From Tee Time to Lifetime Value

For decades, golf optimized the round. The next decade will be defined by understanding the golfer.

Every course operator can tell you how many rounds were played, what green fees were collected, and how much revenue came from carts on any given day. Far fewer can answer the question that ultimately matters more: what is each golfer actually worth?

Welcome to Perfect Putt, a newsletter covering the business and economics of the golf industry. If this was forwarded to you, subscribe to join 12,000+ readers who follow how capital flows through golf.

Read Time: 9 Minutes

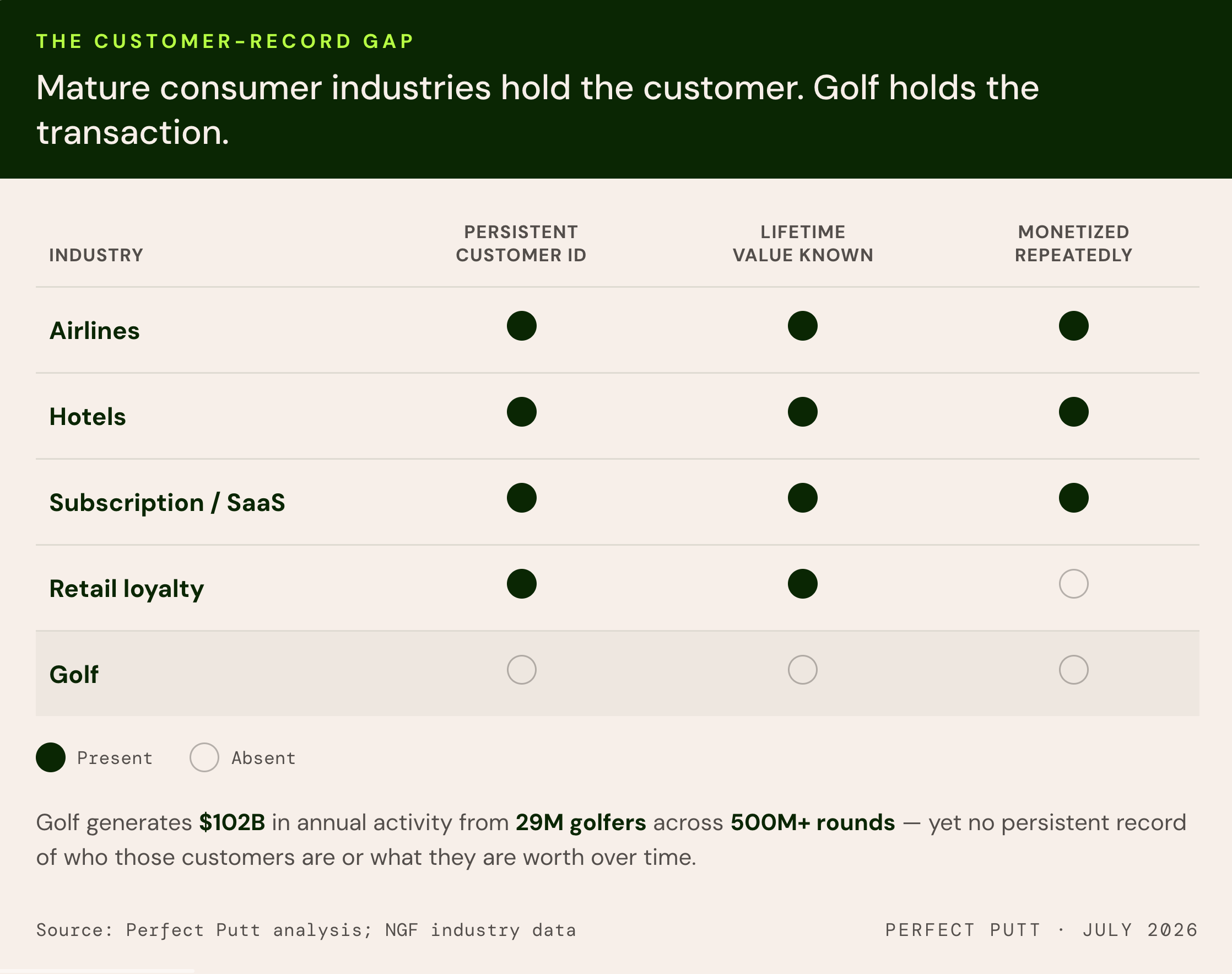

The Missing Customer Asset

Airlines know a passenger's lifetime value down to the dollar. They know how often they fly, which cabin they book, and whether they carry the co-branded credit card. Hotels, subscription businesses, and retailers with loyalty programs do too.

Golf, for the most part, does not.

A golfer who plays forty rounds a year, buys equipment at full price, and brings guests to the course often looks no different in an operator's system than someone who plays twice a year through a discount booking app. Both appear as individual transactions instead of customers with a measurable lifetime value.

This isn't primarily a technology problem. It is the legacy of how the industry was built. Golf's infrastructure was designed to operate facilities by managing tee sheets, carts, and point-of-sale systems, not to build a long-term understanding of the golfer. For decades, investment flowed toward filling tee times instead of understanding the people who filled them.

That distinction has become one of the industry's biggest strategic blind spots. Golf is not lacking customers. According to the National Golf Foundation, the industry generates more than $102 billion in direct economic activity each year, supported by roughly 29 million golfers who played more than 500 million rounds last year. What it lacks is a persistent understanding of who those customers are, how they engage across the golf ecosystem, and what they are worth over time.

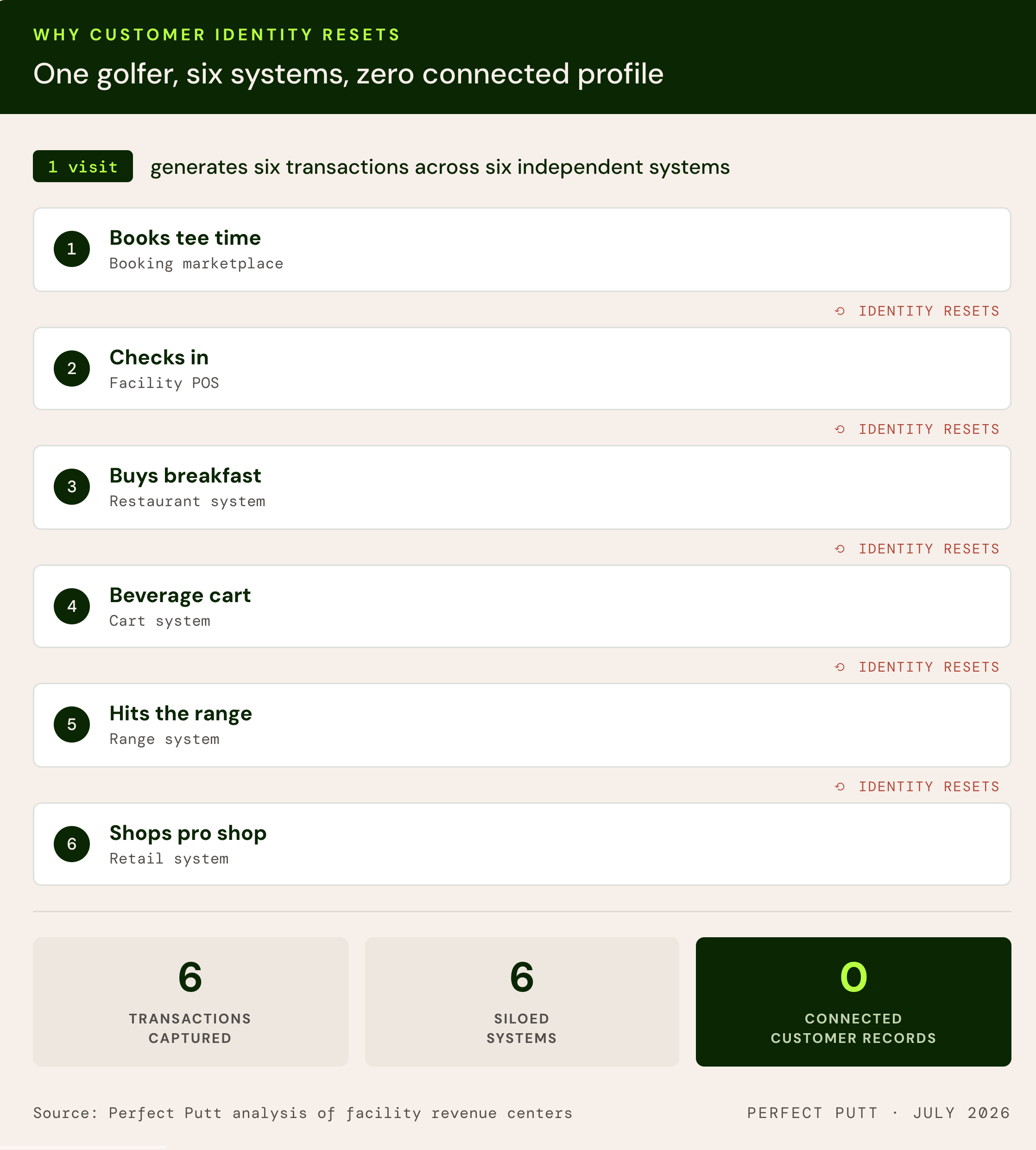

Why Customer Identity Resets

Follow a golfer through a single visit. They book a tee time through one platform. They check in using a different point-of-sale system. Breakfast is purchased through another system, the beverage cart through another, and the driving range through yet another. By the end of the round, one customer has generated five or six transactions, but the business still sees five or six separate interactions instead of one continuous customer relationship.

This is not an exception. It is how much of the industry operates. Its major revenue centers, including the pro shop, restaurant, cart fleet, driving range, and tournament operations, have historically been built as independent systems. Each is optimized to perform its own function, but few are designed to recognize the same customer as they move throughout the facility. The result is an industry that captures millions of transactions but retains remarkably little customer knowledge.

Compare that with hospitality. A hotel brand's most valuable asset is often not any single property, but the customer record that follows a guest across every stay. The shortage isn't visits. It is the infrastructure that turns those visits into a lasting customer asset.

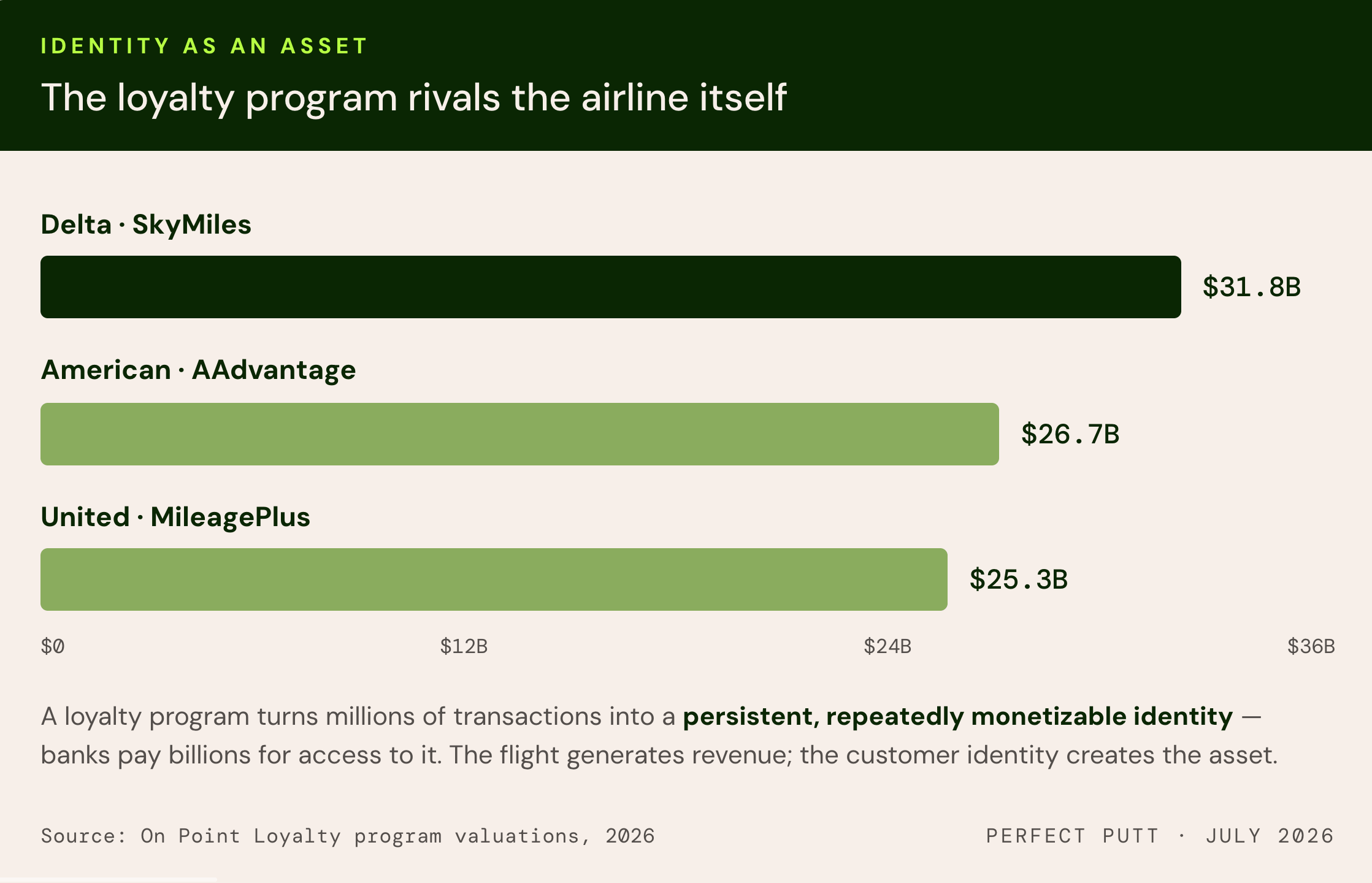

Identity as an Asset

The clearest evidence that customer identity compounds into enterprise value comes from one industry over. In 2026, loyalty consultancy On Point Loyalty valued Delta's SkyMiles program at more than $31.8 billion, ahead of American Airlines' AAdvantage at roughly $26.7 billion and United's MileagePlus near $25.3 billion. In each case, the loyalty program rivals or exceeds the value analysts assign to significant portions of the airline's operating business.

The reason is structural, not sentimental. A loyalty program transforms millions of individual transactions into a persistent customer relationship. That identity becomes valuable because it can be monetized repeatedly. Banks pay airlines billions of dollars for access to frequent flyers through co-branded credit cards, purchasing miles that encourage spending and reinforce loyalty. The flight generates revenue. Customer identity creates the asset.

Decades of facility-first infrastructure left golf too fragmented to build the equivalent. A shared customer identity never existed, so it never had the chance to compound. Nearly every mature consumer industry has gone through a similar transition. Airlines once believed they sold seats until loyalty programs became some of their most valuable assets. Restaurants once viewed the meal as the product until customer data and payments infrastructure became a strategic advantage. Golf has not reached that point yet.

The Infrastructure Layer

A useful preview of what this looks like comes from the restaurant industry, where the infrastructure around the meal has become as valuable as the meal itself. Toast processed roughly $51 billion in gross payment volume during the first quarter of 2026 across more than 170,000 restaurant locations. Despite owning no restaurants, the company carries a market capitalization in the tens of billions of dollars because it sits at the center of the customer relationship. Each additional product, from online ordering and loyalty to payroll and marketing, makes the platform more valuable to operators and more difficult to replace.

Toast doesn't create value by running the restaurant. It creates value by owning the infrastructure that connects transactions into a persistent customer relationship.

Golf is approaching the same inflection point. Payments, loyalty, and point-of-sale infrastructure that once required custom development are now available as subscription software. The missing piece is no longer the technology. It is the customer identity layer that connects every interaction across the ecosystem. The software required to build this layer already exists. The question is who connects it first.

GolfNow, the dominant online tee-time marketplace, processes tens of millions of rounds each year across thousands of courses. It knows when and where a golfer plays, but its visibility largely ends at the reservation. It does not own the full customer journey once the golfer arrives at the facility, including on-course spending, retail, food and beverage, and instruction. Those are the interactions where customer value continues to compound instead of resetting with every visit.

Much of golf's investment activity remains focused on acquiring, operating, or improving physical assets. The larger opportunity is building the infrastructure that captures, connects, and compounds the value of the golfer.

Who Owns the Customer Relationship?

Consider the businesses surrounding a golfer's spending and ask which one compounds over time. A course operator may earn the highest margin on an individual round, but the relationship often resets with the next visit. Equipment brands face a different challenge. They can build strong loyalty, but purchases are infrequent, and growth depends on continually winning the next sale.

Commerce infrastructure operates differently. Rather than delivering the experience, it connects and aggregates the transactions behind it. A platform sitting across thousands of rounds captures a smaller share of each transaction, but compounds that value across every booking, purchase, lesson, retail order, and future interaction tied to the same customer identity. A golf course sells today's round. A customer platform compounds the value of every round that follows.

The market is already moving in that direction. In March 2026, Troon launched Access, a unified identity spanning tee-time booking, loyalty, paid membership, and retail purchases across more than 200 courses. For the first time within that network, a golfer who books a round, redeems points, and buys merchandise is recognized as one customer instead of three unrelated transactions.

More than 200 courses represents meaningful progress, but it remains only a fraction of the roughly 14,000 golf facilities in the United States. Performance data, on-course spending, instruction, and much of the broader golf ecosystem still sit outside that identity layer. No dominant customer platform exists today, but the direction is becoming increasingly clear. Whether it is built by an operator, a technology company, or an entirely new entrant, the business that connects the golfer across the ecosystem will own the asset that becomes more valuable with every interaction.

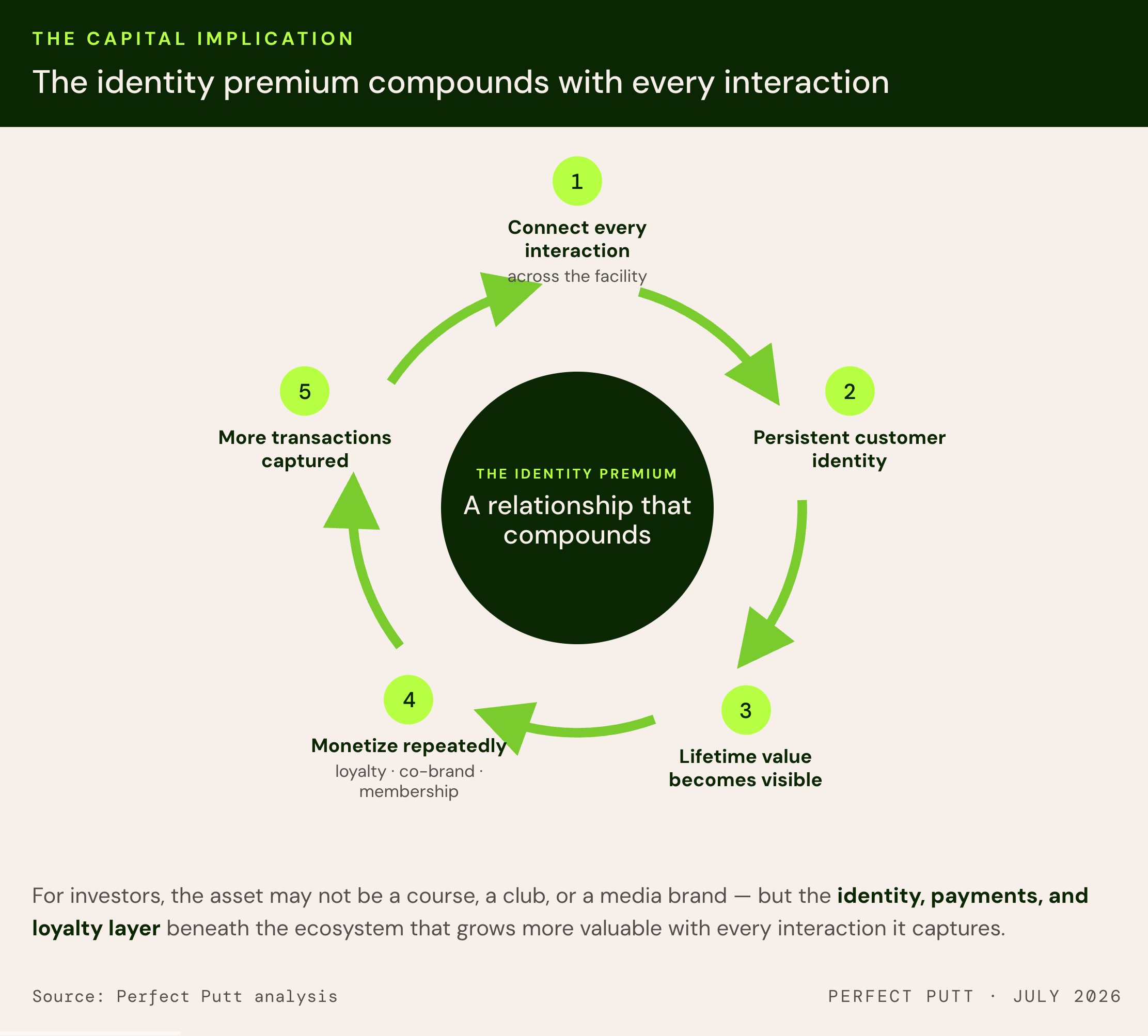

The Capital Implication

Taken together, these shifts suggest golf is changing categories. For decades, the industry has been organized around participation, measured by rounds played and courses built. Increasingly, it resembles a hospitality and commerce business organized around the golfer, where customer identity, loyalty, and transaction flow create more enduring value than any individual green fee.

For operators, the opportunity isn't simply increasing revenue per visit. It's building a customer relationship that survives from one visit to the next. Operators who know who their golfers are, how they engage, and what they are worth over time gain a durable advantage over those still managing isolated transactions.

For investors, the more compelling opportunity isn't the golf course, equipment brand, or media company. It's the infrastructure that connects them. The identity, payments, and loyalty layer beneath the ecosystem compounds value with every interaction it captures.

Building that infrastructure will not be easy. This market remains one of the most fragmented in consumer recreation. Thousands of independently owned public, private, and municipal facilities operate without a shared customer identity, and no company has enough scale to build one alone. That fragmentation is usually treated as the reason this cannot be built. It may also be the reason it becomes so valuable once it is. Unlike airlines or restaurants, where customer infrastructure emerged around a relatively concentrated set of operators, golf has no dominant platform and no incumbent to displace. The market is difficult to unify, but for the same reason, unusually open.

The next category-defining company in golf probably won't own a course, manufacture a club, or operate a tournament. It will be the first business that can answer a question the industry has rarely been able to ask: what is a golfer actually worth over a lifetime?

Every mature industry eventually discovers that its most valuable asset was never the one it thought it was selling. Golf still values its physical assets more precisely than its customers, which is precisely why the golfer remains largely unpriced.

The operators and investors who recognize that shift first won't simply earn more from the next round. They will own more of the lifetime value behind every round that follows.

The best way to support Perfect Putt is to share it with a friend.