Going Back for Seconds: The $4.3 Billion Repricing of the Private Club

More than $4.3 billion in private club enterprise value has changed hands in the last six months. KSL Capital Partners is paying approximately $3 billion to re-acquire Invited Clubs, a company it previously built and exited. Bain Capital closed a $1.3 billion-plus deal for Concert Golf Partners. The question worth asking is not what happened. It is why institutional capital is paying up for golf and country clubs, and what these buyers see in the economics that the rest of the market does not.

Welcome to Perfect Putt, a twice-weekly newsletter covering the business and economics of the 140B+ golf industry. If this was forwarded to you, subscribe to join 11,000+ readers who follow how capital flows through golf.

Read Time: 7 minutes

Where the Arbitrage Sits

The United States has approximately 4,500 private clubs. Around 2,700 of them, roughly 60%, are member-owned equity clubs, typically structured as 501(c) nonprofits governed by volunteer boards. These clubs are not run as businesses. They are run as cooperatives. Boards rotate. Capital planning is reactive. Maintenance is deferred. And member equity, the initiation deposit members pay to join, is rarely liquid and often impossible to sell at cost.

Concert Golf Partners founder Peter Nanula has described this member equity as "somewhat of an illusion." He built a $1.3 billion platform on that insight.

The arbitrage is a governance arbitrage. An institutional acquirer buys a club from volunteer owners who have under-managed the asset for years. The purchase price reflects depressed economics: deferred maintenance, suboptimal pricing, assessment-funded capital plans. The acquirer professionalizes operations, deploys capital, raises pricing to market-clearing levels, and re-underwrites the revenue model. The resulting EBITDA bears little resemblance to what existed at acquisition.

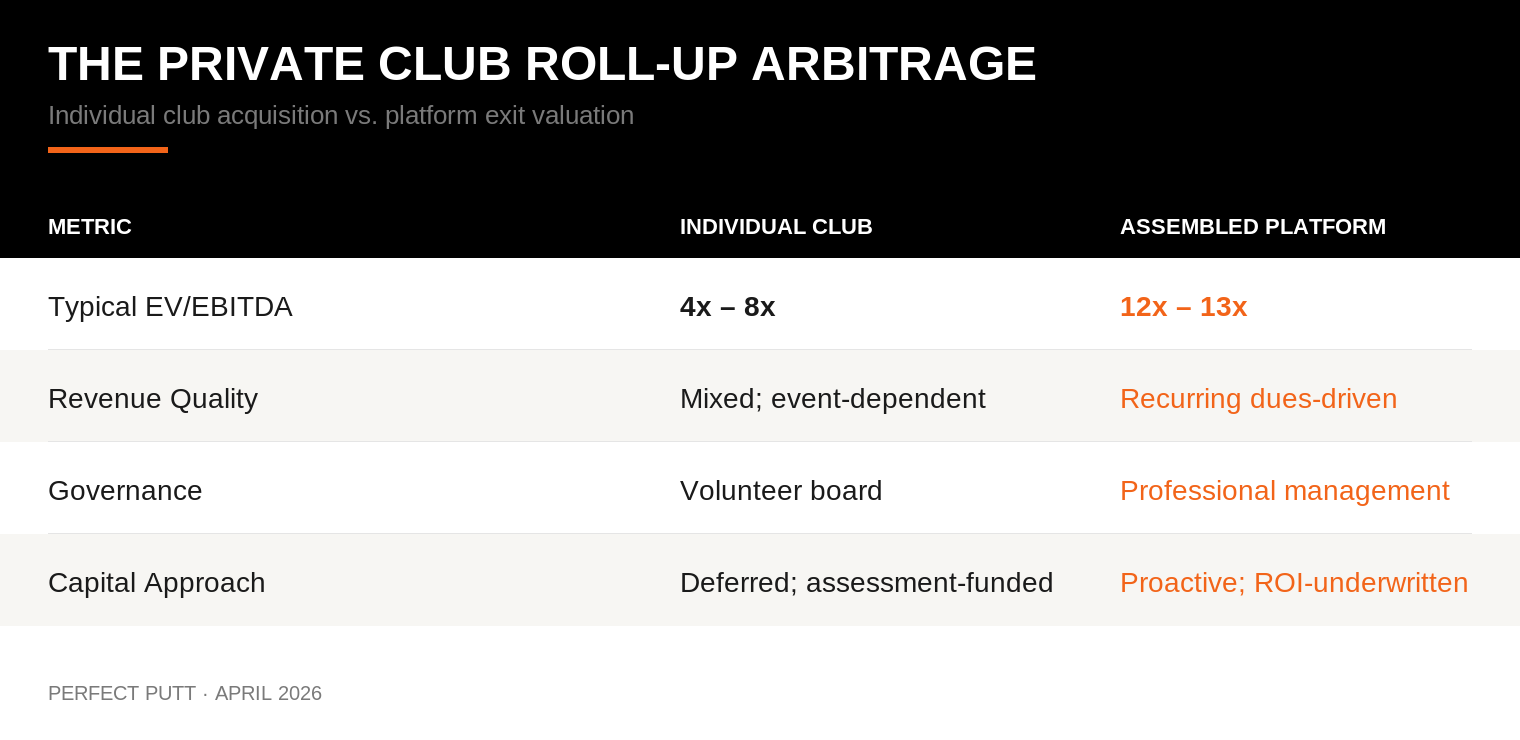

Clearlake invested in Concert in April 2022 when the platform had roughly 20 clubs. Over three and a half years, Concert completed 14 acquisitions, nearly doubled the portfolio to 39 clubs, and doubled both revenue and profitability. When Bain acquired Concert at $1.3 billion-plus, it was underwriting the transformed economics. The spread between what Concert paid for individual clubs and what Bain paid for the assembled platform is where the return was generated. Individual clubs typically trade at 4x to 8x EBITDA. Assembled platforms with professional management and recurring revenue trade at 12x to 13x. PE-led golf transactions averaged 12.8x in late 2025, compared to 9.9x for corporate buyers. That multiple gap is the core of the return.

The Capital Structure Underneath

Multiple arbitrage alone does not explain why PE is paying up for this category. What makes private clubs distinctive is the capital structure embedded in the membership model.

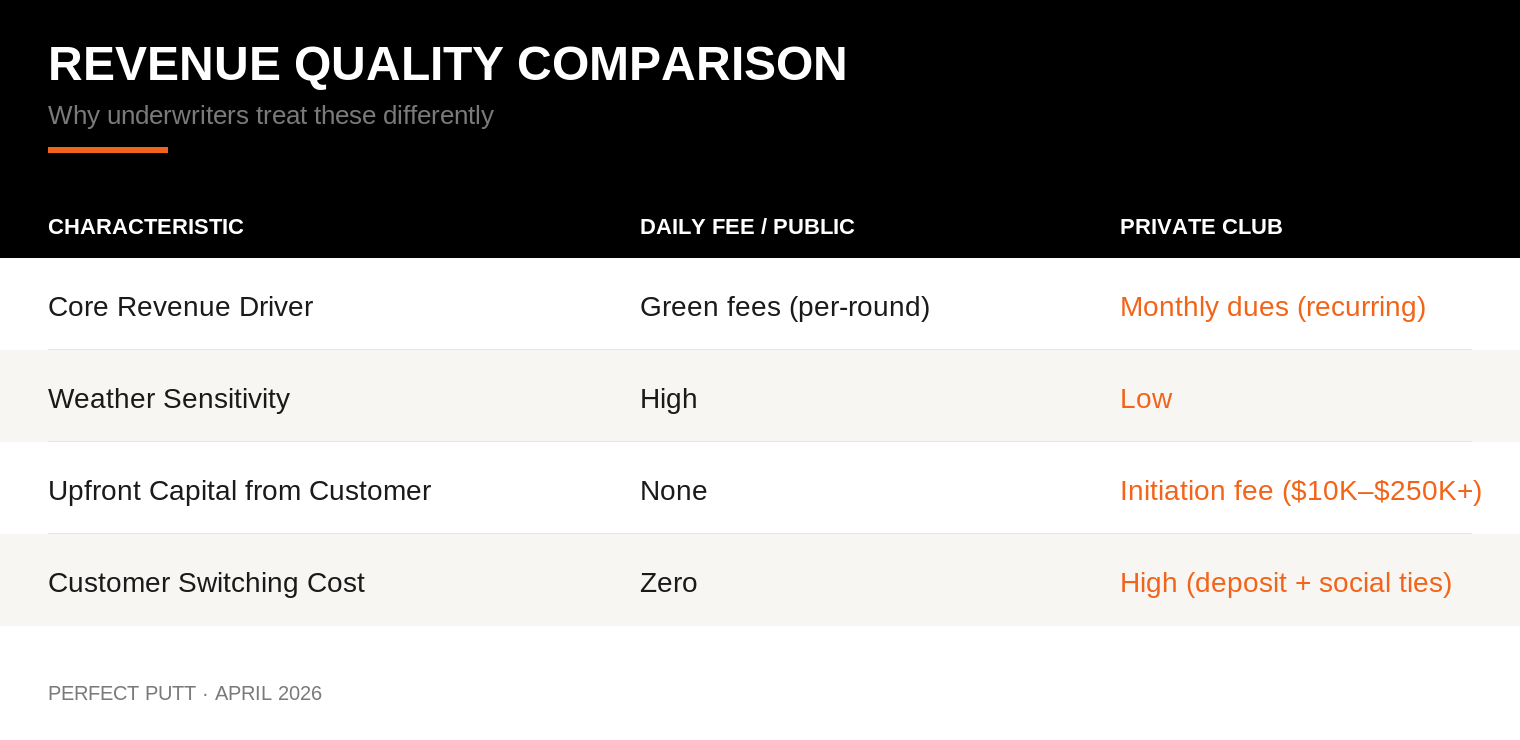

A private club member pays an initiation fee, anywhere from $10,000 to north of $250,000, and then pays monthly dues, typically several hundred to over a thousand dollars. The initiation fee provides upfront capital at zero cost. Refundable deposits are structured with 30-year horizons and subordinated to everything on the balance sheet. In practice, they function as quasi-permanent equity. Non-refundable fees are simply revenue. Monthly dues are recurring, contracted, and not weather-dependent. A private club collects dues in January the same way it does in July. The revenue profile looks less like hospitality and more like a subscription platform with a physical asset attached.

Because dues revenue is recurring and contractual, lenders underwrite it at higher advance rates than transactional hospitality revenue. Per Apollo's December 2025 sports-financing paper, average loan-to-value ratios across sports and club assets sit at roughly 10%, compared to 40% to 70% in traditional real estate or healthcare. Private clubs are structurally under-leveraged relative to the cash flow they produce. For a PE buyer, that gap is both safety margin and the capacity to optimize the capital stack. The customer finances the business at zero cost through initiation deposits and monthly dues. That is the capital structure KSL is paying $3 billion to re-acquire.

How the Return Gets Built

Acquiring a mispriced asset is step one. The return that clears a 20%-plus gross IRR over a four-to-six-year hold is built through four operational levers.

Conversion. Concert's playbook: buy a member-owned club all-cash, eliminate debt, fund capital improvements immediately, convert from nonprofit governance to professional for-profit operation. Concert's $60 million-plus acquisition of The Club at New Seabury on Cape Cod came with what SVP Jordan Peace described as "a large, multimillion-dollar capital plan" to invest further, even though the property was already "healthy and thriving." The conversion unlocks pricing power that volunteer boards could never exercise.

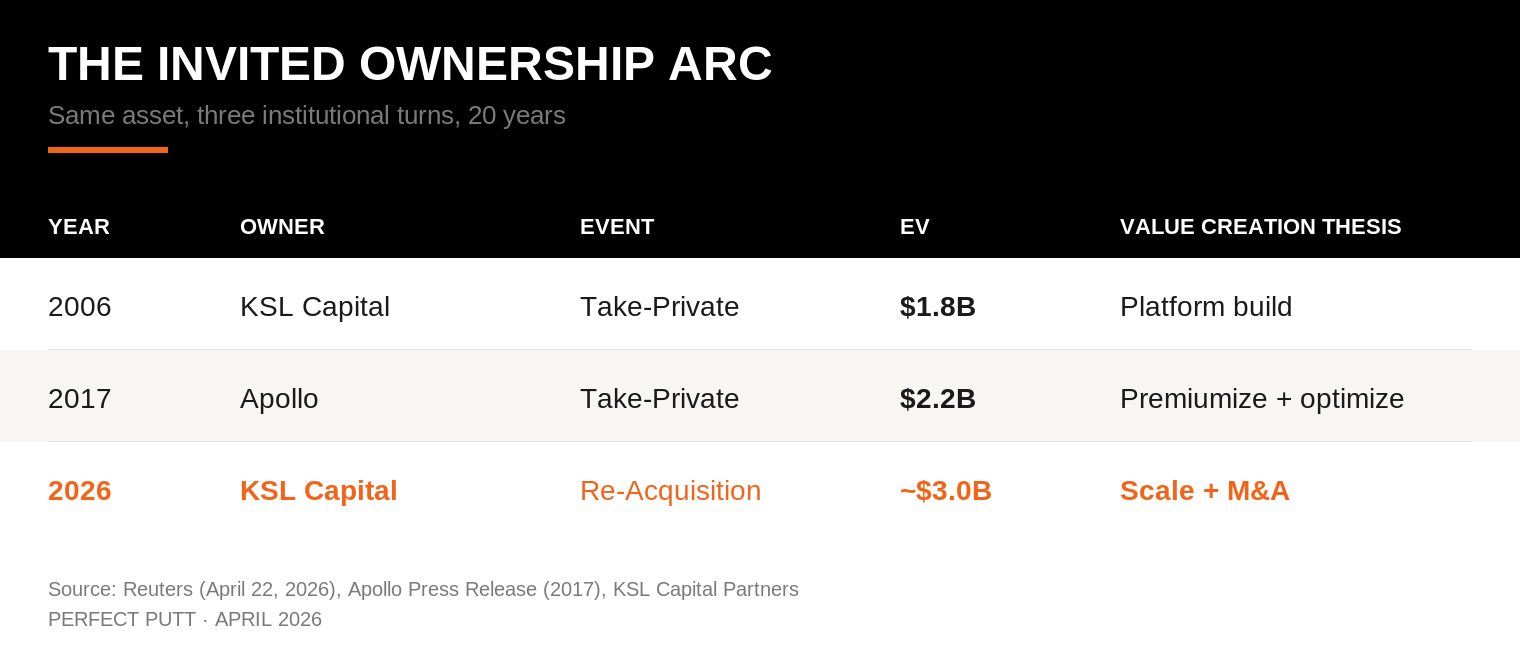

Premiumization. The lever Apollo executed at Invited. Segment the portfolio into tiers, from entry-level through ultra-premium, and use targeted capital investment to move clubs upward. Each tier step carries a 20%-plus increase in dues rates. Initiation fees can increase by multiples. Public benchmarking shows private clubs reported a 34% increase in total income per member between FY 2021 and FY 2023. Across a 150-plus club portfolio, the compounding effect is material. The Invited ownership arc illustrates how each successive sponsor has layered a different value creation thesis onto the same asset. KSL built the platform at $1.8 billion in 2006, Apollo premiumized it after taking it private at $2.2 billion in 2017, and KSL is now re-acquiring at approximately $3 billion to run the next turn of scale and M&A. A 67% increase from original entry, driven not by golf participation trends but by operational transformation.

Portfolio optimization. Sophisticated operators run the playbook in both directions. On the buy side, the platform maintains a pipeline of 15 to 20 targets drawn from roughly 1,500 clubs that fit acquisition criteria. On the sell side, underperforming clubs are divested, often at healthy multiples, to concentrate capital on higher-ROI properties. Invited today operates over 150 clubs, down from more than 200 at peak. That contraction was disciplined capital allocation, not weakness.

Ancillary revenue. Fitness, racquet sports, pools, premium F&B, and event programming all drive incremental per-member spend without adding rounds, which would degrade course quality. Private clubs reported a 34% increase in total income per member between FY 2021 and FY 2023 alone, per RSM's Financial Trends Report. That is not inflation. It is the result of deliberate amenity investment that widens the revenue base per member.

Why Supply Makes the Math Work

Every value creation playbook breaks if supply does not cooperate. In private clubs, it cooperates emphatically.

Private club membership grew roughly 55% from 2019 to 2025, from 1.4 million to 2.2 million members. Private course supply grew 0.1% over the same period. Per the National Golf Foundation, 77% of private facilities report being at or near capacity. New development averages roughly 13 courses per year nationally, takes five-plus years from entitlement to opening, and concentrates in ultra-premium segments. The supply response that would erode pricing power cannot arrive within a PE hold period.

The acquisition pipeline benefits from the same dynamic. There are roughly 2,700 member-owned equity clubs in the U.S., a figure that has declined 20% since 1990. Rising capital costs, aging governance structures, and the proven success of professional conversion models have created a steady stream of willing sellers. Total golf course transaction volume reached $632 million in 2024, up 115% from 2019. There are more sellers than professional buyers. That is a buyer's market for acquirers, even as prices rise.

What Breaks

The risk discipline matters precisely because the thesis is clean.

The most direct risk is cyclical. Private club membership correlates with affluent-household net worth. KSL's first ClubCorp acquisition at $1.8 billion in 2006 preceded a crisis that compressed club economics for a decade. Paying $3 billion in 2026, with household wealth at records, carries the same timing exposure. Dues are sticky and switching costs are real, but initiation pipelines slow in a downturn and the EBITDA trajectory that justified the entry multiple flattens.

The second risk is deposit liabilities. Membership deposits function as free capital in growth. In contraction, as 2008 demonstrated, they become redemption requests that can force refinancings. Professional operators with strong reserves manage this. Operators who have over-levered against deposit-inflated cash flows do not.

The third risk is buyer concentration. Every major U.S. private club platform is now PE-owned: KSL holds Invited and Heritage, Bain holds Concert, Atairos backs Arcis, TPG backs Troon. When the entire category is institutionally held, the marginal buyer at exit becomes harder to find. KSL buying back what it previously sold may reflect that constraint as much as conviction.

The Capital Implication

The question these transactions answer is specific: where does the return come from?

It comes from buying mispriced assets from amateur operators at fragmented-market multiples. From converting volunteer-governed nonprofits into professional platforms. From deploying capital where the return flows through as pricing power: higher dues, higher initiation fees, deeper per-member spend. From a capital structure where the customer finances the business at zero cost. And from a supply environment where demand has grown 55% while supply has not moved.

KSL looked at every opportunity in the market and chose the one it had already built and exited. Bain paid $1.3 billion for the only pure-play private club operator in the industry. These are not bets on golf. They are bets on a specific set of economic mechanics that, once professionalized, clear institutional hurdle rates with margin to spare.

The story is not the $4.3 billion headline, but the capital structure underneath.

The best way to support Perfect Putt is to share it with a friend.