The Modern Architecture of Golf Capital

The most important change in golf is not happening on a golf course. It is happening in the capital markets. As industries mature and become more financeable, they become more scalable and attractive to institutional capital. Capital stops supporting the industry and starts shaping it. Golf now appears to be entering that phase of its evolution.

Welcome to Perfect Putt, a twice-weekly newsletter covering the business and economics of the golf industry. If this was forwarded to you, subscribe below to join 12,000+ readers who follow how capital flows through golf.

Read time: 8 minutes

From Operating Business to Asset Class

Most golf commentary stays at the operator level. Who acquired whom, where membership is growing, whether tee time demand holds. The more durable lens is the capital markets, because the way an industry is financed eventually determines how it is structured.

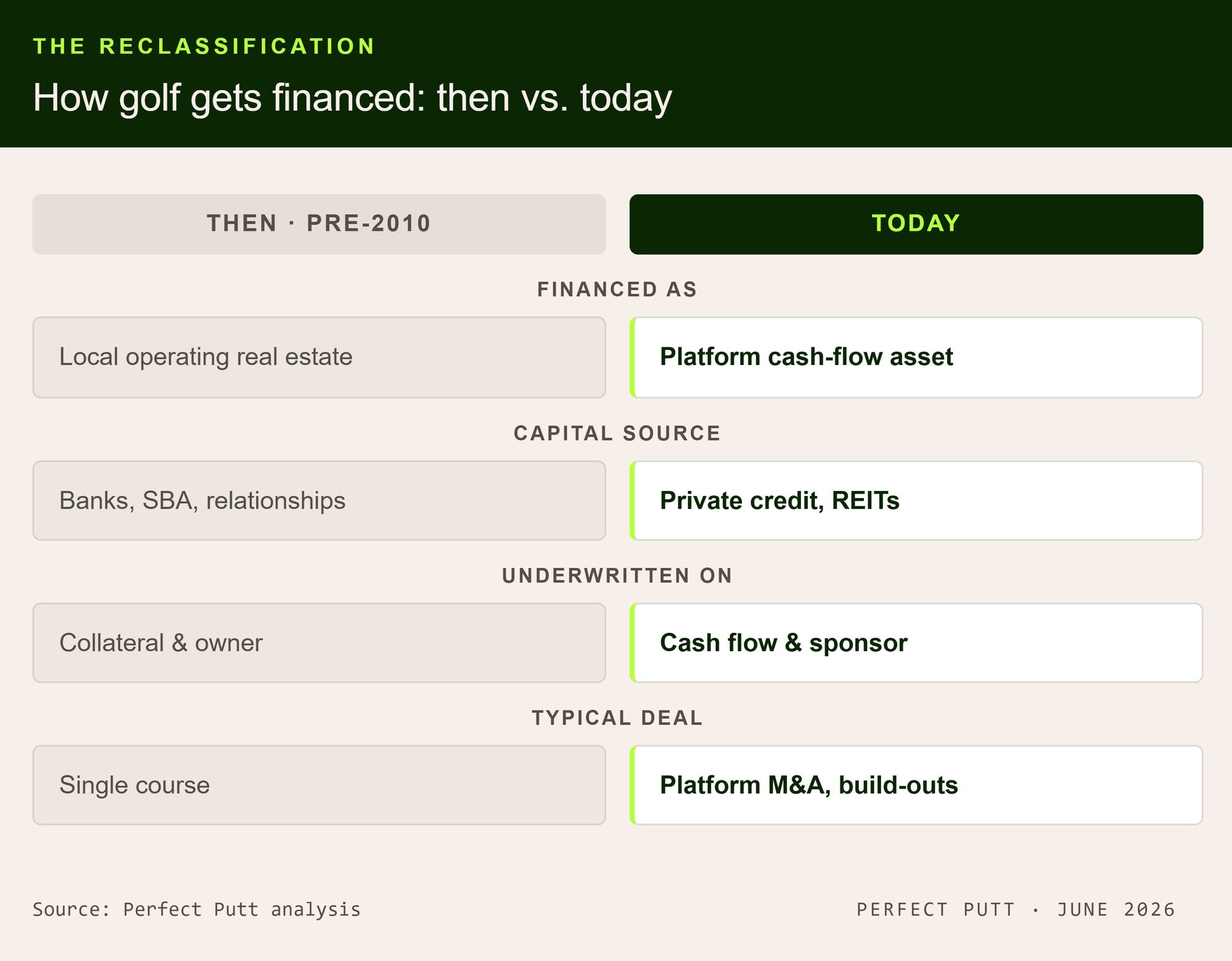

Historically, golf was financed the way a hardware store or a marina was financed: as local real estate, small business lending, and relationship banking. A course was a single asset, owned by an operator, financed by a regional bank that knew the family. Today the largest golf transactions are financed as platform M&A, institutional real estate, recurring-revenue infrastructure, and alternative asset-backed credit. The capital is bigger, more patient, and structurally different.

That transition matters because of what follows it. Once an industry becomes financeable at scale, capital availability begins shaping its structure as much as operational excellence does. The operators will get the headlines. The capital will set the terms. Golf is not the first industry to make this passage, and the path it is walking is well worn.

Asset Classes Follow Similar Paths

Industries rarely begin as institutional asset classes. They become one only after investors learn to standardize underwriting, benchmark performance, and finance acquisitions at scale. The sequence has repeated across dozens of sectors, and it rhymes every time.

Apartment buildings became an asset class once lenders learned to underwrite occupancy and rent growth. Self-storage became one after operators demonstrated durable cash flow through a full cycle. Healthcare practices, veterinary clinics, HVAC, and dental groups became institutional categories once private equity proved that consolidation produced predictable returns. In each case the business did not change first. The financing did.

The early stage of any asset class looks the same. Ownership is fragmented. Every asset is treated as unique. Underwriting is bespoke, and capital is expensive because lenders cannot compare one asset to another with confidence. The mature stage looks different. Operators become platforms. Lenders build pattern recognition. Transactions throw off comparable data. Financing becomes repeatable, and once it does, capital scales into the sector and begins reshaping ownership itself.

Golf sits between those two stages today. It is no longer financed like a scatter of local businesses, and it is not yet financed with the efficiency of multifamily housing or industrial real estate. It is mid-passage: institutional enough to attract serious capital, not yet institutional enough to be priced efficiently. That in-between position is not a footnote. It is the entire opportunity.

Golf Can Carry Leverage

The question banks answered with a no fifteen years ago, and that credit answers with a yes today, is not whether golf demand improved. It is whether the revenue model can support institutional debt. It now can, and that is the real reason the asset class exists.

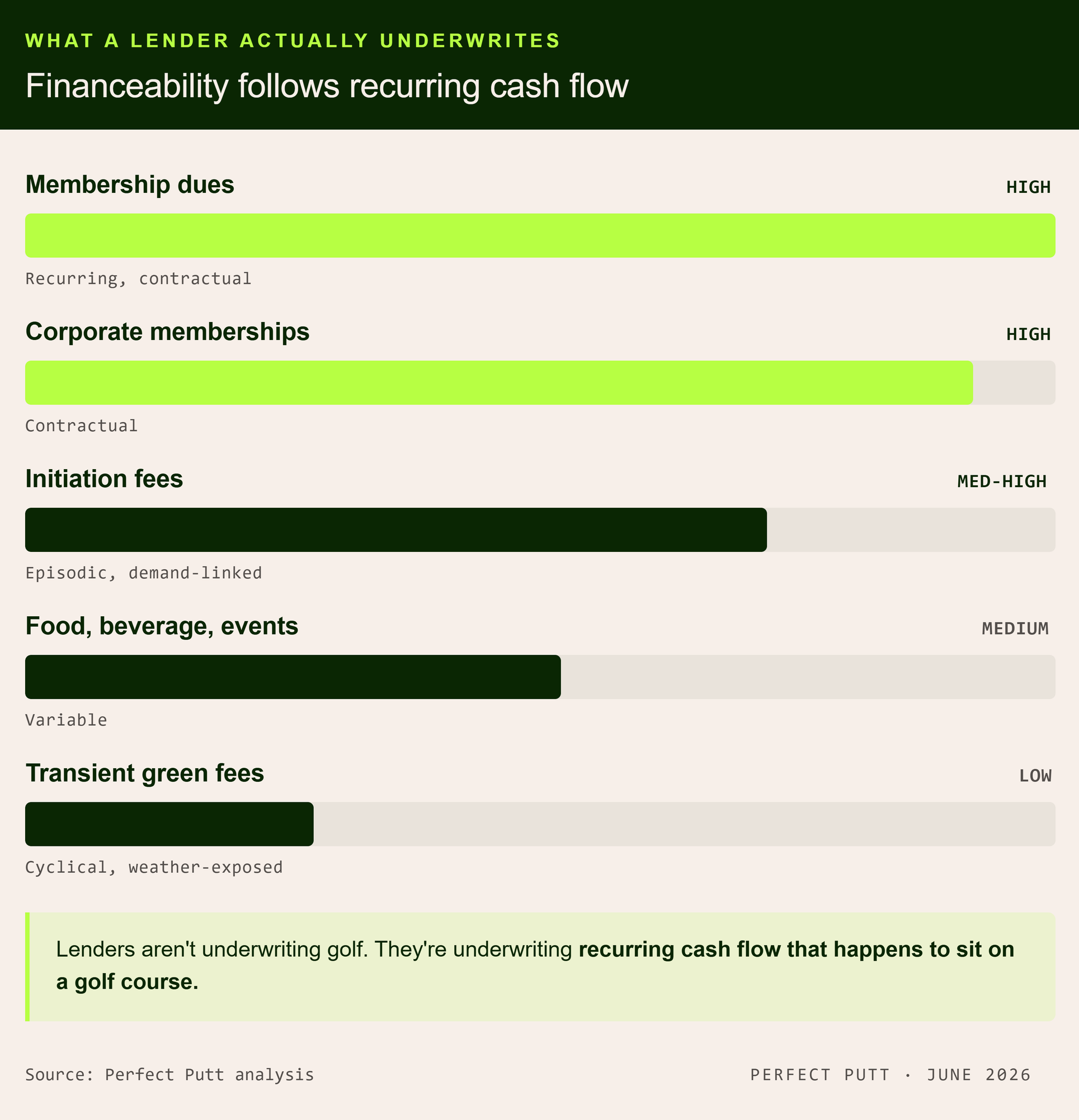

A lender cares less about rounds played than about the visibility of cash flow: contractual revenue, renewal behavior, customer concentration, and margin durability. A modern private club generates dues, initiation fees, food and beverage, events, lodging, corporate memberships, and ancillary recreation. The dues and corporate lines are contractual and recurring. They renew. They look far closer to subscription infrastructure than to a seasonal recreation business. A club with roughly 70% of revenue from dues can support materially more leverage than a daily-fee course dependent on transient play, because the lender can see the cash before it arrives. This is the distinction the market missed for years.

The repricing followed the realization. Average course sale prices rose 38% in 2024 to $6,870,417, the highest since 2007, with the median up 22.8% to $3,025,000, per Leisure Investment Properties Group. Golf assets traded near an 11.5% median cap rate, roughly 700 basis points above core commercial real estate. That spread is the market paying up for cash flow it now trusts.

The Credit Behind the Headlines

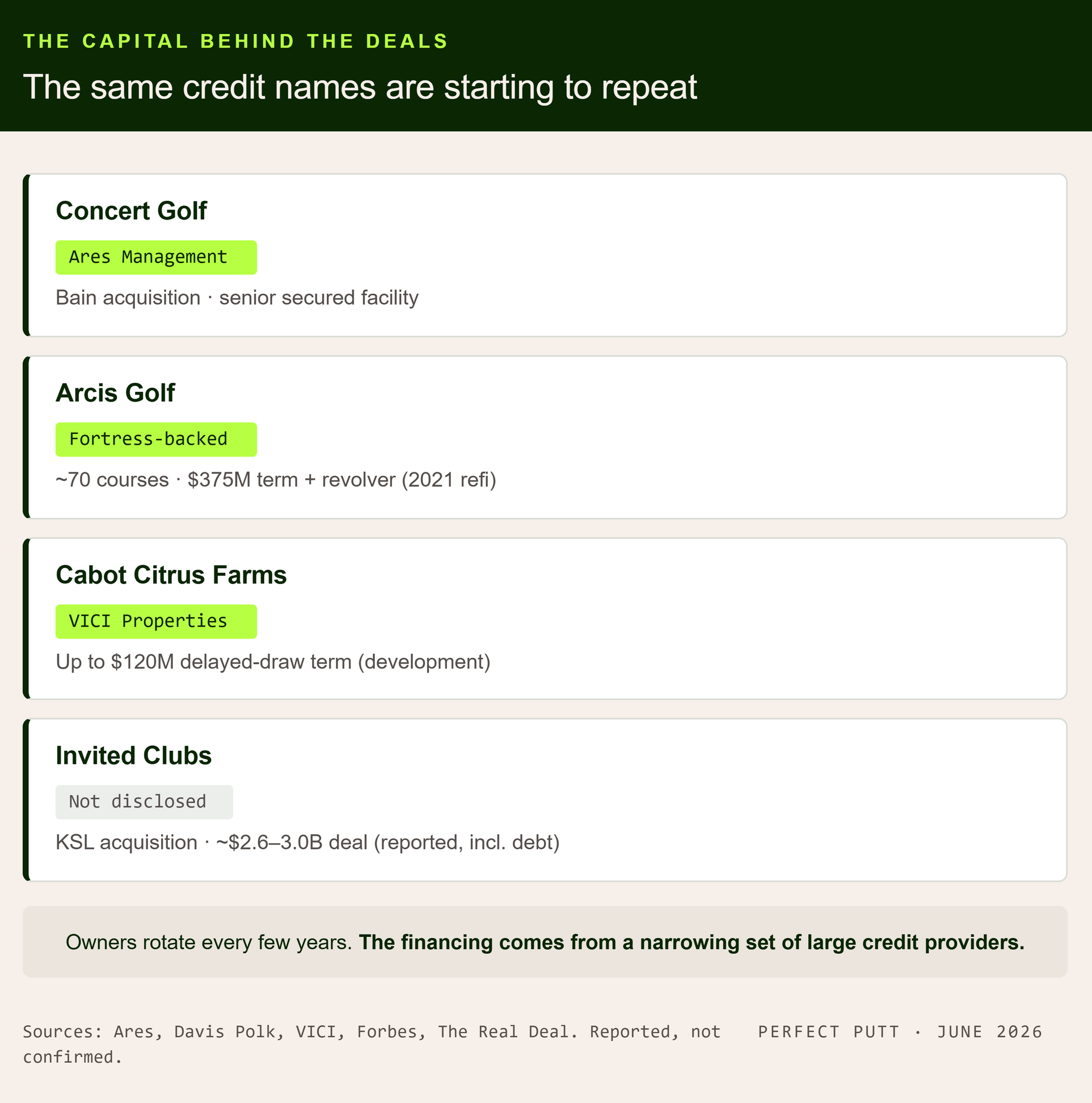

Golf's consolidation has been told as an equity story. Who bought which platform, at what valuation. The debt underneath is where the asset-class shift becomes concrete, and the names are starting to repeat, which is often the first sign that a sector has become institutionally financeable.

Ares Management served as administrative agent, lead arranger, and bookrunner on the senior secured facility behind Bain Capital's acquisition of Concert Golf Partners, per Ares, one line inside roughly $55.0 billion of U.S. direct lending the firm originated in 2025. Arcis Golf, backed by Fortress Investment Group since 2013 and Atairos since 2020, arranged a $375 million senior secured package in 2021, a $300 million term loan plus a $75 million revolver. That facility predates the current wave but set the template, funding a roll-up to roughly 70 courses through institutional credit rather than a bank. VICI Properties partnered with Cabot in 2022 with a delayed-draw term loan of up to $120 million to build-out of Cabot Citrus Farms.

Three deals, three forms of non-bank capital: direct lending, a syndicated leveraged facility, and a structured real estate loan. The pattern extends into the largest transactions even where the debt is invisible. When KSL Capital Partners reacquired Invited Clubs from Apollo Global Management in June 2026, reporting put the deal between $2.6 billion and roughly $3 billion including debt. What is visible is the consistency: who owns the clubs rotates every few years, while the financing is sourced from a narrowing set of large credit providers whose relationships outlast any single owner.

How a Golf Loan Gets Underwritten

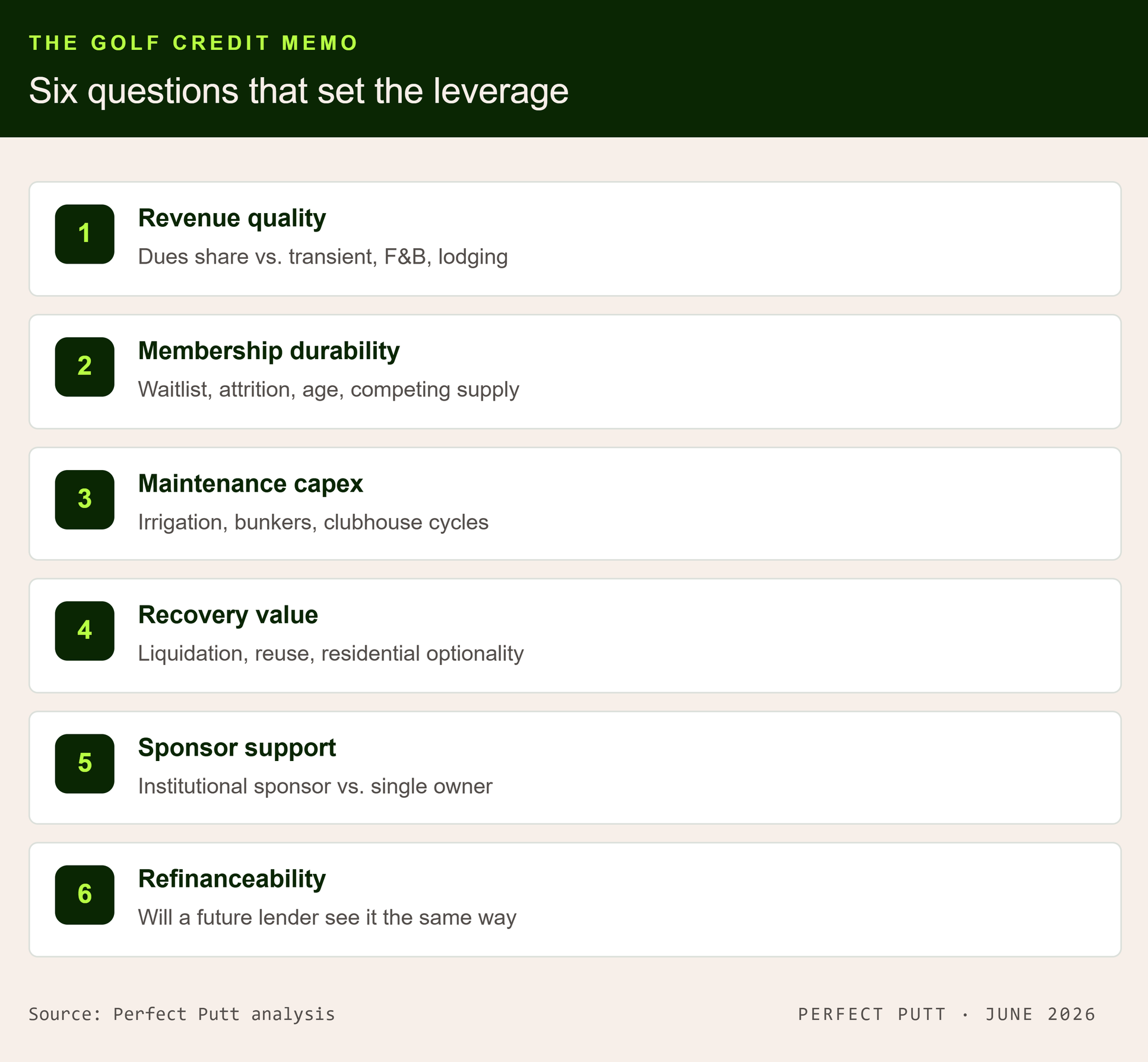

An asset class is only as real as the underwriting behind it, and golf credit is now underwritten with the specificity of any other institutional sector. A golf credit memo turns on five questions, and the answers determine how much leverage an asset can carry.

Revenue quality. The lender decomposes the top line into dues, initiation fees, transient rounds, food and beverage, and lodging. A club with roughly 70% of revenue from dues can support materially more leverage than one leaning on public play, because contractual revenue services debt and weather-dependent revenue does not.

Membership durability. Waitlist depth, historical attrition, the age distribution of the roster, local demographic trends, and competing supply tell the lender whether the dues base is stable or quietly aging out.

Maintenance capex is the line most often missed. A course can defer maintenance for a season but not forever, and irrigation replacement, bunker renovation cycles, and clubhouse needs are real claims on cash a careful lender sizes before sizing debt.

Real estate recovery value governs the downside: in distress, what is the collateral worth, can it keep operating, can it be repurposed, is there residential optionality, or is it conservation-restricted.

Sponsor support matters because Bain behind Concert and Fortress behind Arcis are not the same credit as a single-course owner-operator. The lender underwrites the asset and the sponsor together. The final test is the ability to refinance. The lender has to believe a future lender will view the asset the same way at maturity. This is what makes an institutional asset class self-reinforcing. Each financing sets a precedent for the next, and the precedent is what eventually lets underwriting standardize.

What Breaks First

While the asset class is real, it is continuously evolving, and the risks are specific. Golf is discretionary, and the demand level set in a strong economy is not a floor. The down cycle that ran from 2007 to 2020 is recent enough that anyone underwriting at peak demand is underwriting the good half of a long wave. Cap rates near 11.5%, with several recent course sales above 15%, are not a sign of safety. They are the market pricing real operating risk into golf collateral.

Refinancing is the sharper near-term risk. Much of the debt written into golf over the past few years assumed rates would ease and values would keep rising. If financing costs stay elevated and a course's cost of capital exceeds its cap rate, the math that justified the original loan inverts at maturity. The diversified platform with a relationship lender has options. The single transitional course that took mezzanine or preferred capital at a peak basis, refinancing into a tighter market, may not.

Golf Is Not Fully Institutional, Yet

For all the progress, golf remains an imperfect asset class, and the imperfection is the point. Unlike an apartment block or a self-storage facility, every golf asset is genuinely different. Geography matters. Weather matters. Membership culture matters. Two clubs with identical revenue can produce very different outcomes depending on the age of the roster, the condition of the irrigation, and the depth of the waitlist. The asset resists the standardization that makes pricing efficient.

That complexity is why underwriting stays specialized, and why spreads stay attractive. A lender who can read those differences earns a premium for the skill. A lender who cannot should not be in the asset at all. The opportunity exists precisely because golf has become institutional enough to draw capital but not yet institutional enough to be priced like a commodity.

This is the hinge of the thesis. The day every lender can underwrite golf with confidence is the day the excess return disappears. Standardization is the destination of every asset class, and it is also the end of the window in which early, specialized capital is paid for being early. Golf has not reached that day. It is moving toward it.

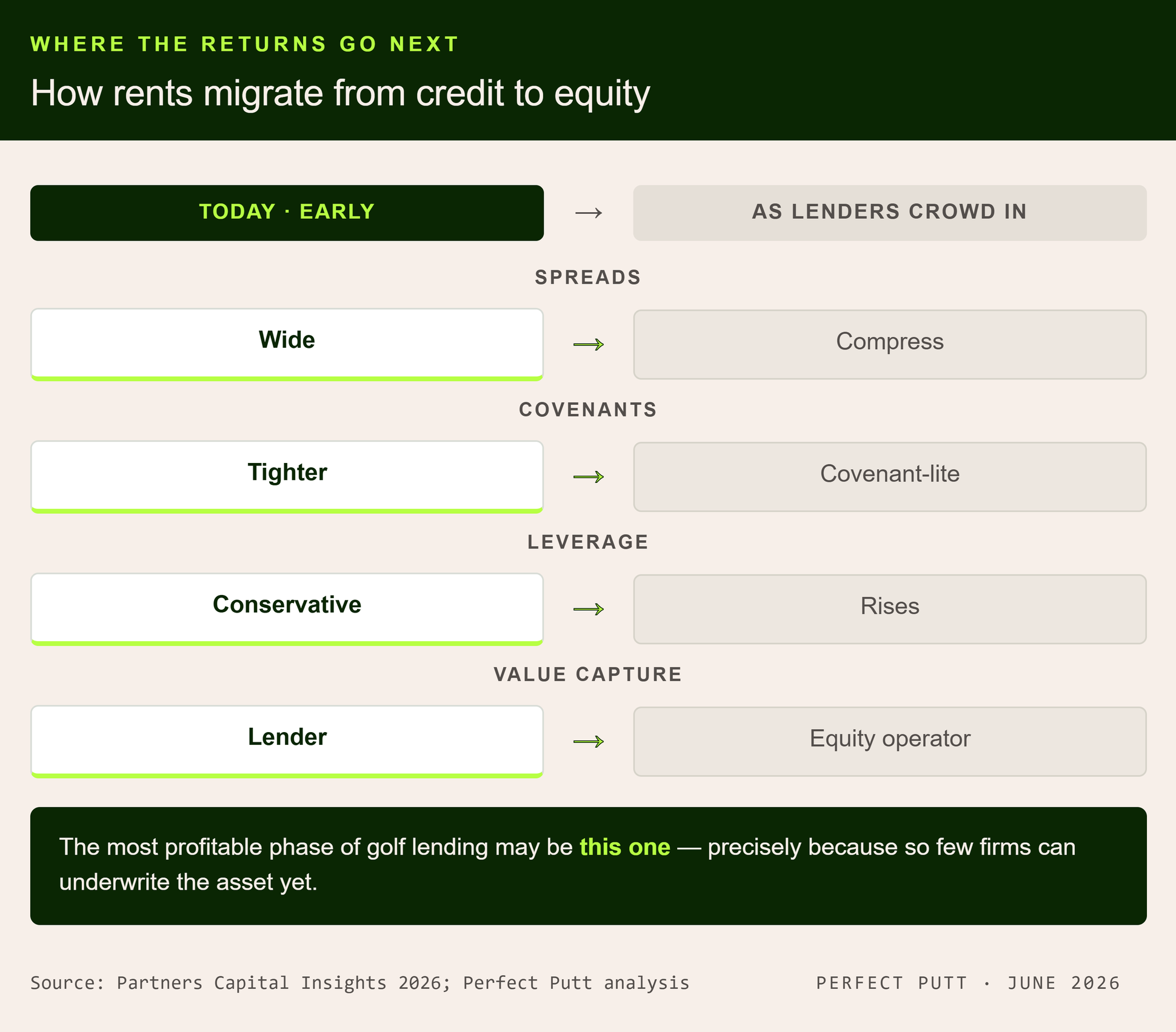

The Lenders May Not Stay the Winners

The temptation is to conclude that the lender now wins. That is true today, and it has a shelf life. Private credit is increasingly competitive, and competition is corrosive to lender economics. As more capital chases golf, spreads compress, covenants weaken, and leverage creeps higher. Each of those moves transfers value from the lender to the borrower. The covenant-lite drift already visible across private credit, with first-lien recovery rates near 38% against a long-term average closer to 62% per Partners Capital, is the early evidence.

The likely path is the one many middle-market sectors have already walked. Today, while golf underwriting is still scarce and bespoke, the credit earns the premium. Five years out, as more lenders enter, underwriting standardizes, and spreads tighten, golf credit commoditizes, and the economic rents migrate back to the equity owners who consolidated early and operate well. The most profitable phase of golf lending may be this one, precisely because so few firms can underwrite the asset yet. That window closes as the asset class matures.

Capital Implication

Golf is becoming an institutional asset class. That is the event underway, and private credit is the instrument carrying it. The near-term trade is clear enough: senior secured exposure to diversified, dues-driven club platforms with experienced sponsors and conservative leverage is attractive. The back of the stack on a single transitional course, destination-resort development, mezzanine, or preferred equity behind aggressive transient-round assumptions is where the risk concentrates and the margin thins.

The more durable conclusion sits underneath the deal flow. The scarce asset is not capital. Ares, Apollo, and Blackstone all have capital. The scarce asset is the ability to determine, consistently and through a full cycle, which golf assets deserve leverage, how much they deserve, and what they are worth when demand softens. That capability does not commoditize when spreads do.

The most defensible long-term position in golf may not be lending money or operating clubs. It may be owning the underwriting platform that determines which assets receive capital in the first place. As golf completes its move from a niche recreational business into a recognized institutional asset class, the allocators that can price the asset better than anyone else captures the value that competition strips from everyone who only supplies the capital.

The best way to support Perfect Putt is to share it with a friend.