Golf Simulators: A Hardware Business with a Software Future

Welcome back. We have an exciting edition this week — today's deep dive features a guest post from our friends at The Club by Old Tom Capital, a private, golf-focused investment community for accredited investors. If you haven't come across them yet, they're worth knowing.

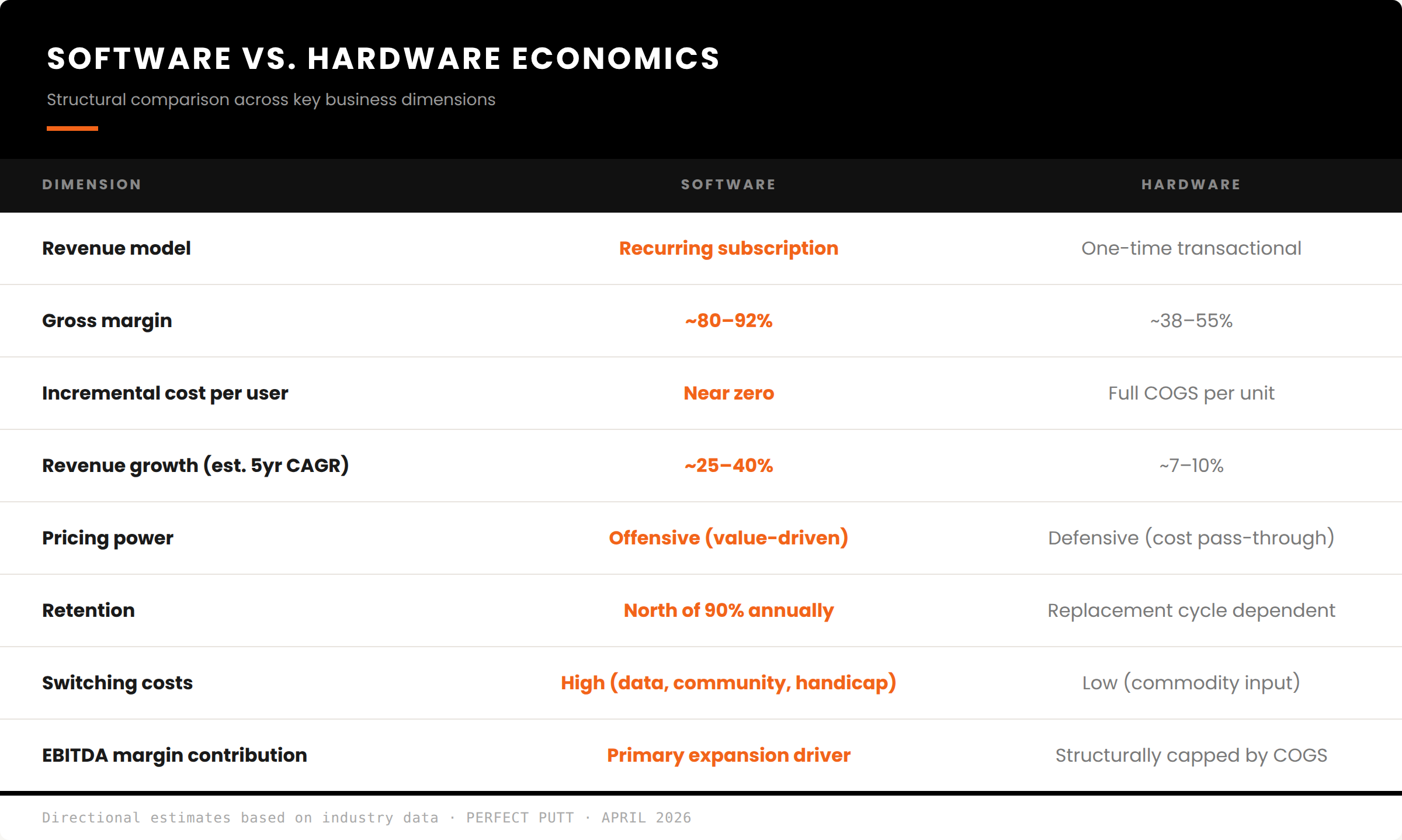

Recurring software is the only segment of the simulator economy driving margin expansion. Inside a typical vertically integrated simulator company, software generates roughly 5% of revenue today against 80% from hardware — but it carries gross margins nearly double the hardware line, grows three to five times faster, and retains subscribers above 90% annually. The mix is small. The trajectory is not.

The simulator category is one of the clearest examples of mispricing we see in golf today. The market continues to frame these businesses as hardware companies. The durable economics sit entirely in the software layer — and the gap between those two framings is where the opportunity lives.

Read Time: 9 minutes

The Software Thesis

Five years ago, building a home golf simulator required a $15,000 launch monitor, proprietary software locked to that device, and a room large enough to swing a driver. Today, a golfer can buy an entry-level launch monitor for under $700, pair it with third-party software for $250 a year, and play 2,000 courses from a garage bay. The hardware barrier has collapsed. The durable economic value accrues to software.

The $2 billion figure most commonly cited for this market represents the global simulator hardware industry — enclosures, tracking systems, launch monitors, screens. Topgolf alone generated $1.8 billion in segment revenue in 2024. Add launch monitors, entertainment venues, tech-enabled coaching, the residential installed base, and the emerging software layer, and the total off-course golf economy is conservatively $9 to $11 billion globally, growing north of 10% annually. The $2 billion figure is the hardware slice. It is not the market.

A record 48 million Americans played golf in some form in 2025. Nearly 38 million engage off-course. Approximately 19 million participate exclusively off-course and have never booked a tee time. The U.S. has lost over 2,000 courses since 2006 while commercial simulator businesses have nearly tripled since 2022. More golfers, fewer courses, and a generation that expects digital-first experiences. The simulator is the release valve. The split between hardware and software within it will define which companies compound and which compete on price.

The Hardware Race to the Bottom

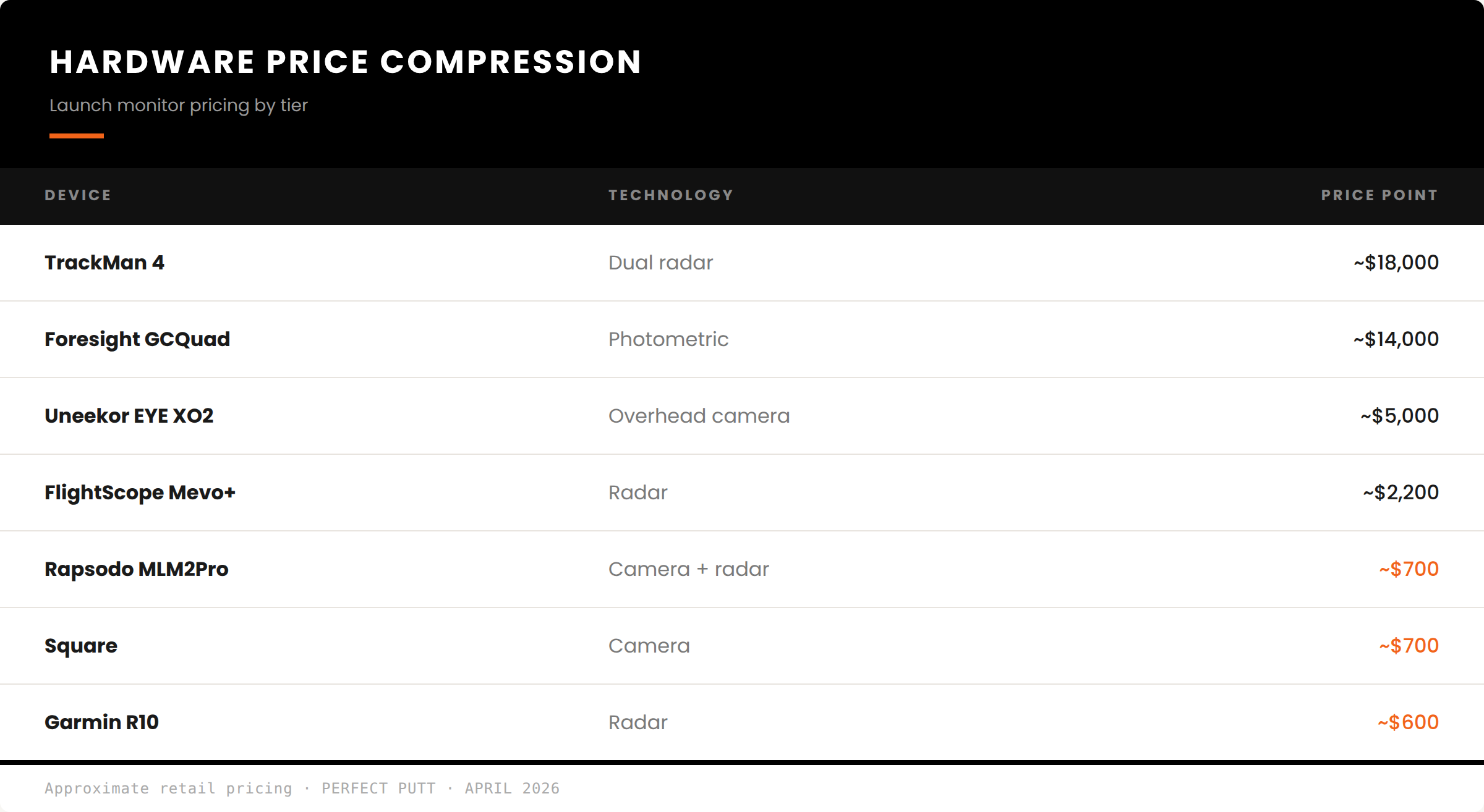

The launch monitor market has undergone a pricing compression that mirrors classic consumer electronics cycles. Premium devices anchored at $14,000 to $25,000 for a decade now have mid-market equivalents at $2,000 to $5,000 and entry-level competitors at a fraction of the legacy price point. Performance parity at the recreational level is effectively achieved — the accuracy gap that justified a $15,000 device has narrowed to a margin most golfers will never notice.

This is a textbook commoditization curve. Launch monitor hardware margins sit in the 38–50% range and are compressing as sub-$2,000 entrants drive the floor lower. Even vertically integrated companies with proprietary tracking systems are finding that margin expansion depends on software attach, not hardware pricing power.

The commercial simulator enclosure is more insulated — a $50,000-plus unit with proprietary tracking still commands a premium on latency and build quality. But this is a technology moat that erodes every sensor cycle. We do not underwrite it as durable.

Where the Margin Lives

Simulator software is economically superior to hardware on every dimension that matters for long-term value creation — margin, growth, retention, and reinvestment intensity.

Hardware gross margins range from roughly 38% to 55%, capped by the cost of goods. Software gross margins sit in the 80–92% range. Content is developed once and distributed to every user simultaneously, at near-zero incremental cost per subscriber.

The compounding mechanism is the installed base. Every new simulator unit sold at full hardware COGS adds a software subscriber at near-zero marginal cost. Retention on recurring simulator software runs north of 90% on open-architecture platforms — meaning customers choose to stay rather than being locked in. Commercial venues treat the subscription as operational infrastructure, not discretionary spend. Recurring, contracted, compounding on the installed base without proportional reinvestment — that is software revenue. Hardware revenue is none of those things.

Over a five-year horizon, recurring software grows at an estimated 25–40% annually while core hardware grows at 7–10%. EBITDA margin expansion is sourced almost entirely from software mix shift, not from operational improvement on the hardware side. If software growth stalls, margin expansion disappears. If hardware stalls but software keeps compounding, margins expand faster. That asymmetry is the thesis.

Hardware is not the business. Hardware is the distribution infrastructure for a software annuity. The hardware sale is the acquisition event. The software subscription is where the lifetime value compounds.

The Strategic Moat: Interoperability

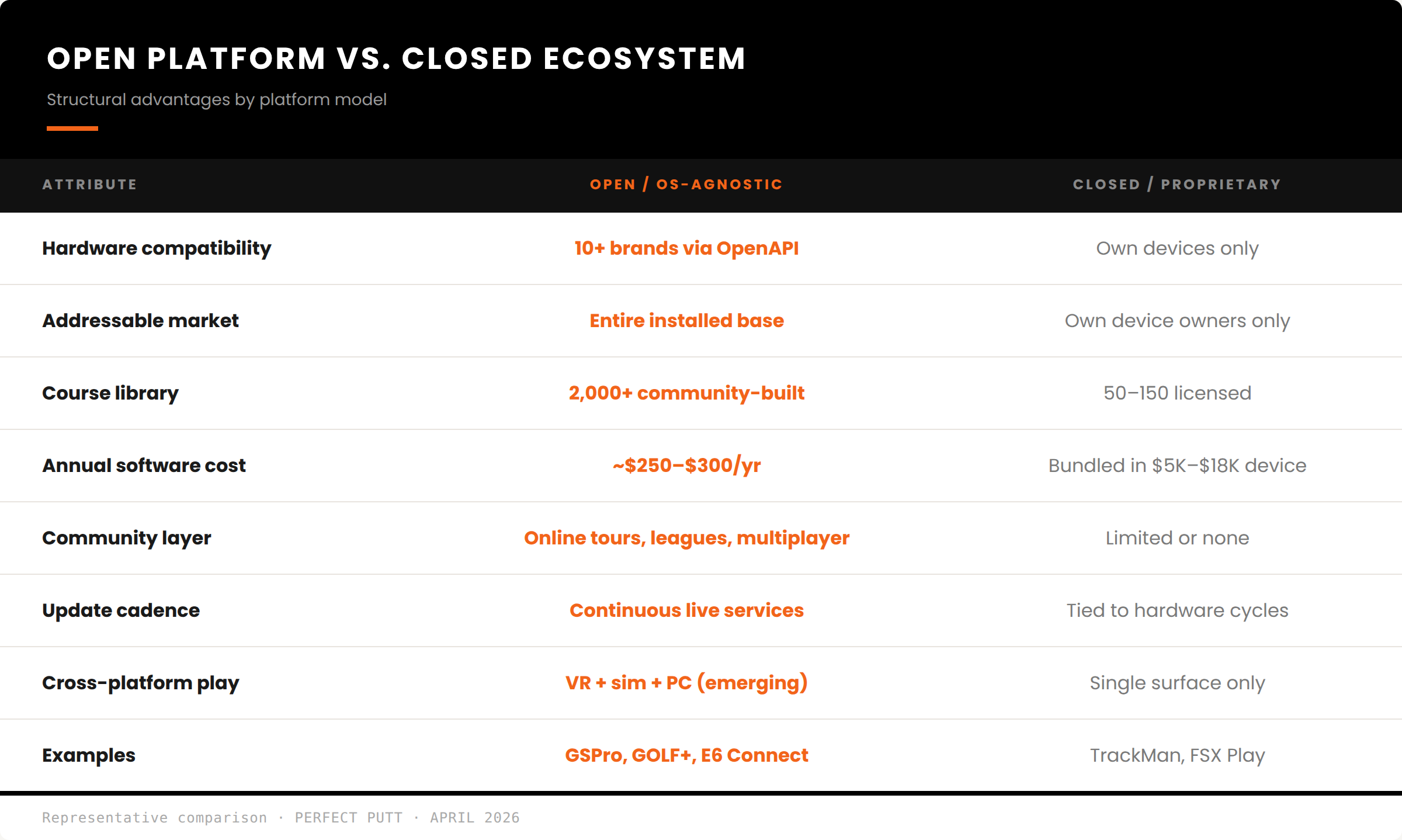

The most important variable an investor can underwrite in this category is whether the software is open or closed.

Closed ecosystems — software locked to proprietary hardware — capture margin on both sides but cap the addressable market at their own device sales. They work at the premium tier and nowhere else.

Open platforms take the opposite approach. GSPro integrates with every major launch monitor on the market — Uneekor, Foresight, FlightScope, Garmin, Rapsodo, Full Swing — and its user community has built more than 2,000 courses using proprietary design tools, a content library that grows without the company spending a dollar on licensing. GOLF+, which pioneered VR golf on Meta Quest with over two million players, is now porting its physics engine to traditional simulator hardware. E6 Connect runs across iPad and Windows with a commercial operator focus.

The structural consequence is what matters. Open platforms grow with the hardware market regardless of who wins the hardware race. Every new launch monitor sold — by any manufacturer, at any price point — is a potential subscriber. Closed ecosystems grow only with their own device sales. In a market where launch monitor volume is accelerating while average selling price is declining, the platform that works with everything owns the expanding installed base. That is a structural asymmetry worth owning.

The Hardware Pivot

Hardware companies see the shift. Launch monitor and simulator OEMs are retrofitting subscription layers onto their businesses: gating features behind paid tiers, building proprietary content libraries, requiring subscriptions for third-party platform access.

The instinct is correct. The execution is structurally constrained. A hardware company adding software is bolting a subscription onto a transactional business. The org chart, the P&L, and the capital allocation still orient around the next hardware cycle. Software is the supplement, not the core.

Software-native platforms were built the other way around. Platform first, hardware-agnostic by design, community as the retention engine from day one. They are the subscription model. Building from the platform out versus building from the box out is the structural gap that determines which companies compound and which compete on price.

The most telling signal comes from the OEM side. At least one major launch monitor manufacturer now sells a third-party software subscription through its own storefront. When hardware companies start distributing someone else's software, the value migration is no longer theoretical. It is already priced into customer behavior. The public markets will follow.

Community Is the Retention Engine

The software companies that will compound are not the ones with the best graphics. They are the ones that build the deepest community infrastructure: competitive layers, social features, and retention mechanics that make the platform more valuable as the user base grows.

GSPro's Simulator Golf Tour runs ongoing online competitions across its subscriber base. GOLF+ operates a competitive tour with regular events and seasonal championships. A golfer with an established handicap, a tournament history, a regular playing group, and a competitive ranking on a platform does not switch because a competitor has marginally better course rendering. The social graph holds.

This is the dynamic that drives retention across every successful platform business. Strava in running, Peloton in fitness, Duolingo in education. The product is the entry point. The community is the moat. We underwrite community depth as rigorously as we underwrite unit economics.

The Missing Infrastructure Layer

The simulator ecosystem has scaled rapidly without the institutional infrastructure that underpins every other organized form of golf. That absence is the largest unclaimed pool of economic value in the category.

There is no unified handicapping system for simulator play. No GHIN equivalent. A golfer can post a score on GSPro, play a round on GOLF+, and complete a session on E6 Connect, and none of those results connect to each other or to the on-course handicap system. No certification standard for shot realism. No sanctioning body for competition. No federated data infrastructure that allows performance to inform coaching, fitting, or player development. Over 9 million Americans used a simulator or screen golf setup in 2025, roughly half with no on-course handicap to begin with.

As simulator golf migrates toward structured competition, including leagues, tournaments, wagering, and real stakes, the absence of a governance layer becomes a constraint on the market's maturity. Whoever builds the standards, certification, and data infrastructure captures a category of value that sits above any individual software or hardware company. That layer does not exist today. It will. The firm that builds it owns the protocol for how simulator golf connects to the rest of the game.

The Next Convergence

The most interesting development we are tracking is the convergence of form factors. GOLF+ built its engine in VR and is bringing it to traditional simulators, running the same physics, courses, and competitive infrastructure whether a golfer wears a headset or hits into a screen. Mixed reality, in which a headset is worn while hitting real balls with a real club, may be the only current technology that credibly solves the putting and short game problem that has limited simulator realism since the format was invented.

The companies that can serve golfers across VR, simulator, and eventually PC and mobile from a single unified engine capture the largest addressable market without rebuilding the core product for each surface. That is a software architecture advantage no hardware company can replicate, and a mispricing the public markets have not yet caught.

Where Value Accrues

The market is still pricing simulator businesses as hardware companies with software supplements. The inverse is true. The error is structural. Public markets price what they can count, and what they can count in this category is units shipped. The recurring software line is too small, too new, and too unevenly disclosed to move a multiple. That is where the mispricing begins, and it is where it will persist longest.

Compounding value in this category is created by businesses building against three criteria simultaneously: a software mix that is small today but accelerating, an architecture open by design rather than by retrofit, and a community layer deep enough that users treat the platform as infrastructure. Most companies in the market are building for one. A few are building for two. The businesses building against all three are rare. Those are the ones we underwrite.

The simulator category reveals a pattern we see across golf. The industry has long been priced as a physical business: real estate, equipment, rounds played. The economic center of gravity is migrating to the digital infrastructure, recurring revenue, and data layers sitting above those traditional assets. Whoever owns the software, the community, and eventually the governance of a vertical within golf owns the durable margin of that vertical. Everything else is cost of goods sold.

The box gets you in the door. The platform keeps you there.

Thanks to Perfect Putt for the floor. If you want to invest in the future of golf, be sure to check out The Club and see if it's a fit for you.