The Business of the Upgrade

Golf has quietly built one of consumer sport’s most sophisticated secondary markets. What began as a way to resell last year’s clubs has become an infrastructure layer that shapes upgrade frequency, value capture, and control of the equipment economy.

Welcome to Perfect Putt, a newsletter covering the business and economics of the golf industry. If this was forwarded to you, subscribe to join 12,000+ readers who follow how capital flows through golf.

Read time: 7 minutes

Every weekend, golfers trade last year's clubs for credit toward something newer. It feels like a simple resale transaction. It isn't. Each trade-in recycles capital back into the equipment ecosystem, lowering the cost of upgrading and increasing the likelihood of the next purchase. The golfer saves money. The retailer acquires inventory and customer attention. The manufacturer benefits from a faster replacement cycle.

Taken together, millions of these transactions form one of the most important and least-examined markets in golf. The question is not why golfers trade clubs. It is who profits every time they do.

A $1Bn+ Market Hiding in the Garage

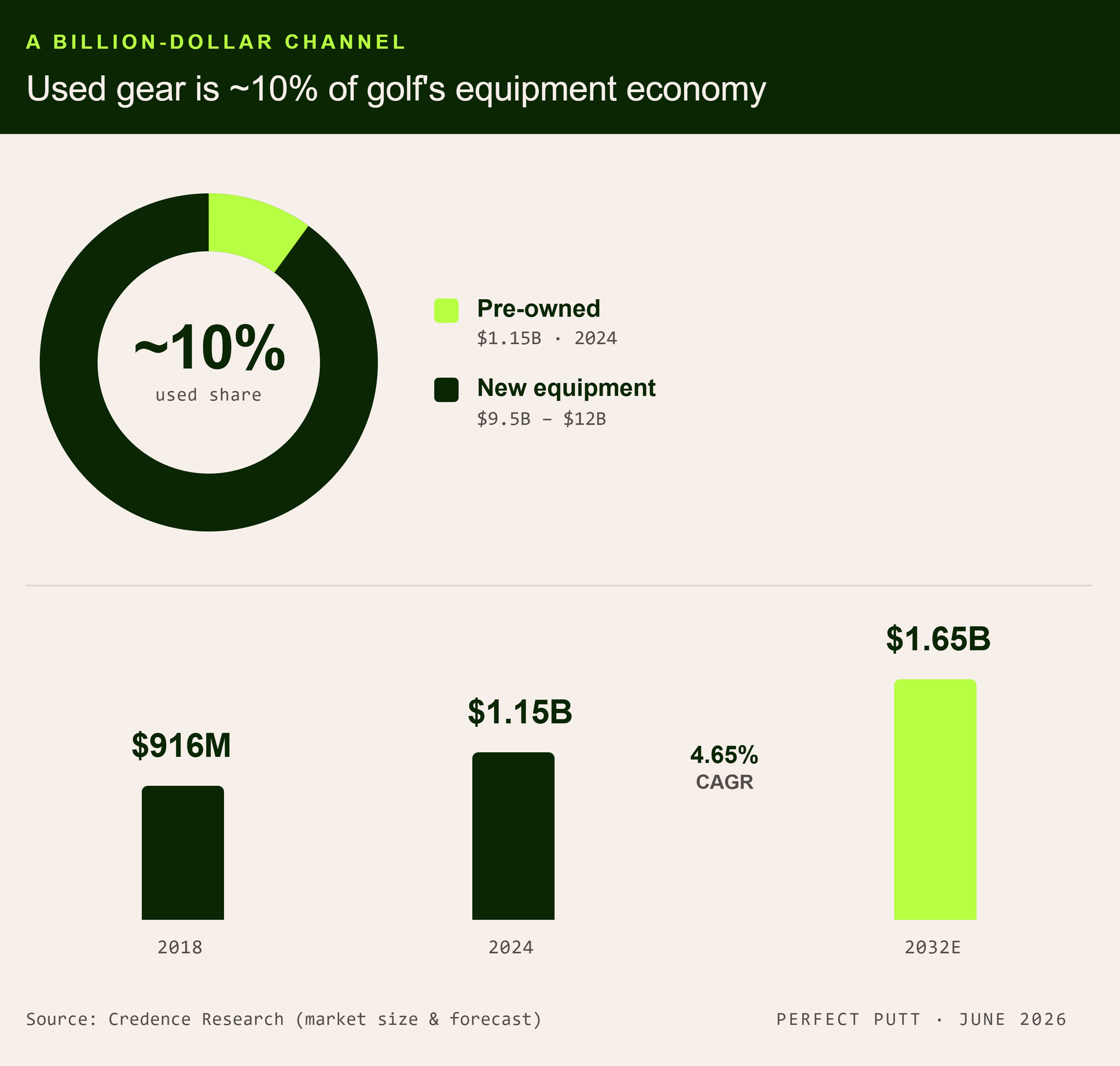

Start with size, because the number is bigger than the coverage suggests and smaller than the hype implies. Credence Research values the global market for pre-owned golf equipment at roughly $1.15 billion in 2024, up from about $916 million in 2018, and projects it will reach roughly $1.65 billion by 2032, a compound growth rate near 4.65%. That is not a niche. It is roughly a tenth the size of the global new-equipment market, which most researchers place between $9.5 billion and $12 billion.

A billion-dollar global channel growing faster than inflation is not a rounding error. It is a structural feature of how golfers acquire gear. Yet unlike most markets its size, it has no dominant public reporting line, no quarterly earnings call, and little analyst attention. It hides in plain sight precisely because it is split across trade-ins, certified pre-owned storefronts, consignment, and peer-to-peer marketplaces.

The Depreciation Engine

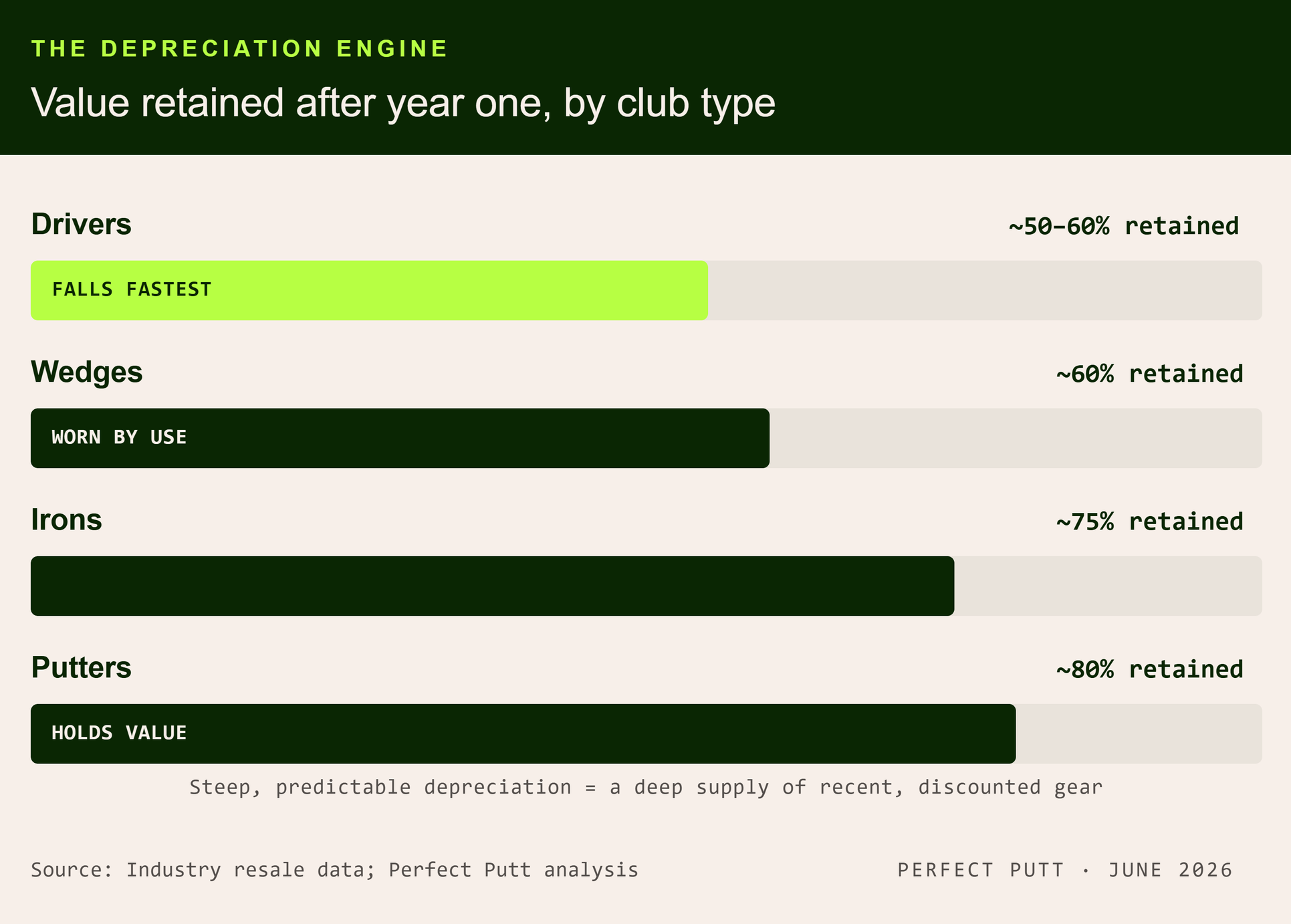

Every secondary market runs on the same fuel: the gap between what something costs new and what it is worth used. In golf, that gap is steep and predictable.

Drivers fall fastest, often losing 40% to 50% of their value in the first year alone, because the major manufacturers refresh their flagship lines on a near-annual cadence. Last season’s “longest driver ever” becomes this season’s trade-in the moment the new one ships. Wedges depreciate quickly too, worn down by use. Irons and putters hold value best; a well-kept putter can outlast a half-dozen driver cycles. Premium brands retain more than lesser names across the board.

Read one way, this is a consumer complaint: golf equipment loses value quickly. Read another way, it is the entire reason the secondary economy exists. Steep, reliable depreciation creates a deep supply of recently released, still-excellent equipment at a discount, and a steady stream of owners motivated to sell before the next markdown. The release cycle that frustrates buyers is the same release cycle that keeps the resale pipeline full.

The Cannibalization Question

The obvious objection deserves a real answer. If used equipment is growing, and manufacturers are not fighting it, what about the golfers who buy nothing but used gear?

That population is real. Spend time around equipment forums and you find golfers who never buy new. Beginners are routinely advised to start used, and value buyers treat three- and four-year-old premium clubs as the smart purchase, since on-course performance ages slowly while prices fall fast. For these golfers, the used market is not feeding new sales. It is replacing them.

So the honest version of the thesis is narrower than “the used market subsidizes the new market.” It is this: the secondary market appears to expand the overall equipment economy in ways that may outweigh the cannibalization. Three mechanisms are worth separating.

Entry. Cost is the single biggest barrier to taking up golf. A deep, trusted used market lowers that barrier and pulls in players who would otherwise stay out, some of whom become new-equipment buyers later.

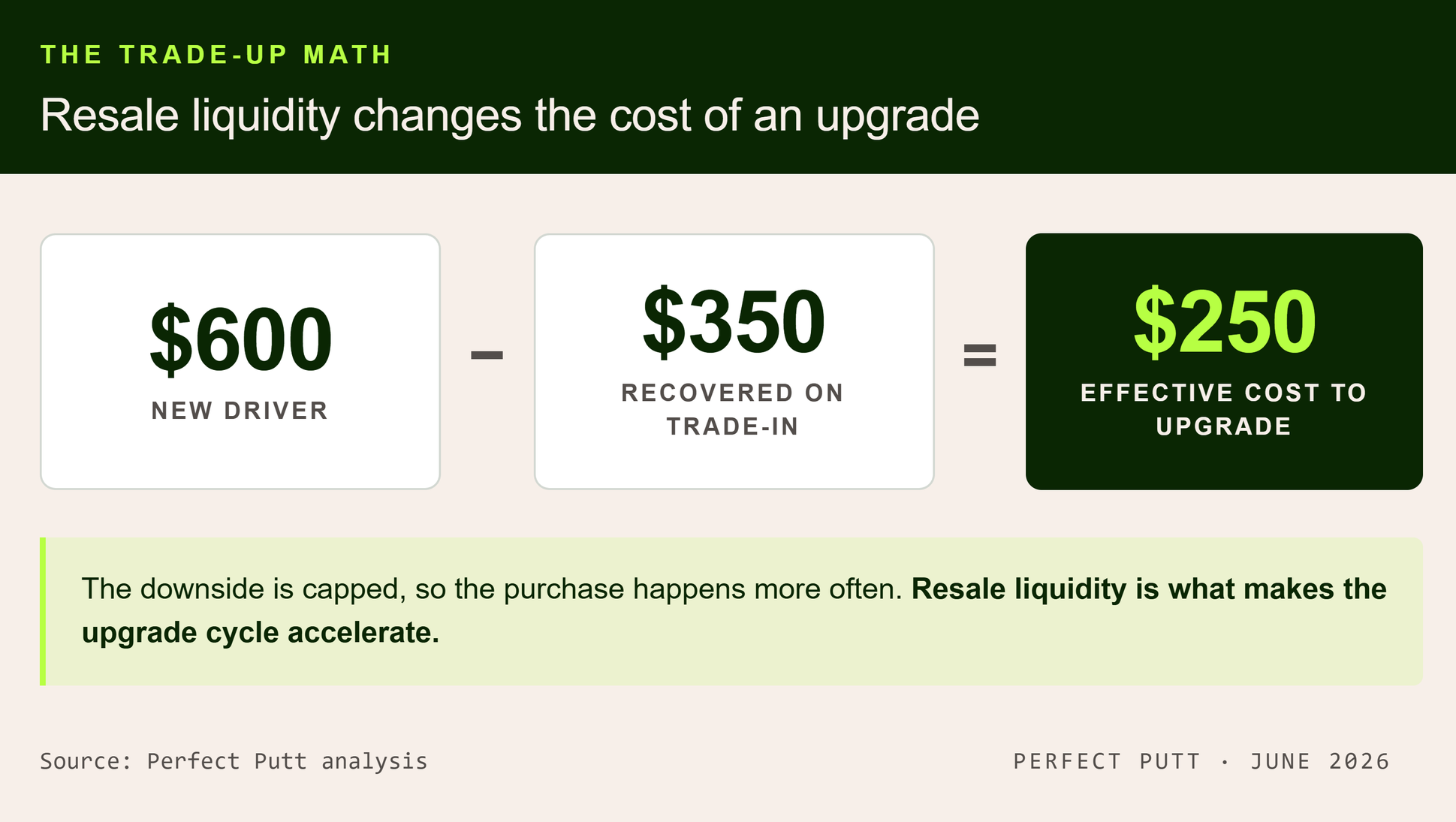

Trade-up. Resale liquidity changes the math on an upgrade. Recover $350 on a $600 driver and the effective cost to upgrade falls to $250. The downside is capped, so the purchase happens more often.

Churn. The golfers most active in resale tend to be the same ones who upgrade most often, recycling capital out of one purchase and into the next.

None of this makes cannibalization disappear. Some golfers will always buy used instead of new. The precise balance matters less than the direction of travel, and the fact that manufacturers, retailers, and platforms keep investing in trade-in and certified pre-owned programs tells you how the industry’s largest players read it.

From Product Sales to Lifetime Value

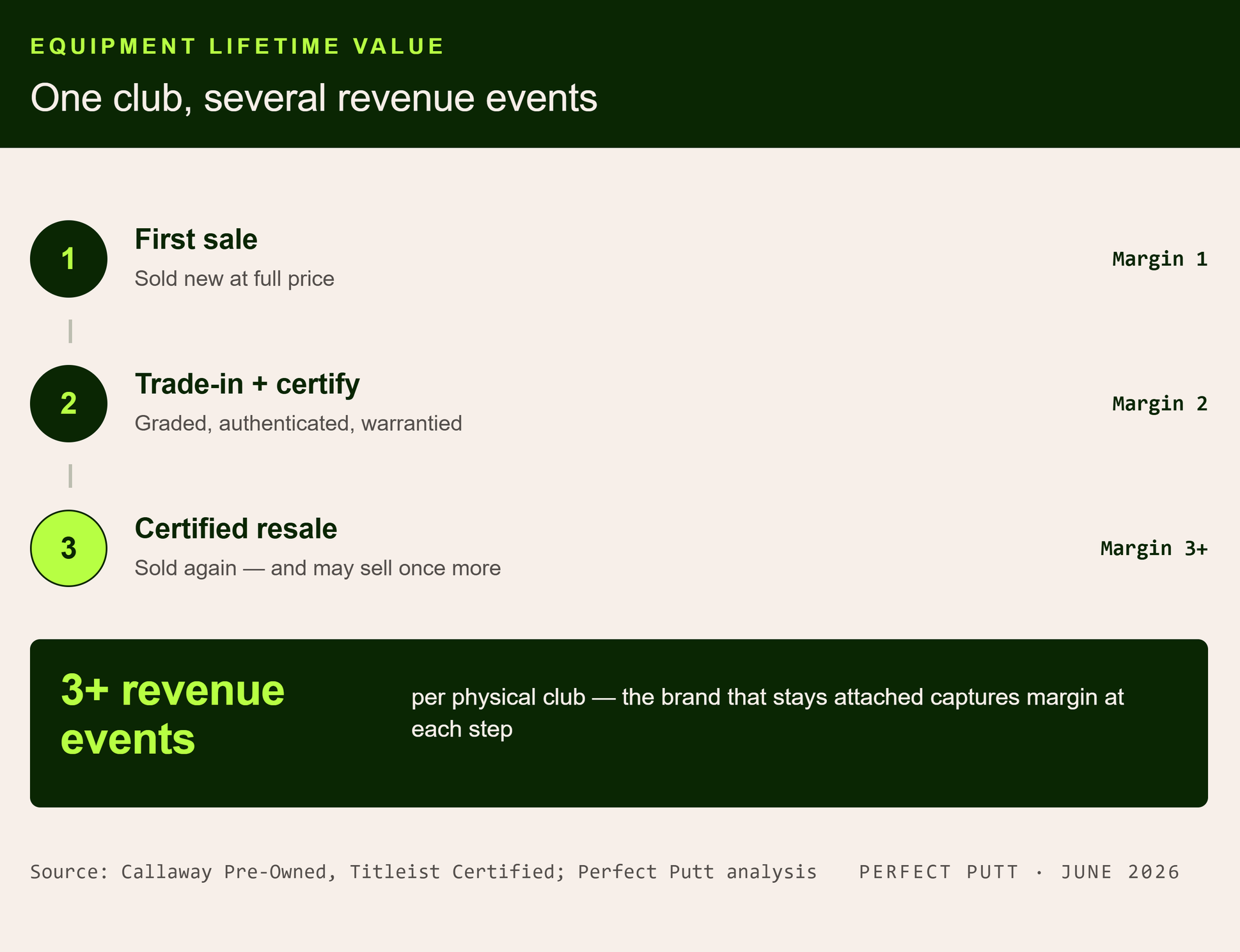

Historically an equipment company monetized a club once, then moved on. The shift now underway is that leading brands want to participate in the entire life of that asset, not just its first sale.

Call it equipment lifetime value. A new driver is sold. A year later it is traded in, graded, certified, and resold, and it may sell again after that. One physical club can generate several revenue events across its life, and the brand that stays attached to it captures margin at each step rather than watching the value leak to a third party. The economics start to resemble cars, watches, and sneakers, where the ownership cycle matters as much as the original sale.

This is why the majors now run their own resale channels. Callaway operates Callaway Golf Pre-Owned, with a “Trade In, Trade Up” program and a 90-day buy-back guarantee that returns store credit. Titleist runs Titleist Certified, where Acushnet sells serial-verified pre-owned clubs it has authenticated and graded itself, backed by a 12-month warranty. TaylorMade participates through its own pre-owned channels. Far from fighting resale, the biggest names now operate their own versions of it.

The strategic logic is about the customer, not the club. A golfer who trades a Titleist toward another Titleist stays inside the brand. A golfer who sells that same club to a stranger disappears from view. The first relationship compounds. The second resets. Seen that way, a trade-in is not a service. It is a customer-acquisition channel that also happens to recover inventory.

Who Is Building The Rails

The infrastructure has matured well beyond eBay listings and clubhouse bulletin boards. The clearest independent leader is 2nd Swing, which carries more than 150,000 new and pre-owned clubs and powers the PGA of America’s official Value Guide, a channel into thousands of club professionals. GlobalGolf built the certified pre-owned playbook: a multi-point inspection, a 12-month limited warranty, and UTry, which it bills as the industry’s first online try-before-you-buy program. The OEM channels sit alongside them. Underneath everything is the long tail of eBay, Facebook Marketplace, and auction apps, where golfers transact directly and the middleman disappears.

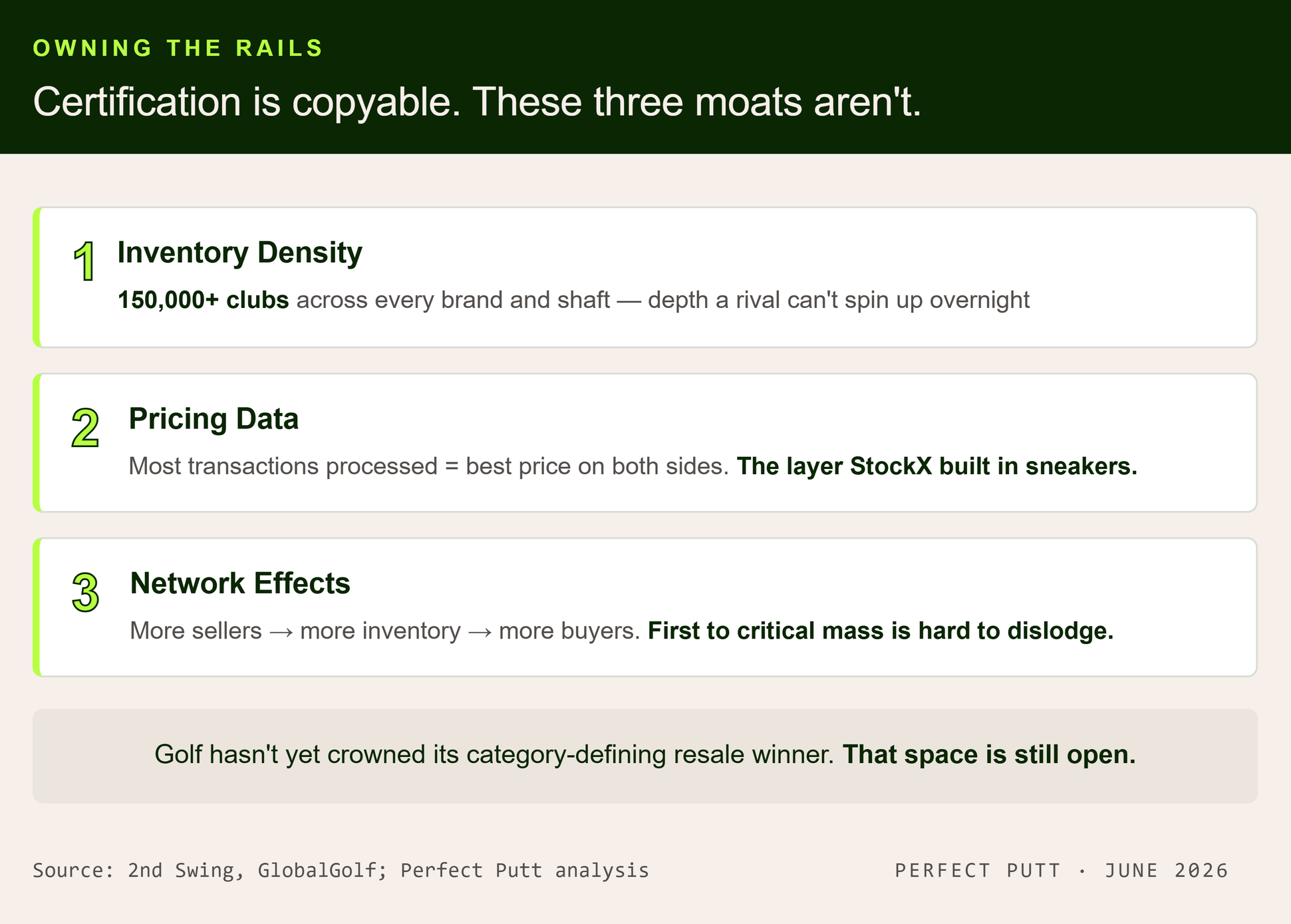

Certification is necessary but copyable, and every major OEM now runs one. Authentication is table stakes. The durable advantages sit one layer down.

Inventory density: a catalog of 150,000 clubs across every brand and shaft is not something a rival spins up overnight, and depth is what makes a buyer choose one seller over a thinner one.

Pricing data: the business that has processed the most transactions knows what every club is worth and can price both sides of the trade better than anyone. That is the layer StockX built in sneakers, where a live market price turned a resale site into a multibillion-dollar company.

Network effects: more sellers means more inventory, more buyers, and more sellers again. Whoever reaches critical mass first will be hard to dislodge.

Capital Relevance

For an investor, the appeal has little to do with golfers and everything to do with economics. Recommerce is structurally attractive. Take rates on resold goods typically run 10% to 25%, and the same physical item can be sold more than once, with incremental cost limited to repurchase and logistics. It may also prove more resilient in softer spending environments: when budgets tighten, golfers tend to trade down to used rather than out of the game, so the channel can hold up better than new-hardware sales. And it carries a real sustainability story, which travels well with capital.

That said, golf resale is not a software business. The operators that capture the most value handle physical goods: taking in trades, grading condition, refurbishing, processing returns, and carrying inventory until it sells. The winner may not be the company with the most clubs but the one with the fastest inventory turns, because accurate pricing shortens holding periods and disciplined logistics improve cash conversion. The durable winner needs both a pricing brain and an operational spine.

There is also a pattern worth respecting. Nearly every large durable-goods category has eventually produced a verticalized, data-driven resale winner. Golf has not yet crowned one.

2nd Swing and GlobalGolf have built meaningful positions, with genuine scale and infrastructure advantages in inventory, pricing data, and trade-in flow. But neither has yet become the category-defining consumer marketplace that StockX became for sneakers, the name a golfer thinks of first when they decide to sell. That space is still open.

What Happens Next

For an investor, the used club market is interesting for reasons that have little to do with golfers and everything to do with economics.

Two versions of the future are worth watching, and they are not mutually exclusive. In one, the OEMs deepen. Callaway, Titleist, and TaylorMade scale trade-in and pre-owned aggressively enough to keep the full lifecycle of their own equipment inside the brand, capturing resale margin that currently leaks to third parties. In the other, a platform wins: a specialist marketplace, built on authentication, data-driven pricing, and logistics, consolidates the fragmented long tail the way Carvana and StockX did in their categories. Both point in the same direction. The center of gravity is shifting from selling clubs to managing ownership cycles.

For years the used-club market was treated as a clearance bin. It has quietly become the connective tissue of the equipment economy, and a major input into how often golfers buy at all.

The everyday trade-in is not the end of a purchase. It is the start of the next one. And the real opportunity is not selling clubs. It is owning the upgrade cycle: the pricing intelligence, the trade-in infrastructure, the inventory density, and the customer relationship that sit between every set a golfer moves through. The most valuable company in this category may not be the one that sells the most clubs. It may be the one that owns the rails underneath all of them.

Treat golf resale as an asset-backed recommerce play, not a software bet. Underwrite inventory turns and cost of capital as hard as gross margin, and price the operational drag of physical goods into the return. The asymmetry favors whoever locks in the pricing-data layer and trade-in flow before a consumer brand consolidates the category. Until that winner emerges, the most investable exposure is the rails, not the clubs.

The best way to support Perfect Putt is to share it with a friend.