Golf Is Outgrowing Its Legacy Format

The game isn't running out of demand. It's running out of capacity.

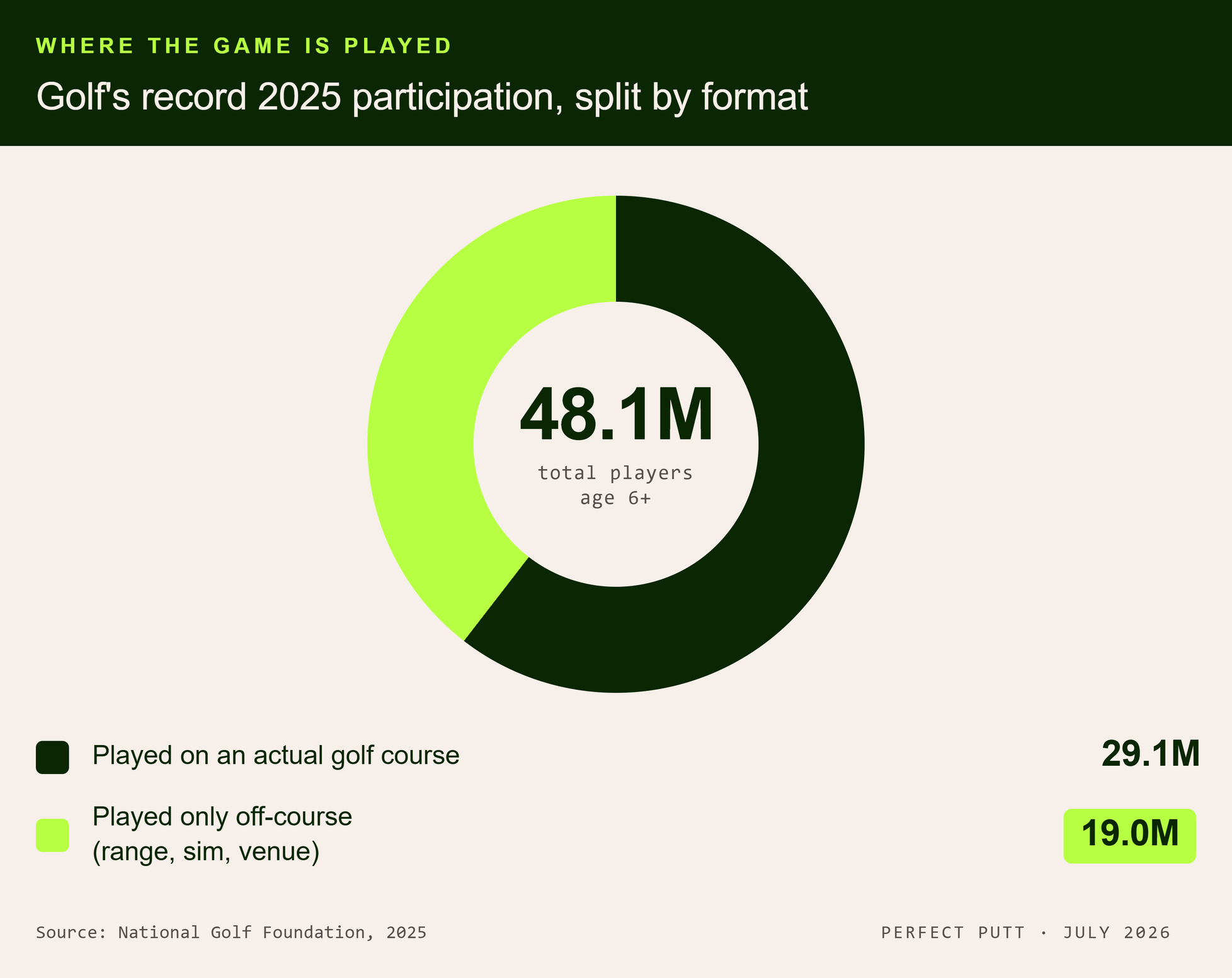

Golf set another participation record in 2025. Roughly 48.1 million Americans played the game, the eighth consecutive year of growth and nearly 50 percent more than a decade ago.

Yet the most important number in golf is not 48.1 million. It is 19 million.

That is how many people played golf last year without ever setting foot on a golf course. The traditional 18-hole round is not in decline. It is at capacity. Demand continues to grow, but the game's primary format can no longer absorb all of it. That disconnect is quietly reshaping where golfers spend their time, where developers build, and where capital is beginning to flow.

Welcome to Perfect Putt, a twice-weekly newsletter covering the business and economics of the golf industry. If this was forwarded to you, subscribe below to join 12,000+ readers who follow how capital flows through golf.

Read Time: 8 Minutes

Golf Has Reached a Capacity Ceiling

For most of golf's modern history, growth came from one of two places. Sell more rounds or charge more for them. Today, both levers are nearing their limits.

The United States has roughly 2,000 fewer golf facilities than it did at its supply peak in 2003, yet rounds played continue to reach record levels. Public green fees have risen roughly 29 percent since 2019, almost exactly matching inflation over the same period. Operators have already captured much of the pricing power created by the post-pandemic boom. There is little room for another meaningful step higher.

The remaining constraint is physical. A golf course sells daylight. Once the tee sheet is full, additional demand becomes a waitlist rather than incremental revenue. Faster rounds help only at the margin. Building new 18-hole courses is slow, expensive, and increasingly difficult. The traditional format has reached a capacity ceiling.

That explains why two headlines that appear contradictory are actually describing the same market. Golf participation continues to set records while rounds played grow only modestly. The traditional round is not losing relevance. It simply cannot accommodate everyone who now wants to play.

Capacity constraints reshape industries differently than demand constraints. When demand weakens, incumbents compete harder for the same customer. When capacity becomes scarce, new business models emerge to serve customers the incumbent product no longer can. That is exactly what is happening in golf.

The industry's next decade will be defined less by the traditional 18-hole round than by the businesses expanding access around it. Institutional investors continue buying scarce golf assets. Golf-native operators are increasingly building new capacity. That distinction will shape where much of the industry's future growth and investment returns are created.

Demand Is Arriving in a Shape the Course Cannot Hold

Look again at the 19 million Americans who played golf last year without ever setting foot on a golf course. It is easy to dismiss them as simulator users or Topgolf customers, but that misses the point. They actively chose golf and found a format that better matched how they wanted to spend their time. Off course participation now reaches nearly 38 million Americans and has become the largest driver of the game's growth over the past five years.

The traditional golf course was never designed for this customer. It assumes four or five available hours, a meaningful financial commitment, and often an established relationship with the game. Today's fastest growing golfer is different. They have ninety minutes after work, young children at home, or simply a preference for a more flexible experience. Their interest in golf is real. Their willingness to dedicate half a day to it often is not.

This is not a story about replacing traditional golf. It is a story about expanding it. The 19 million Americans who played exclusively off course last year are not defectors from green-grass golf. Most were never likely to book a Saturday morning tee time in the first place. Accessible formats create an on ramp into the game, broadening participation rather than dividing it.

That distinction explains why participation continues to climb even as rounds played grow only modestly. The industry is not running out of golfers. It is running out of places where those golfers can participate in ways that fit modern lifestyles. The best operators have recognized that shift. Rather than asking consumers to adapt to golf, they are adapting golf to consumers. The next generation of golf development is being built not for the avid golfer who already plays twice a week, but for everyone else.

The Format That Fits, and the Proof It Already Works

The industry's response has not been to reinvent golf. It has been to compress it.

The emerging model preserves everything people enjoy about the game while removing many of the barriers that have historically limited participation. A well-designed short course delivers real golf on real grass with real shots in less than two hours. Add lighting and the property remains productive long after sunset. Add a technology enabled driving range, simulator bays, instruction, and quality food and beverage, and the experience evolves from a single activity into a destination that can serve golfers and non-golfers alike throughout the day.

This is not a simplified version of golf. It is a more flexible one. The objective is no longer to maximize rounds played. It is to maximize engagement.

That distinction is increasingly evident in the projects opening across the country.

Consider 3's in Greenville, South Carolina. At its center is a fully lit, walkable 12-hole par 3 course that can be completed in under two hours. Wrapped around it is a food and beverage program designed to encourage guests to linger long after the final putt. Golf remains the anchor, but the gathering becomes the product. Friends meet for dinner and play a few holes. Families stop by after work. Leagues fill evenings that a traditional course could never monetize because daylight has already disappeared.

The Park in West Palm Beach demonstrates that the concept extends well beyond private development. The city transformed a conventional municipal facility into a broader community asset by pairing a Gil Hanse designed championship routing with a lighted nine-hole short course and a dedicated children's golf area. The result is a facility that welcomes serious players without excluding everyone else. Accessibility and architectural quality no longer sit in opposition. They reinforce one another.

ParOne at SkyRidge, which opened near Park City in 2026, offers perhaps the clearest glimpse of where the model is heading. A short course sits alongside a technology enabled driving range, simulator lounges, and a full food and beverage offering, creating a golf centered hospitality campus rather than a standalone golf course. The customer can practice, play, eat, socialize, or simply spend an evening on property without feeling obligated to commit to a traditional round.

Three projects. Three different ownership models. Three different markets. Yet each arrives at the same conclusion. The winning asset is becoming less about building another golf course and more about building a golf ecosystem.

That distinction matters because the economics of a golf property improve as reasons to visit multiply. A traditional course succeeds when someone books a tee time. A golf campus succeeds whenever someone walks through the front gate. The golfer who comes for nine holes may stay for dinner. The family that arrives for dinner may decide to play a short loop. The beginner who starts on the practice range may eventually join a league or book instruction. Every additional experience reinforces the next.

The shift mirrors what has happened across much of the broader leisure economy. The strongest businesses are no longer defined by a single transaction. They create ecosystems that encourage repeat engagement across multiple occasions. Golf is beginning to follow the same path.

That is why the most interesting developments in the industry increasingly resemble mixed use hospitality assets more than traditional golf facilities. They are designed not around the scorecard, but around frequency. The more often people find reasons to visit, the more valuable the underlying real estate becomes, and the stronger the operating business that sits on top of it.

A Better Business Model

Consumer demand alone would not justify this shift if the economics were weak. They are not. The short-format campus is not simply a more accessible version of golf. It is a more efficient business.

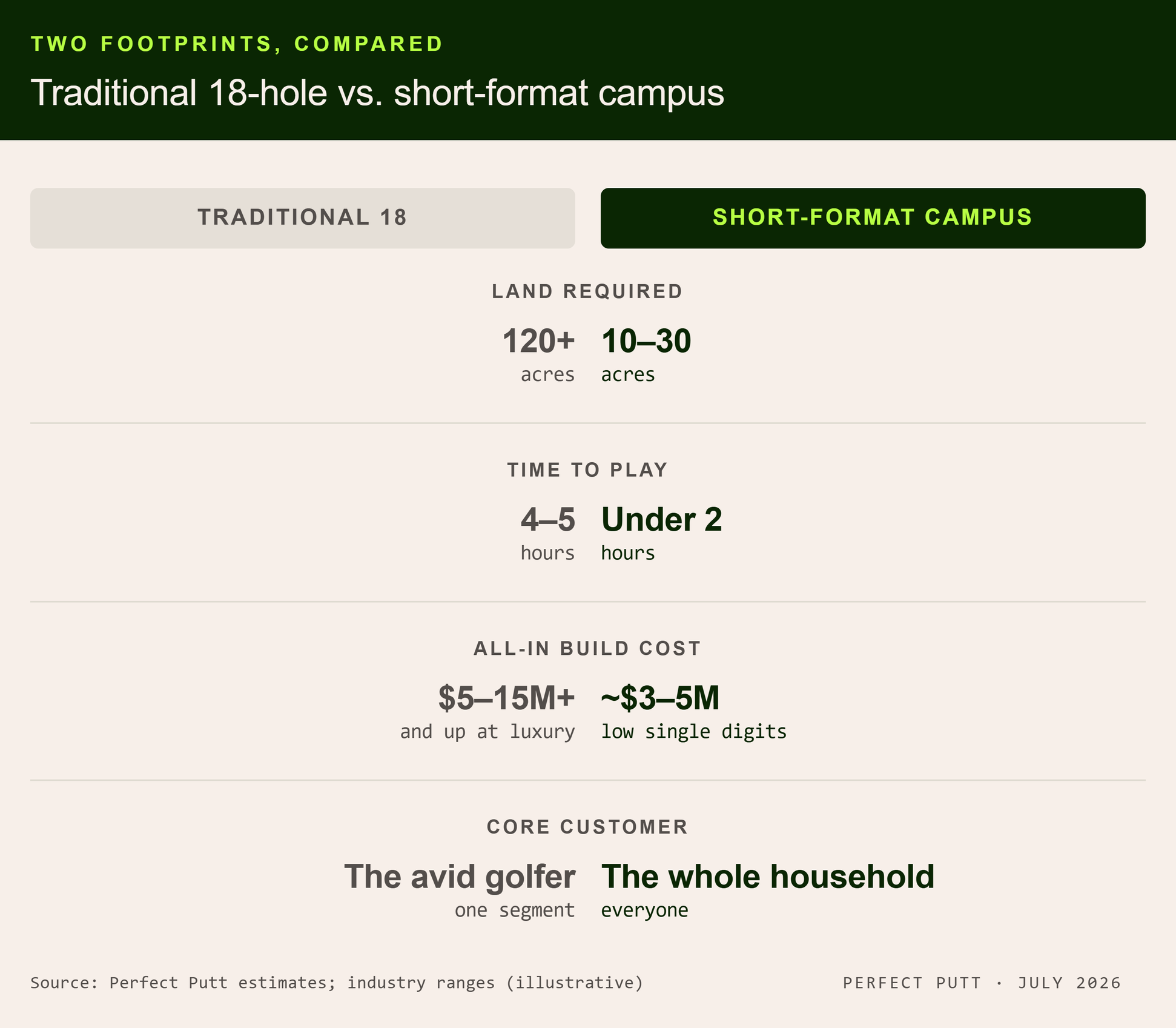

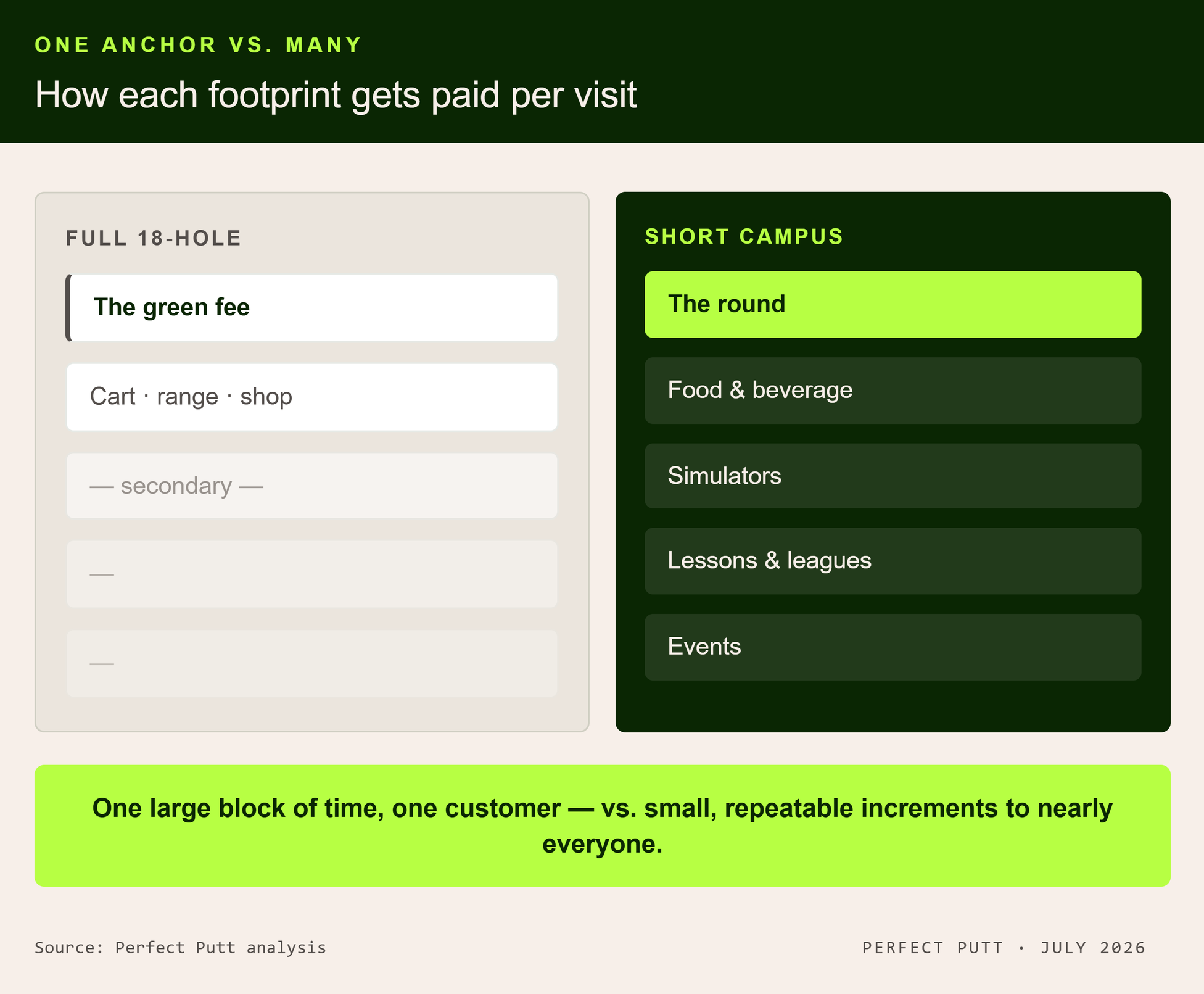

A traditional 18-hole course is a capital-intensive asset. Development typically requires more than 120 acres, build costs ranging from roughly $5 million to $15 million+ before land, and years of permitting, construction, and grow in before stabilized operations. Once open, it monetizes a finite number of tee times each day. Ancillary revenue from food and beverage, retail, and practice facilities matters, but the green fee remains the economic engine.

The golf campus reorders that equation. Development often requires only 10 to 30 acres and materially less capital, allowing projects to open faster and reach cash flow sooner. More importantly, each visit supports multiple revenue streams including golf, food and beverage, instruction, simulator bays, leagues, memberships, and events. Rather than maximizing revenue per tee time, operators maximize revenue per visit.

That distinction changes the economics. Smaller footprints reduce land, maintenance, and labor costs. Lighting and indoor facilities expand utilization beyond daylight hours and traditional playing seasons. The customer base broadens from avid golfers to families, beginners, and corporate groups while increasing visit frequency. A customer who plays an 18-hole course twice each month may visit a nearby campus twice each week.

The result is a business with lower capital intensity, faster development, broader demand, and more diversified cash flow. Developers are not building these campuses because they are novel. They are building them because every invested dollar serves more customers, generates more revenue opportunities, and reaches payback faster than the traditional model. The championship course maximizes the value of a tee sheet. The golf campus maximizes the lifetime value of a customer.

Capital Is Beginning to Rotate

The development pipeline already reflects the shift. Approximately 42 percent of all golf course openings in the United States between 2021 and 2025 were short courses. That is not a niche trend. It is a structural reallocation of development capital.

Traditional golf assets have also become increasingly expensive. Years of institutional capital flowing into private clubs, destination resorts, and established operators have elevated valuations while higher financing costs have compressed prospective returns for new buyers. None of this diminishes the long-term attractiveness of elite golf assets. The world's best clubs and resorts remain scarce and defensible. Scarcity alone, however, does not create growth.

Golf capital is quietly dividing into two strategies. Institutional investors continue acquiring irreplaceable legacy assets. Golf native operators are increasingly creating new ones. Rather than competing for existing rounds, they are expanding the market by serving customers who previously had no place within the traditional model.

That distinction also separates the golf campus from entertainment concepts. Entertainment venues monetize novelty. Golf campuses monetize habit. Players return because they are improving, because their league meets every Tuesday evening, because instruction creates regular engagement, or because the property naturally fits into everyday life. Habit is a more durable business than novelty. Over a full investment cycle, it generally produces stronger customer retention, greater pricing power, and more predictable cash flow.

The Investment Takeaway

Golf's next decade will not be defined by whether participation continues growing. It almost certainly will. The more important question is where that incremental demand will be served.

The traditional 18-hole course remains golf's aspirational product. The world's best clubs, resorts, and championship venues will continue to command extraordinary value because they represent something fundamentally scarce. That market is not disappearing, nor should investors bet against it.

The more compelling opportunity lies elsewhere. The industry's fastest growing customer increasingly seeks an experience measured in hours instead of half days. They want something easier to access, less intimidating to begin, and flexible enough to fit modern schedules. Businesses built around that customer are solving a structural capacity problem instead of simply competing for existing demand.

For investors, the implication is straightforward. Underwrite traditional golf as a scarce real asset where returns depend on disciplined acquisition and long-term stewardship. Underwrite accessible golf as a growth platform capable of expanding participation, increasing visit frequency, and generating multiple revenue streams from every customer interaction.

The next generation of category defining golf businesses may not own the most famous golf course. They may simply own the most valuable two hours of someone's week.

The best way to support Perfect Putt is to share it with a friend.