathway for major champions from 2022-2025, attracted only Brooks Koepka. Cam Smith, Jon Rahm, and DeChambeau all passed when the window closed in February. But the calculus changes materially when guaranteed money disappears and the league's operational continuity is uncertain.

The PGA Tour is under no pressure to accommodate. CEO Brian Rolapp told Pat McAfee in April that the Tour is "reading the same headlines" as everyone else and does not know what is happening inside LIV. The tone was deliberate. Any future pathways are expected to be more restrictive than the Returning Member Program, not less. For LIV's highest-value players, the ones who drive sponsorship, ticket sales, and whatever media value exists, every month of uncertainty erodes the asset base that a prospective buyer would be acquiring.

The Turnaround Playbook

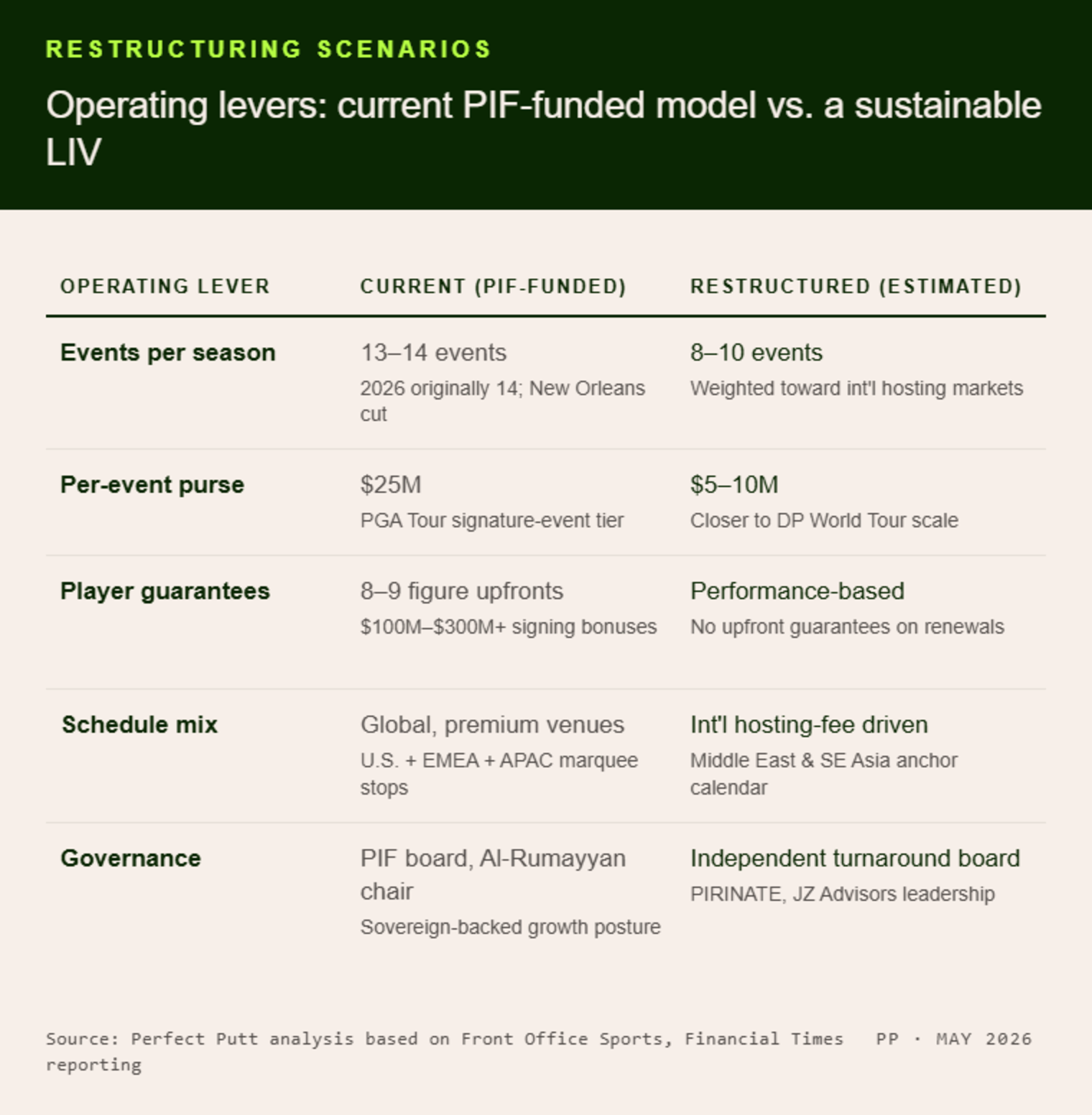

The composition of LIV's new independent board tells you what phase this business is entering. Gene Davis is the chairman and CEO of PIRINATE Consulting Group, a firm that specializes in turnaround management, merger and acquisition consulting, and restructuring advisory. Jon Zinman is the founder of JZ Advisors, a strategic advisory firm focused on financial and operational transformation for companies navigating complex reorganizations. Yasir Al-Rumayyan, PIF's governor, is stepping down from his role overseeing the league. These are not growth-stage appointments. This is the language of distressed-asset management.

A restructured LIV would need to look fundamentally different. The 2026 season was originally scheduled for 14 events; it is already down to 13 after the cancellation of New Orleans, where Louisiana is clawing back $1.2 million in state funding previously disbursed, per Front Office Sports. A sustainable LIV likely means 8-10 events, weighted toward international markets where hosting fees subsidize production costs. It means dramatically lower purses, closer to DP World Tour levels than the $25 million-per-event model that defined LIV's first four seasons. It means fewer players, leaner operations, and a product that is unrecognizable compared to what PIF funded.

There is also the DP World Tour question. Multiple reports have noted that a merger or partnership with the DP World Tour is among the options the new board is exploring. The strategic logic is straightforward: the DP World Tour has established media rights deals, a global tournament infrastructure, and relationships with golf federations that LIV lacks. But the DP World Tour also has a strategic alliance with the PGA Tour, and any integration with LIV would need to navigate that relationship. The path from here is narrow, and every viable option involves a materially smaller business than what PIF envisioned.

Who Acquires LIV?

The buyer universe for LIV Golf as a going concern is thin. Private equity requires a path to cash flow, and the gap between LIV's revenue and cost structure is too wide for any reasonable leverage profile. An alternative sovereign wealth fund faces the same strategic problem PIF identified: the investment required to sustain LIV dwarfs the realistic return on capital. A strategic acquirer like PGA Tour Enterprises could selectively absorb high-value components (certain player contracts, specific international event infrastructure, sponsorship relationships) but has no incentive to acquire the whole entity. The Tour's leverage increases with every month of LIV uncertainty, and Rolapp has demonstrated no urgency to accelerate that timeline.

The most probable outcome is not a single transaction. It is a managed disaggregation. The most competitive players return to the PGA Tour or DP World Tour on restrictive terms. The sponsorship portfolio, the one asset class with demonstrated value, is either retained by a slimmed-down entity or transferred to whatever successor structure emerges. The international event calendar, particularly in markets like the Middle East and Southeast Asia where hosting fees are substantial, may survive in some form under a different governance structure. The franchise equity (the $300 million team valuations, the $1 billion aspiration) is written down to whatever a small number of wealthy individuals are willing to pay for what amounts to a branding exercise attached to an exhibition tour.

The $6 billion experiment produced real competitive pressure on the PGA Tour, real fan engagement in new markets, and real growth in sponsorship and attendance. What it did not produce was an economic moat. And without one, the asset is worth what the next dollar of subsidy costs. As of April 29, that is a number PIF decided it was no longer willing to pay.

Capital Implication

LIV Golf's post-PIF future will be determined in the next six to nine months, and the outcome will reshape the competitive structure of professional golf for the next decade. If LIV winds down, the PGA Tour recaptures competitive exclusivity over the world's best players for the first time since 2022, strengthening its media rights negotiating position, reinforcing the SSG-backed $12 billion enterprise valuation, and removing the primary source of purse inflation that has compressed tour economics.

If LIV survives in diminished form, it becomes a niche international circuit operating at a fraction of its current scale, relevant to hosting-fee markets but no longer a competitive threat to the PGA Tour's talent pipeline. Either outcome is net positive for PGA Tour Enterprises.

The question for the rest of the golf ecosystem (sponsors, broadcasters, equipment OEMs, and the players caught in between) is how disorderly the transition becomes.

The best way to support Perfect Putt is to share it with a friend.